By Peyman Daneshgar

Payday loans are marketed as quick, easy solutions for emergency cash. You walk in, write a post-dated check, and walk out with money in hand. But for millions of people, that “quick fix” turns into a financial trap that can last for years. With annual percentage rates (APRs) that can exceed 400% , a small $300 loan can quickly balloon into a debt that consumes your paycheck, again and again .

If you are searching for how to get out of payday loan debt fast, you are likely feeling the pressure of relentless fees, aggressive collection calls, and the sinking feeling that you will never catch up. You are not alone, and more importantly, you are not out of options.

This guide is the most comprehensive resource available on the topic. We will walk you through the exact strategies to break the cycle, from immediate steps you can take today to long-term solutions that will secure your financial future. Whether you are dealing with one loan or multiple, have good credit or bad, this article will provide a clear, actionable roadmap to freedom.

Table of Contents

- Understanding the Payday Loan Trap

- Immediate Steps: How to Get Out of Payday Loan Debt Fast

- Consolidation Strategies: Using Lower-Interest Debt to Pay Off Payday Loans

- Professional Help: Nonprofit Credit Counseling and Debt Management Plans

- Legal Options: Consumer Proposals and Bankruptcy

- How to Build a Financial Safety Net to Avoid Future Payday Loans

- Frequently Asked Questions (FAQs)

- Conclusion: Take Control of Your Financial Future

Understanding the Payday Loan Trap

To get out of a trap, you must first understand how it works. Payday loans are designed to be difficult to escape. They are small-dollar, short-term loans, typically due on your next payday (usually within two to four weeks) . The lender does not rely on your ability to repay; they rely on your desperation and the structure of the loan itself.

The True Cost of Borrowing

The fees are where the danger lies. A typical payday loan charges $15 to $30 for every $100 borrowed . While that might not sound like much, let’s look at the math. If you borrow $300 with a $45 fee and have to repay it in two weeks, the annual percentage rate (APR) is nearly 400% . In comparison, even a high-limit credit card might charge 25% or 30%.

how to save money on a tight income

The Rollover Cycle

The real problem begins when you cannot repay the full amount on your due date. The lender will offer you a “rollover,” where you pay another fee to extend the loan for another two weeks . According to the Consumer Financial Protection Bureau (CFPB), more than 80% of payday loans are rolled over or followed by another loan within 14 days . If you roll that $300 loan over four times, you could pay over $225 in fees without reducing your principal balance by a single dollar .

Why It Feels Impossible

You are essentially paying exorbitant interest just to stay afloat. This cycle drains your bank account, making it impossible to save money or pay other bills, which leads to… another payday loan. It is a vicious, self-perpetuating cycle.

money saving challenges for couples

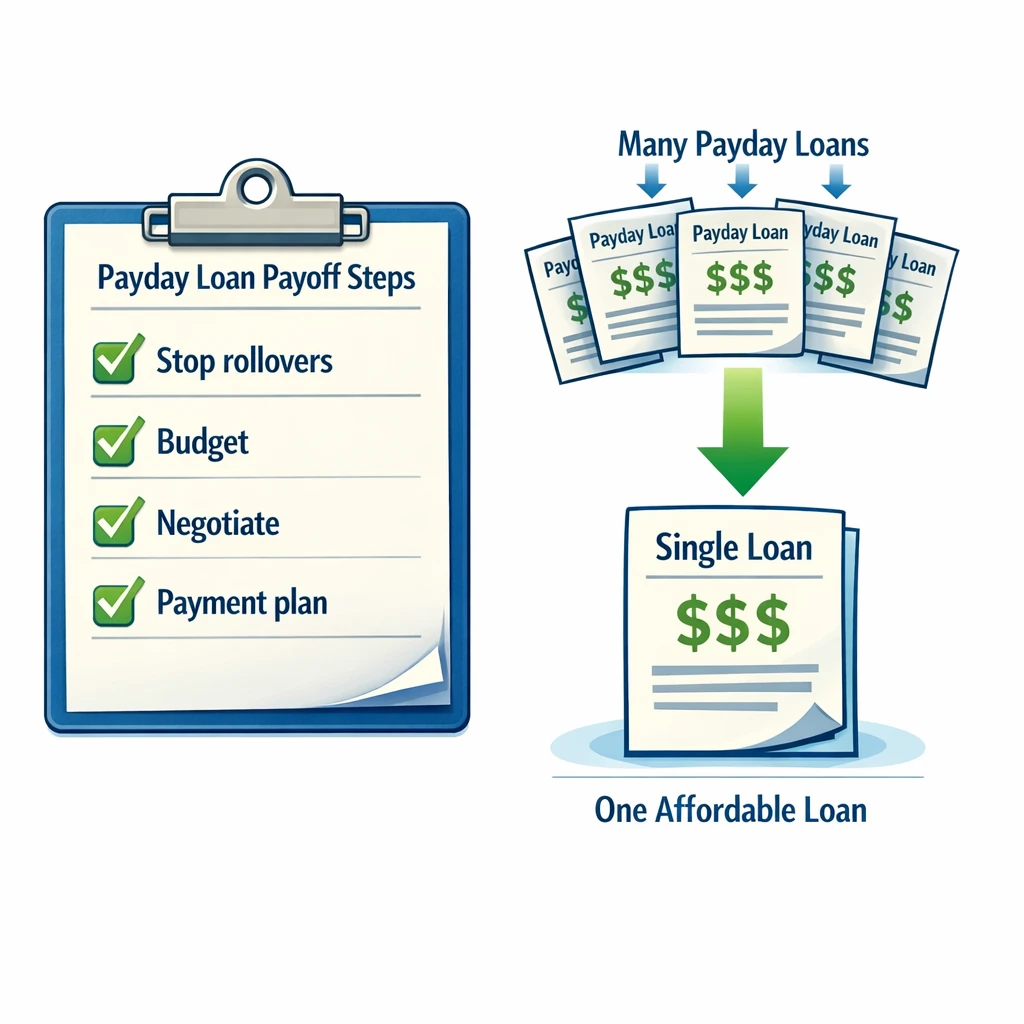

Immediate Steps: How to Get Out of Payday Loan Debt Fast

When you are in a crisis, you need to act immediately. These steps are designed to stop the bleeding and put you in a position of control.

1. Stop the Rollover Cycle

The most critical rule is this: Do not take out a new payday loan to pay off an existing one. This is the equivalent of digging a hole to fill a hole. It only adds more fees and makes your situation worse . You must commit to breaking the chain, even if it means facing some uncomfortable financial realities head-on.

2. Revoke ACH Authorization to Protect Your Bank Account

When you took out the loan, you likely signed an authorization allowing the lender to withdraw money directly from your bank account via ACH (Automated Clearing House). If you are worried about the lender cleaning out your account and causing overdraft fees, you can stop this.

You have the right to revoke this authorization. Send a written letter to both your payday lender and your bank, revoking permission for electronic withdrawals. The CFPB has also introduced new protections; as of March 2025, lenders cannot attempt to withdraw money from your account more than twice if those attempts fail . Stopping automatic withdrawals gives you control over when and how you pay, rather than letting the lender take money you need for rent or food .

3. Contact Your Lender to Negotiate a Repayment Plan

This may feel intimidating, but lenders are often willing to work with you. They would rather receive a steady payment plan than send your debt to collections, where they might recover nothing .

Call your lender and be honest. Tell them you are struggling and want to pay off the debt, but you cannot do it in a lump sum.

- Ask for an Extended Repayment Plan (ERP): Some states require lenders to offer these plans, which allow you to pay the loan back in smaller installments over a longer period (e.g., four months) .

- Negotiate Fees: Ask if they will waive some of the late fees or rollover fees to help you get back on track.

- Get it in Writing: If they agree to a plan, make sure you get the terms in writing so there is no confusion later.

- sinking funds: what are they and how to set them up

Consolidation Strategies: Using Lower-Interest Debt to Pay Off Payday Loans

The math of payday loans is simple: they win if you keep paying 400% interest. You win if you can replace that debt with something cheaper. Debt consolidation is the process of taking out a new loan (with a lower rate) to pay off the high-cost payday loans .

Debt Consolidation Loans

If you have decent credit—or even fair credit—you may qualify for a personal loan from an online lender, bank, or credit union .

- How it works: You borrow enough to pay off your payday loans entirely. You then repay the personal loan in fixed monthly installments over one to five years.

- The Benefit: Personal loan APRs typically range from 6% to 36%, which is exponentially lower than 400% . This turns an unmanageable debt into a predictable, affordable payment.

- Watch out for: Origination fees (usually 1% to 10% of the loan amount), which are deducted from your funds .

Payday Alternative Loans (PALs) from Credit Unions

If traditional banks have turned you down, credit unions are a fantastic resource. The National Credit Union Administration (NCUA) allows federal credit unions to offer Payday Alternative Loans (PALs) .

- How it works: These are small-dollar loans designed specifically to help people escape payday debt.

- The Benefit: Loan amounts range from $200 to $1,000, with repayment terms of one to six months. The interest rate is capped at 28% —a fraction of what payday lenders charge .

- Requirement: You generally need to be a credit union member for a short period, but many credit unions make it easy to join.

- best cash envelope system wallets 2024

Balance Transfer Credit Cards

If you have a credit card with an available limit, or if you can qualify for a new balance transfer card, this can be a powerful tool .

- How it works: You transfer the debt (via a cash advance or balance transfer) to a credit card, preferably one with a 0% introductory APR offer.

- The Benefit: A 0% APR period (often 12-21 months) means 100% of your payment goes toward the principal, not interest.

- Watch out for: Balance transfer fees (typically 3% to 5%) and cash advance fees. Ensure the math works in your favor .

Borrowing from Family or Friends

This is often an uncomfortable conversation, but it is usually better than paying 400% interest.

- How it works: Ask a trusted loved one for a loan to pay off the payday lender.

- The Benefit: They will likely charge 0% interest, giving you a clean slate.

- The Risk: Money can strain relationships. Treat this like a business transaction. Put the terms in writing and commit to a repayment schedule to preserve the trust .

Professional Help: Nonprofit Credit Counseling and Debt Management Plans

If you feel overwhelmed or cannot qualify for a loan, it is time to call in the experts. Nonprofit credit counseling agencies exist to help people exactly in your situation .

How a Credit Counselor Can Help

A certified credit counselor will review your entire financial situation—income, expenses, and total debt—for free. They can help you create a realistic budget and discuss options you may not have considered .

Debt Management Plan (DMP)

If your payday loans are part of a larger debt problem (including credit cards), a Debt Management Plan might be the answer.

zero-based budgeting vs. 50/30/20 rule

- How it works: The credit counseling agency negotiates with your creditors, including payday lenders, to lower interest rates or waive fees. You then make a single monthly payment to the agency, which distributes the funds to your creditors .

- The Benefit: You don’t need good credit to qualify. This can stop collection calls and help you become debt-free in 3-5 years .

Organizations like the Credit Counselling Society, InCharge Debt Solutions, or the National Foundation for Credit Counseling (NFCC) are reputable places to start .

Legal Options: Consumer Proposals and Bankruptcy

If your debt is so severe that you cannot see a way out even with a budget, or if your wages are being garnished, legal solutions exist. These are serious steps with long-term consequences, but they provide a fresh start when nothing else will.

Consumer Proposal (Canada) / Debt Settlement (US)

This is a legally binding agreement negotiated by a Licensed Insolvency Trustee (in Canada) or a debt settlement company (in the US) .

- How it works: You agree to pay a portion of your debt back (e.g., 30% to 50%), and the rest is forgiven.

- The Benefit: It stops all interest and collection calls.

- The Risk: It will significantly impact your credit score for several years, but less so than bankruptcy.

- how to save for a house down payment in 2 years

Bankruptcy

This is the absolute last resort. If your payday loan debt is just one part of a mountain of unmanageable debt, bankruptcy can discharge (eliminate) most of it .

- The Benefit: It wipes the slate clean legally.

- The Risk: It severely damages your credit for 6-7 years, can affect employment, and may require you to surrender certain assets.

How to Build a Financial Safety Net to Avoid Future Payday Loans

Getting out of debt is only half the battle. To stay out, you must build a buffer so that the next emergency doesn’t send you running back to the payday lender.

Create a Realistic Budget

Write down every dollar that comes in and every dollar that goes out. Apps or simple spreadsheets can help. Knowing where your money is going is the first step to controlling it .

Start a “Baby” Emergency Fund

Saving money when you are in debt seems impossible, but even $500 set aside can prevent a crisis. Start small. Save $5 or $10 a week. Cut one streaming service. Sell an unused item. Having cash on hand means you won’t need a loan when the car breaks down .

Explore Earned Wage Access (EWA)

Instead of a payday loan, apps like EarnIn allow you to access money you have already earned before payday. This is not a loan; there is no interest, no credit check, and no mandatory fees. It is simply getting your own money earlier to cover a gap .

Utilize Community Resources

Before borrowing, check if you qualify for help from local churches, charities, or government assistance programs. Many organizations offer food, fuel, or rental assistance that can free up cash in your budget .

Frequently Asked Questions (FAQs)

1. Can I just stop paying my payday loan?

You can, but there are serious consequences. The lender may charge late fees, send your account to collections, sue you, and attempt to garnish your wages. It will also damage your credit score . It is better to negotiate a payment plan than to ignore the debt.

how to stop impulse buying online

2. Are there payday loan forgiveness programs?

True “forgiveness” programs are rare. Payday lenders rarely forgive debt unless you go through a legal process like bankruptcy or a consumer proposal. However, some state-specific programs and hardship plans can offer relief by waiving fees or extending terms .

3. How can I stop a payday lender from taking money from my account?

You can revoke ACH authorization. Send a written notice to the lender and your bank stating that you are withdrawing permission for them to electronically debit your account. Under CFPB rules, after two failed attempts, the lender cannot try again without your renewed permission .

how to open a brokerage account for the first time

4. What is the best alternative to a payday loan?

The best alternatives include:

- Payday Alternative Loans (PALs) from credit unions (capped at 28% APR) .

- Earned Wage Access apps (access your own pay early) .

- A small personal loan from an online lender or bank .

- Asking your employer for a paycheck advance.

5. Can I consolidate payday loans with bad credit?

Yes. While you may not qualify for a top-tier bank loan, you can explore credit union PALs, which are designed for people with low credit scores. Additionally, a nonprofit Debt Management Plan (DMP) does not require a credit check and can consolidate payments .

6. How do I negotiate with a payday lender?

Call them before the due date. Explain that you are facing financial hardship and cannot pay the full amount. Ask if they offer an Extended Repayment Plan (ERP). Be honest about what you can afford to pay each month. If they refuse, contact a nonprofit credit counselor for help negotiating .

7. Will a payday loan consolidation loan hurt my credit?

Initially, applying for a new loan may cause a small, temporary dip in your credit score due to the hard inquiry. However, if you make your new loan payments on time, it will help build a positive payment history and improve your score over the long term .

what is dollar-cost averaging and how to set it up

8. What is the new CFPB rule on payday loans in 2025/2026?

As of March 30, 2025, new protections took effect. Lenders cannot attempt to withdraw funds from your bank account more than twice unsuccessfully. This rule is designed to prevent the avalanche of overdraft fees that often accompany payday lending .

Conclusion: Take Control of Your Financial Future

Learning how to get out of payday loan debt fast is not just about making a single phone call; it is about changing your relationship with money. The cycle of high-cost debt is designed to keep you trapped, but you now have the roadmap to escape.

Start with the immediate steps: protect your bank account and talk to your lender. Then, look at the math. Replace that 400% interest debt with something manageable, whether it is a credit union loan, a consolidation loan, or a nonprofit Debt Management Plan. Finally, commit to building a small savings cushion so you never have to rely on a payday loan again.

You have the power to break the cycle. It will take discipline and courage, but financial freedom is waiting on the other side. Take the first step today.