The Ultimate Guide to First-Time Home Buyer Grants and Programs 2024

By Peyman Daneshgar

Buying your first home is a monumental milestone. It is the culmination of a dream, a step toward building generational wealth, and a declaration of independence. Yet, in today’s housing market, that dream can feel frustratingly out of reach. With median home prices hovering around $420,000 and mortgage rates climbing, the biggest hurdle for most first-time buyers isn’t finding the perfect house—it’s scraping together enough cash for the down payment and closing costs .

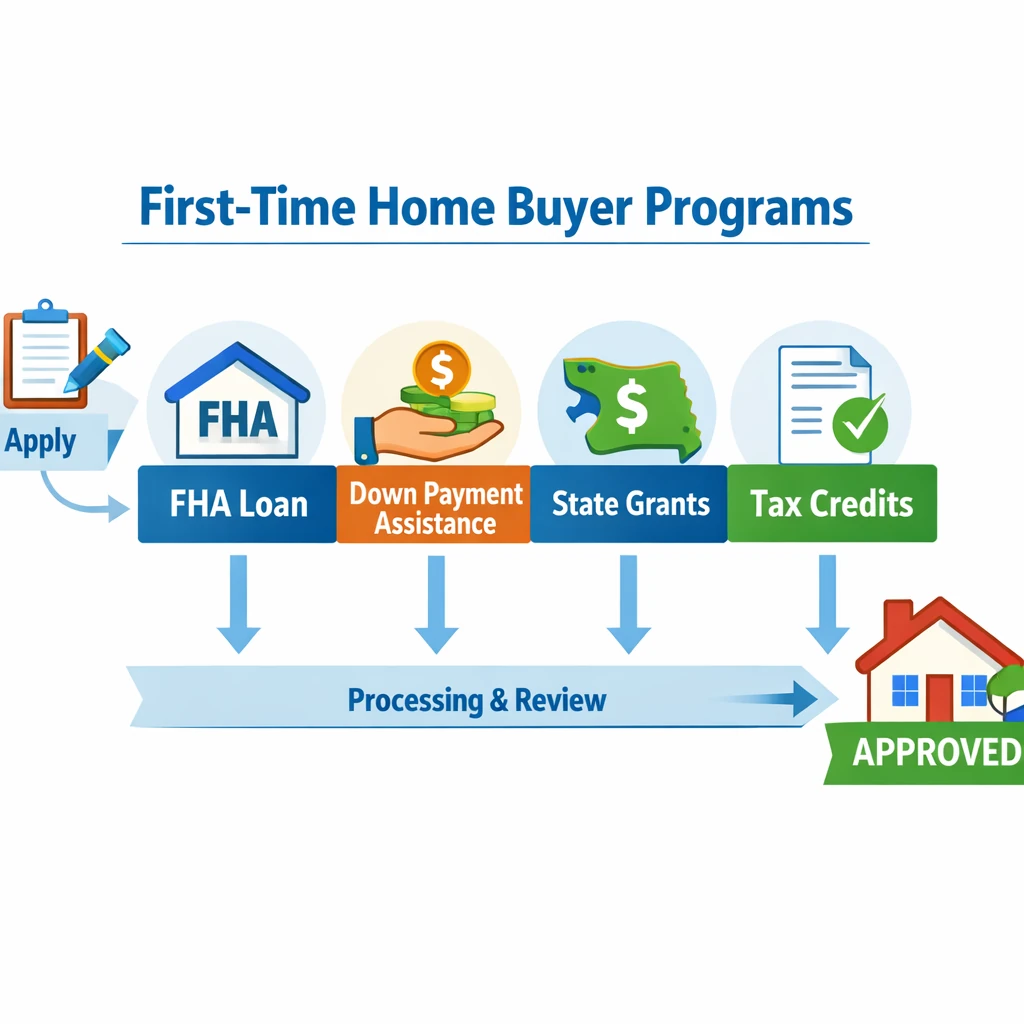

This is where first-time home buyer grants and programs 2024 become a game-changer. Across the United States, a vast network of federal, state, and local programs exists specifically to help people like you overcome this barrier. From grants that never have to be repaid to low-interest loans and special mortgage programs, billions of dollars in assistance are available. The key is knowing where to find them and how to qualify.

This guide is the definitive resource for navigating these opportunities. We will walk you through every major program, from the well-known FHA and VA loans to hyper-local down payment assistance in cities like Boston and Denver. By the end, you will have a clear roadmap to finding the financial help you need to unlock your first home.

Table of Contents

- What Are First-Time Home Buyer Grants and Programs?

- Federal First-Time Home Buyer Programs (The Foundation)

- State and Local First-Time Home Buyer Grants and Programs 2024

- National Down Payment Assistance Programs

- How to Find Programs in Your Area

- Who Qualifies as a “First-Time Home Buyer”?

- How to Apply for First-Time Home Buyer Grants and Programs 2024

- Frequently Asked Questions (FAQs)

- Conclusion: Your Path to Homeownership Starts Here

What Are First-Time Home Buyer Grants and Programs?

Before diving into the specifics, it is essential to understand the landscape of assistance. Not all help is created equal.

First-time home buyer grants are typically funds provided by a government agency or non-profit that you do not have to repay. They are often used for down payments or closing costs, provided you meet certain eligibility requirements, such as income limits and completing a homebuyer education course.

First-time home buyer programs is a broader term that includes grants as well as:

- Low-interest loans: Money you borrow (and repay) but at below-market rates.

- Deferred payment loans: Loans that sit on the property’s title with 0% interest and are forgiven after a certain period (e.g., 5, 10, or 30 years) or repaid only when you sell or refinance.

- Tax credits: Ongoing reductions in your tax liability, like the Mortgage Credit Certificate (MCC).

- Specialized mortgages: Loans like FHA, VA, and USDA that have lower down payment requirements than conventional loans.

The key takeaway is that billions of dollars in assistance go unclaimed every year simply because buyers do not know these first-time home buyer grants and programs 2024 exist .

how to create a budget for beginners step by step

Federal First-Time Home Buyer Programs (The Foundation)

Before looking for grants, you need to understand the federal loan programs that make homeownership accessible. These are not grants, but they are the foundation upon which most other assistance is built.

FHA Loans: Low Down Payment, Flexible Credit

FHA loans, insured by the Federal Housing Administration, are a top choice for first-time buyers .

- Down Payment: As low as 3.5% for borrowers with credit scores of 580 or higher. If your credit score is between 500 and 579, you may still qualify with a 10% down payment .

- Credit Flexibility: Generally more forgiving of lower credit scores than conventional loans.

- Loan Limits: In 2024, the FHA loan limit for a single-family home in most low-cost areas is $498,257, and in high-cost areas, it can go up to $1,149,825 .

- Key Consideration: You will have to pay mortgage insurance premiums (MIP) both upfront and annually, typically for the life of the loan if you put down less than 10%.

VA Loans: Zero Down for Veterans and Military

For those who have served, the VA loan is arguably the most powerful home buying tool available .

- Down Payment: 0% down is the standard. No down payment required.

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than 20% down, VA loans do not require monthly mortgage insurance.

- The Savings: On a typical $430,000 home, a conventional buyer might need over $51,000 upfront, while a VA buyer can purchase with $0 down, saving years of saving time .

- Utilization: While highly beneficial, these loans are underutilized in some high-cost areas like New York and Los Angeles, often due to a lack of awareness or co-op restrictions .

- how to save for a house down payment in 2 years

USDA Loans: Zero Down for Rural Homebuyers

The USDA loan program is designed to encourage homeownership in rural and suburban communities .

- Down Payment: 0% down.

- Eligibility: The home must be in a USDA-eligible area. Surprisingly, 97% of U.S. land mass is eligible, including many small towns and suburbs with populations under 35,000 .

- Income Limits: Your household income cannot exceed 115% of the median income for that area .

- Loan Limits: In 2024, the standard loan limit for guaranteed loans is $398,600, with higher limits in high-cost counties .

Conventional Loans (Fannie Mae and Freddie Mac)

Conventional loans are not government-backed but often have first-time buyer-friendly features like 3% down payment programs (e.g., Fannie Mae’s HomeReady or Freddie Mac’s HomeOne). They are best for buyers with good credit who want to avoid the strict property requirements of FHA or USDA loans.

best budgeting method for irregular income

State and Local First-Time Home Buyer Grants and Programs 2024

This is where the real treasure hunt begins. States, counties, and cities offer targeted assistance that can be layered on top of your federal loan. Here are some standout examples of first-time home buyer grants and programs 2024 from across the U.S.

California: Dream For All Shared Appreciation Loan

California’s “Dream For All” program is a innovative state-level initiative designed to help first-generation homebuyers .

- What it is: A shared appreciation loan. The state provides a voucher offering up to 20% of a home’s value for down payment and closing cost assistance.

- Eligibility: Targeted specifically at first-generation homebuyers—those whose parents do not own a home .

- How it works: In 2024, 1,700 first-generation buyers were conditionally approved through a random selection process due to high demand. Recipients have 90 days to find a home.

- Repayment: When you sell or refinance, you repay the initial assistance plus up to 20% of any increase in the home’s value. These funds then help future buyers .

- how to stop impulse buying online

Boston, MA: BHA First Home Program

The City of Boston has allocated significant funding to help its residents achieve homeownership .

- What it is: A down payment assistance program specifically for families in the Boston Housing Authority (BHA).

- The Grant: Eligible families receive $75,000 towards the purchase of a home in Boston .

- Funding: In late 2024, Mayor Michelle Wu allocated an additional $3 million in ARPA funds to continue this program through 2026, aiming to help an additional 57 families. The program has already helped over 50 BHA residents buy homes .

Denver, CO: UMB First-Time Homebuyer Grant

UMB Bank offers a unique grant program for buyers in specific low-to-moderate income areas of Denver .

- What it is: A one-time grant.

- The Grant: Qualifying borrowers can receive a grant of 5% of the purchase price (for a down payment) plus up to 2% lender credit for closing costs. Alternatively, a 3% grant option is available .

- Eligibility: Limited to designated census tracts in Adams, Arapahoe, Denver, Douglas, and Jefferson counties. Income limits apply.

- how to create a budget

Phoenix, AZ: UMB Down Payment Assistance

In Maricopa County, Arizona, UMB offers two paths to assistance .

- Option 1 (Grant): A one-time grant of 3% of the purchase price for a down payment, plus up to 2% lender credit for closing costs.

- Option 2 (Assistance): Qualifying borrowers can finance up to 100% of the purchase price of the home, effectively a zero-down loan.

- Eligibility: Limited to designated census tracts within Maricopa County.

- 50/30/20 rule calculator excel template free

Missouri, Kansas, and Texas: UMB Down Payment Assistance

In limited areas across these three states, UMB offers a program to help buyers .

- What it is: A loan program and closing cost credit.

- The Assistance: Qualifying borrowers can borrow up to 100% of the purchase price and may receive up to 2% lender credit towards closing costs.

- Eligibility: Limited to specific counties, including Jackson and Clay in Missouri, Johnson and Wyandotte in Kansas, and Collin, Dallas, and Tarrant in Texas .

Western Australia: Home Buyers Assistance Account (For Australian Readers)

While this guide is primarily U.S.-focused, it is worth noting that government assistance exists globally. For example, in Western Australia, first-time buyers can apply for the Home Buyers Assistance Account (HBAA) grant .

- The Grant: Up to $2,000 AUD to reimburse expenses like stamp duty, legal fees, and mortgage insurance.

- Eligibility: The property must be purchased for $500,000 or less (as of the 2024 expansion), and the buyer must live in it for at least 12 months .

- how to use a balance transfer card wisely

National Down Payment Assistance Programs

In addition to state and local programs, there are national non-profits and resources that can help you find and secure assistance.

- NID Housing Counseling Agency: HUD-approved agency offering education and counseling.

- Down Payment Resource: A website (downpaymentresource.com) that tracks down payment assistance programs nationwide. You can enter your details to see what you might qualify for.

- Your Mortgage Lender: Many large lenders have their own proprietary grant programs. For example, Bank of America offers the “America’s Home Grant” which provides up to $10,000 for closing costs or rate buydowns. Always ask your lender what specific grants they offer.

- how to save money on a tight income

How to Find Programs in Your Area

Finding the right first-time home buyer grants and programs 2024 for your specific location requires a bit of detective work. Here is your action plan:

- Start with HUD: Visit the U.S. Department of Housing and Urban Development (HUD) website and look for the “HUD Approved Housing Counseling Agency” list. Find an agency near you and schedule a counseling session. This is often a requirement for grants and is the best first step.

- Check Your State Housing Finance Agency (HFA): Every state has an HFA (e.g., CalHFA in California, MassHousing in Massachusetts). Their websites are treasure troves of information on state-specific loans, grants, and tax credits.

- Check Your City and County: Go to the official government website for your city and county. Search for terms like “down payment assistance,” “first-time home buyer,” or “housing department.” As seen with Boston, local funding can be substantial .

- Talk to a Local Lender: Find a mortgage officer who specializes in first-time home buyer programs. They work with these programs every day and can quickly tell you what you qualify for.

- money saving challenges for couples

Who Qualifies as a “First-Time Home Buyer”?

You might be surprised to learn that the official definition is broader than you think. According to HUD, you are considered a first-time home buyer if you meet any of the following criteria:

- An individual who has had no ownership in a principal residence during the three-year period ending on the date of purchase of the property.

- A single parent who has only owned a home with a former spouse while married.

- A displaced homemaker who has only owned with a spouse.

- An individual who has only owned a principal residence not permanently affixed to a permanent foundation in accordance with applicable regulations.

- An individual who has only owned a property that was not in compliance with state, local, or model building codes and which cannot be brought into compliance for less than the cost of constructing a permanent structure.

This means that even if you owned a home years ago, you may still qualify as a first-time buyer today.

How to Apply for First-Time Home Buyer Grants and Programs 2024

- Get Pre-Approved: Talk to a lender to get pre-approved for a mortgage. This tells you your price range and shows sellers you are serious.

- Complete Homebuyer Education: Many grants require you to complete a HUD-approved homebuyer education course. Do this early.

- Find a Real Estate Agent: Look for an agent experienced in working with first-time buyers and assistance programs.

- Apply for the Grant: Your lender or housing counselor will typically help you complete the grant application. Be prepared to provide income documentation (tax returns, pay stubs) and proof of assets.

- Make an Offer and Close: Once your grant is approved, you can make an offer on a home with confidence, knowing your down payment and closing costs are covered.

- sinking funds: what are they and how to set them up

Frequently Asked Questions (FAQs)

1. What is the best first-time home buyer grant?

There is no single “best” grant—it depends entirely on where you live and your personal situation. For a veteran, the VA loan is unbeatable. For a low-income buyer in Boston, the $75,000 BHA grant is life-changing. The best program is the one you qualify for that offers the most financial help for your specific needs.

2. Do I have to pay back first-time home buyer grants?

It depends on the type. True grants, like the UMB grants in Denver, do not need to be repaid . Deferred payment loans, like California’s Dream For All program, must be repaid when you sell or refinance, often with a share of the appreciation . Always read the fine print.

3. Can I use more than one grant or program?

Yes! This is known as “layering.” For example, you might use an FHA loan (federal) combined with a state-level down payment assistance program (state) and a lender-specific grant (local). Your lender or housing counselor can help you layer assistance, but there are often limits, so coordination is key.

4. What credit score do I need for these programs?

It varies. FHA loans can go as low as 500 with 10% down, or 580 with 3.5% down . USDA and VA loans do not have a published minimum, but lenders typically look for a score of 620 or higher . Many state and local grants require a score in the mid-600s.

5. Are these programs only for low-income buyers?

While many programs have income limits (often set at 80% or 120% of the area median income), not all do. For example, the standard USDA guaranteed loan allows income up to 115% of the area median . Some programs, like certain conventional 3% down loans, have no income limit at all.

6. How much do I need for a down payment?

With programs like VA and USDA, you can put $0 down . With FHA, you can put down 3.5% . With conventional loans and many grant programs, the goal is to get you in with as little out-of-pocket as possible, sometimes 0% to 3% .

7. What is a Mortgage Credit Certificate (MCC)?

An MCC is a dollar-for-dollar reduction on your federal tax liability based on a percentage of your mortgage interest. It effectively gives you more take-home pay to help qualify for a larger loan or make your monthly payments more affordable. Many state HFA’s offer MCCs alongside their down payment programs.

8. Can I use a grant for closing costs?

Yes. Most down payment assistance programs allow the funds to be used for closing costs as well. The UMB programs, for example, explicitly offer lender credits to cover closing costs . The Western Australia HBAA grant is specifically designed to reimburse incidental expenses like settlement fees and mortgage insurance .

9. How long does it take to get approved for a grant?

The timeline varies. Some lender-specific grants can be approved quickly (within days) as part of your loan application. State programs with high demand, like California’s Dream For All, may use a lottery system with a specific application window .

10. Where can I find a HUD-approved housing counselor?

You can visit the U.S. Department of Housing and Urban Development’s website and use their “HUD Approved Housing Counseling Agency” search tool. This is a free and invaluable resource.

best cash envelope system wallets 2024

Conclusion: Your Path to Homeownership Starts Here

The dream of owning your first home is more attainable than you might think. While the headlines focus on high prices and interest rates, a parallel world of first-time home buyer grants and programs 2024 is working quietly behind the scenes to level the playing field. From federal loans that require nothing down to city-specific grants of $75,000, help is available if you know where to look.

Your next step is clear: start researching. Check your state’s housing finance agency website. Google “[Your City] down payment assistance.” Talk to a local lender who specializes in first-time buyer programs. The path to homeownership is a journey, and these programs are the guideposts that will lead you there. Your first home is waiting—go find it.