The Ultimate Guide: What is a Roth IRA and How Does It Work?

By Peiman Daneshgar

Table of Contents

- Introduction

- What is a Roth IRA? A Simple Definition

- The History and Purpose of the Roth IRA

- How Does a Roth IRA Work?

- Roth IRA vs. Traditional IRA: Key Differences

- 2026 Contribution Limits and Income Eligibility

- The Five-Year Rule Explained

- Withdrawal Rules: What You Can Take Out and When

- Roth IRA Conversions and the Backdoor Strategy

- How to Open and Fund a Roth IRA

- Investment Options Within a Roth IRA

- Pros and Cons of a Roth IRA

- Roth IRA for Young Investors and Children

- Roth IRA for Retirement Planning

- Frequently Asked Questions

- Conclusion

Introduction

When it comes to retirement savings, few questions are as fundamental as: “What is a Roth IRA and how does it work?” Since its creation in 1998, the Roth IRA has become one of the most powerful and popular tools for building tax-free wealth in retirement. Yet for many, the rules, benefits, and strategies surrounding this account remain confusing.

In the current financial landscape of 2026, with updated contribution limits and evolving tax laws, understanding the Roth IRA is more important than ever. Whether you are just starting your career or are deep in your peak earning years, this account offers unique advantages that can transform your retirement lifestyle.

This comprehensive guide will answer every question you have about what is a Roth IRA and how does it work. We will explore the mechanics, the tax benefits, the rules, and the strategies that make the Roth IRA a cornerstone of smart retirement planning for millions of Americans .

What is a Roth IRA? A Simple Definition

A Roth IRA is a type of tax-advantaged individual retirement account that allows you to save for retirement with after-tax dollars . The key feature that distinguishes it from other retirement accounts is that qualified withdrawals in retirement are completely tax-free .

how much house can I afford on a $70,000 salary?

The Core Concept: Pay Taxes Now, Not Later

With a Roth IRA, you contribute money that you have already paid income taxes on. You receive no upfront tax deduction for your contributions . However, the money inside the account grows tax-free, and when you withdraw it in retirement—assuming you follow the rules—you pay zero federal income tax on those withdrawals, including all the investment gains .

Named After Senator William Roth

The account is named after Delaware Senator William Roth, who championed the legislation that created it. The Taxpayer Relief Act of 1997 established the Roth IRA, and it became available to investors starting in 1998 .

Not Just for Retirement

While primarily designed for retirement, the Roth IRA offers unique flexibility. You can withdraw your direct contributions (but not earnings) at any time, for any reason, completely tax-free and penalty-free . This makes it a powerful tool that can also serve as an emergency fund of last resort.

first-time home buyer grants and programs 2024

The History and Purpose of the Roth IRA

To fully understand what is a Roth IRA and how does it work, it helps to know why it was created.

Before Roth: The Traditional IRA

Before 1998, the primary individual retirement account was the Traditional IRA, created in 1974. With a Traditional IRA, you get a tax deduction when you contribute, but you pay ordinary income tax on every dollar you withdraw in retirement . This works well if you expect to be in a lower tax bracket when you retire.

The Roth Innovation

Senator Roth and his colleagues proposed a different idea: what if, instead of giving people a tax break now, we allowed them to contribute after-tax dollars and then never tax the money again? The goal was to provide tax diversification and to help taxpayers hedge against the risk of higher future tax rates .

Why It Matters Today

In 2026, with federal deficit concerns and historically low tax rates that could potentially rise in the future, the Roth IRA’s appeal has only grown. Locking in tax-free growth today protects you against whatever tax rates might look like 20 or 30 years from now.

is debt consolidation a good idea?

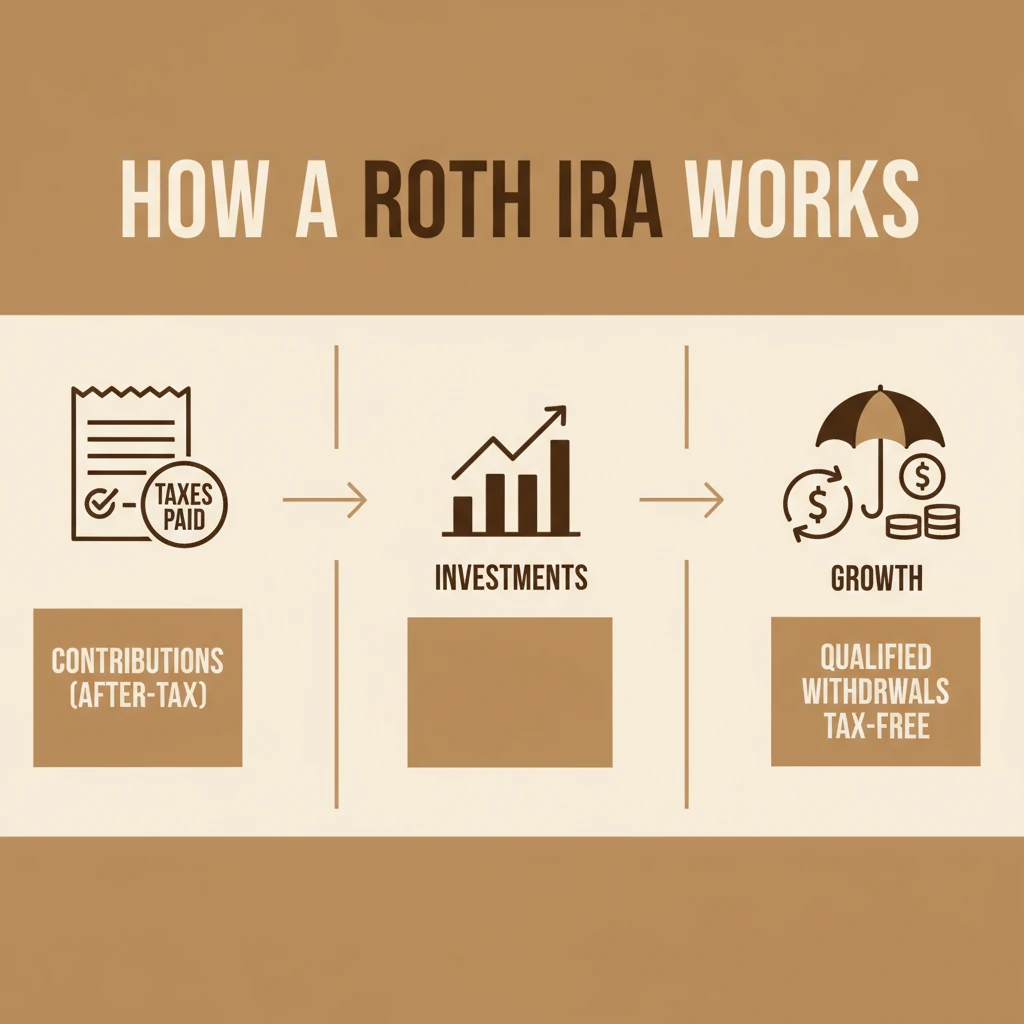

How Does a Roth IRA Work?

Let’s break down the mechanics of a Roth IRA step by step.

Step 1: You Contribute After-Tax Money

You fund your Roth IRA with money that has already been taxed. For example, if you earn $50,000 and contribute $7,000 to a Roth IRA, you still pay taxes on the full $50,000. You do not deduct the $7,000 from your taxable income .

Step 2: Your Money Grows Tax-Free

Once inside the account, your investments can grow through interest, dividends, and capital appreciation. You pay no annual taxes on any of this growth. Unlike a taxable brokerage account, you do not receive 1099 forms or pay capital gains taxes when you sell investments within the Roth IRA .

Step 3: You Withdraw Money Tax-Free in Retirement

When you reach age 59½ and your account has been open for at least five years, you can begin taking withdrawals. These “qualified distributions” are completely tax-free . You never pay taxes on the contributions you already made or on the decades of compounded growth.

how to talk to creditors when you can’t pay

A Simple Example

- Maria is 30 years old. She contributes $7,000 to her Roth IRA.

- She invests in a low-cost S&P 500 index fund.

- Over 30 years, her account grows to $75,000.

- At age 60, Maria withdraws $75,000.

- She pays $0 in federal income tax on the entire $75,000.

Roth IRA vs. Traditional IRA: Key Differences

To truly grasp what is a Roth IRA and how does it work, you must understand how it differs from a Traditional IRA .

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Treatment of Contributions | After-tax; no deduction | May be tax-deductible (depending on income) |

| Tax Treatment of Withdrawals | Tax-free (qualified distributions) | Taxed as ordinary income |

| Upfront Tax Break | No | Yes (if eligible) |

| Required Minimum Distributions (RMDs) | No RMDs during owner’s lifetime | RMDs begin at age 73 |

| Income Limits | Yes, contributions phase out at higher incomes | Deduction phases out if you have a workplace plan, but anyone can contribute |

| Early Withdrawal of Contributions | Anytime, tax-free and penalty-free | Subject to taxes and potential penalties |

| Age Limit for Contributions | None, can contribute after 70½ | Cannot contribute after age 70½ |

Which One Should You Choose?

The decision often comes down to your current tax bracket versus your expected future tax bracket .

- Choose a Roth IRA if: You expect to be in a higher tax bracket in retirement than you are now. You are young and your earnings have decades to grow tax-free. You want maximum flexibility and no RMDs.

- Choose a Traditional IRA if: You are in a high tax bracket now and expect to be in a lower bracket in retirement. You need the upfront tax deduction to make saving affordable.

2026 Contribution Limits and Income Eligibility

For 2026, the IRS has adjusted contribution limits and income phase-out ranges upward due to inflation .

Contribution Limits for 2026

| Age | Maximum Annual Contribution |

|---|---|

| Under Age 50 | $7,500 |

| Age 50 and Older | $8,600 ($7,500 + $1,100 catch-up) |

Important Rules:

- You cannot contribute more than your taxable compensation for the year.

- The limit applies to the combined total of all your IRAs (Traditional + Roth). If you have both, your total contributions cannot exceed these limits .

Income Eligibility for 2026 (Roth IRA Contribution Phase-Outs)

Not everyone can contribute the full amount to a Roth IRA. Your ability to contribute phases out based on your Modified Adjusted Gross Income (MAGI) .

| Filing Status | Full Contribution Allowed | Partial Contribution Phase-Out Range | Contribution Not Allowed |

|---|---|---|---|

| Single, Head of Household | MAGI less than $153,000 | $153,000 – $168,000 | MAGI $168,000 or more |

| Married Filing Jointly | MAGI less than $242,000 | $242,000 – $252,000 | MAGI $252,000 or more |

| Married Filing Separately | Not eligible for full contribution | $0 – $10,000 | MAGI $10,000 or more |

If your income exceeds these limits, you may still be able to fund a Roth IRA using the “Backdoor Roth IRA” strategy (discussed below).

government programs for medical debt relief

The Five-Year Rule Explained

One of the most misunderstood aspects of what is a Roth IRA and how does it work is the five-year rule .

Two Different Five-Year Clocks

There are actually two distinct five-year rules that apply to Roth IRAs:

Rule 1: The Five-Year Rule for Qualified Distributions

To withdraw your earnings tax-free, two conditions must be met:

- You must be at least age 59½ (or meet another qualifying event like disability or first-time home purchase).

- Your first Roth IRA must have been opened at least five tax years ago .

The five-year clock starts on January 1 of the tax year for which you made your first contribution, not the date you actually opened the account .

Example:

If you open a Roth IRA and make a contribution for the 2025 tax year on April 15, 2026, the five-year clock is considered to have started on January 1, 2025. You would satisfy the five-year rule on January 1, 2030.

Rule 2: The Five-Year Rule for Roth Conversions

Each Roth conversion has its own separate five-year clock. If you convert money from a Traditional IRA to a Roth IRA, you must wait five years to withdraw the converted amount without incurring a 10% early withdrawal penalty (if you are under age 59½) .

The Aggregation Rule

Once you satisfy the five-year rule for any Roth IRA, it applies to all of your Roth IRAs . However, this aggregation rule does not apply to Roth 401(k)s, which have their own separate five-year clocks.

how to use a balance transfer card wisely

Withdrawal Rules: What You Can Take Out and When

Understanding withdrawal rules is central to mastering what is a Roth IRA and how does it work .

The Ordering Rules

The IRS requires that withdrawals from a Roth IRA follow a specific order:

- Regular Contributions (come out first)

- Conversion Contributions (come out next, on a first-in, first-out basis)

- Earnings (come out last)

Withdrawals of Contributions (Anytime)

Because you already paid taxes on your contributions, you can withdraw them at any time, for any reason, completely tax-free and penalty-free .

Example: If you contributed $10,000 over the years and your account is now worth $15,000, you can withdraw up to $10,000 at any time with no taxes or penalties.

Qualified Distributions (Tax-Free and Penalty-Free)

A distribution is “qualified” and completely tax-free if:

- You are age 59½ or older AND the five-year rule has been met, OR

- You are disabled, OR

- You are taking a distribution as a beneficiary after the owner’s death

Non-Qualified Distributions (Taxes and Penalties May Apply)

If you withdraw earnings before age 59½ and before satisfying the five-year rule, those earnings are:

- Subject to ordinary income tax

- Subject to a 10% early withdrawal penalty

Exception: A 10% penalty (but not income tax) may apply to early withdrawals of converted amounts within the first five years after conversion .

Exceptions to the 10% Penalty

The IRS provides several exceptions to the 10% early withdrawal penalty, including:

- First-time home purchase (up to $10,000 lifetime limit)

- Qualified higher education expenses

- Unreimbursed medical expenses exceeding 7.5% of AGI

- Health insurance premiums while unemployed

- Disability or death

- Strategies to Pay Off $30,000 in Student Loans

Roth IRA Conversions and the Backdoor Strategy

What is a Roth Conversion?

A Roth conversion is the process of moving funds from a Traditional IRA (or other pre-tax retirement account) to a Roth IRA . You pay income tax on the amount converted in the year of conversion, but after that, the money grows tax-free.

The Backdoor Roth IRA Strategy

For high-income earners who cannot contribute directly to a Roth IRA due to income limits, the “backdoor Roth IRA” is a legal strategy to get money into a Roth IRA .

How it works:

- Make a non-deductible contribution to a Traditional IRA.

- Convert that Traditional IRA to a Roth IRA.

Important Caveat: The Pro-Rata Rule

If you have other pre-tax money in any Traditional IRA, SEP IRA, or SIMPLE IRA, the IRS considers all of your IRAs combined for tax purposes. You cannot convert only the non-deductible portion tax-free. A portion of every conversion will be taxable based on the ratio of pre-tax to after-tax money across all your IRAs .

How to Open and Fund a Roth IRA

Opening a Roth IRA is a straightforward process.

Step 1: Choose a Provider

You can open a Roth IRA with:

- Brokerage firms (Vanguard, Fidelity, Charles Schwab, etc.)

- Robo-advisors (Betterment, Wealthfront)

- Banks and credit unions (though investment options may be limited)

Step 2: Complete the Application

You will need to:

- Provide personal information (name, address, Social Security number)

- Designate beneficiaries

- Fund the account

- does debt settlement hurt your credit score?

Step 3: Fund Your Account

You can contribute in several ways:

- Lump sum (up to the annual limit)

- Automatic monthly transfers

- Transfer from another IRA (rollover or conversion)

Step 4: Choose Your Investments

Unlike a 401(k), which offers a limited menu, a Roth IRA allows you to invest in virtually anything: stocks, bonds, ETFs, mutual funds, and even some alternative investments .

Contribution Deadlines

You can contribute to a Roth IRA for a given tax year up until the tax filing deadline (typically April 15 of the following year) .

Investment Options Within a Roth IRA

One of the greatest advantages of a Roth IRA is the vast universe of investment choices .

What You Can Invest In

- Individual Stocks: Ownership shares in specific companies

- Bonds: Government, municipal, or corporate bonds

- Exchange-Traded Funds (ETFs): Baskets of securities that trade like stocks

- Mutual Funds: Professionally managed portfolios

- Target-Date Funds: Funds that automatically adjust asset allocation based on your retirement year

- Real Estate Investment Trusts (REITs): Real estate exposure

- Certificates of Deposit (CDs): FDIC-insured options at banks

- how to get out of payday loan debt fast

What You Generally Cannot Invest In

- Life insurance contracts

- Collectibles (art, antiques, rugs, metals, gems, stamps, coins, alcoholic beverages)

Investment Strategy Considerations

Because Roth IRA withdrawals are tax-free, it is often advantageous to place investments with the highest expected growth potential (like small-cap stocks or aggressive growth funds) in your Roth IRA. This maximizes the benefit of tax-free compounding.

best debt consolidation loans for good credit 2024

Pros and Cons of a Roth IRA

Pros

- Tax-Free Growth and Withdrawals: Once in retirement, you pay no taxes .

- No Required Minimum Distributions: You can let the money grow for as long as you live .

- Flexibility to Withdraw Contributions: Your contributions are always accessible .

- Hedge Against Future Tax Increases: You lock in today’s tax rates on your contributions.

- Estate Planning Benefits: Heirs can inherit Roth IRAs with favorable tax treatment .

- No Age Limit for Contributions: You can contribute after age 70½ if you have earned income .

Cons

- No Upfront Tax Deduction: You do not lower your current tax bill .

- Income Limits: High earners cannot contribute directly .

- Lower Contribution Limits than 401(k)s: At $7,500/$8,600, the limit is much lower than employer plans .

- Complex Rules: The five-year rule and ordering rules require careful planning .

Roth IRA for Young Investors and Children

One of the best times to learn what is a Roth IRA and how does it work is when you are young.

The Power of Starting Early

A person who contributes $7,000 per year from age 22 to 30 and then stops could easily end up with more money at retirement than someone who starts at 30 and contributes for 35 years. The magic of compound interest is maximized over long time horizons .

Roth IRA for Kids (Custodial Roth IRA)

If a child has earned income (from a part-time job, babysitting, lawn mowing, etc.), they can have a custodial Roth IRA. The parent manages the account until the child reaches adulthood. This can give a child a massive head start on retirement savings.

Roth IRA for Retirement Planning

Tax Diversification

Financial advisors often recommend having a mix of tax-deferred (Traditional 401k/IRA) and tax-free (Roth) accounts in retirement . This allows you to:

- Control your taxable income each year

- Manage Medicare premium surcharges (IRMAA)

- Withdraw strategically to minimize overall taxes

Estate Planning Benefits

Because Roth IRAs have no RMDs, they can be left to heirs to continue growing tax-free for their lifetimes (under certain rules). This makes Roth IRAs powerful wealth transfer vehicles .

Frequently Asked Questions

Q1: What is the main advantage of a Roth IRA?

The main advantage is that all qualified withdrawals in retirement are completely tax-free, including decades of compounded growth .

Q2: Can I lose money in a Roth IRA?

Yes. A Roth IRA is an investment account, not a savings account. The value can go down based on the performance of the investments you choose.

Q3: What are the 2026 Roth IRA contribution limits?

For 2026, the limit is $7,500 for those under 50 and $8,600 for those 50 and older .

Q4: What is the income limit for a Roth IRA in 2026?

For single filers, the phase-out range is $153,000 to $168,000 MAGI. For married couples filing jointly, it is $242,000 to $252,000 .

Q5: Can I withdraw money from my Roth IRA at any time?

You can withdraw your direct contributions at any time, tax-free and penalty-free. Withdrawing earnings before age 59½ and before the five-year rule is met may trigger taxes and penalties .

Q6: What is the five-year rule for Roth IRAs?

It is the requirement that your first Roth IRA must have been open for at least five tax years before you can withdraw earnings tax-free, even after age 59½ .

Q7: Can I have both a Roth IRA and a 401(k)?

Yes. You can contribute to both, provided you meet the income limits for the Roth IRA. This is a great way to maximize tax-advantaged savings .

Q8: What happens to my Roth IRA when I die?

Your designated beneficiary(ies) inherit the account. Spouses have special options, including treating it as their own Roth IRA. Non-spouse beneficiaries generally must empty the account within 10 years .

Q9: What is a backdoor Roth IRA?

A strategy for high-income earners to contribute to a Roth IRA by making a non-deductible Traditional IRA contribution and then converting it to a Roth IRA .

Q10: Is a Roth IRA better than a Traditional IRA?

It depends on your individual tax situation. Generally, a Roth is better if you expect to be in a higher tax bracket in retirement. A Traditional IRA is better if you want a tax break now and expect to be in a lower bracket later .

Conclusion

Understanding what is a Roth IRA and how does it work is essential knowledge for anyone serious about building long-term wealth. This remarkable account offers a unique combination of tax-free growth, flexibility, and estate planning benefits that simply cannot be found elsewhere.

In the 2026 tax environment, with updated contribution limits and ongoing economic uncertainty, the Roth IRA stands as a pillar of smart retirement planning. Whether you are just starting your career with a modest income or are a high earner navigating the backdoor strategy, the Roth IRA deserves a central place in your financial life.

The key takeaway is simple: pay taxes on your money now, let it grow for decades, and never pay taxes on it again. Your future self will thank you for the foresight and discipline you apply today.