By Peyman Daneshgar

If you are carrying credit card debt at an interest rate of 20% or higher, you are likely watching a significant portion of your monthly payment disappear into thin air. It feels like running on a treadmill—you are making payments, but the balance isn’t shrinking fast enough. For millions of consumers, a balance transfer card offers a way off that treadmill.

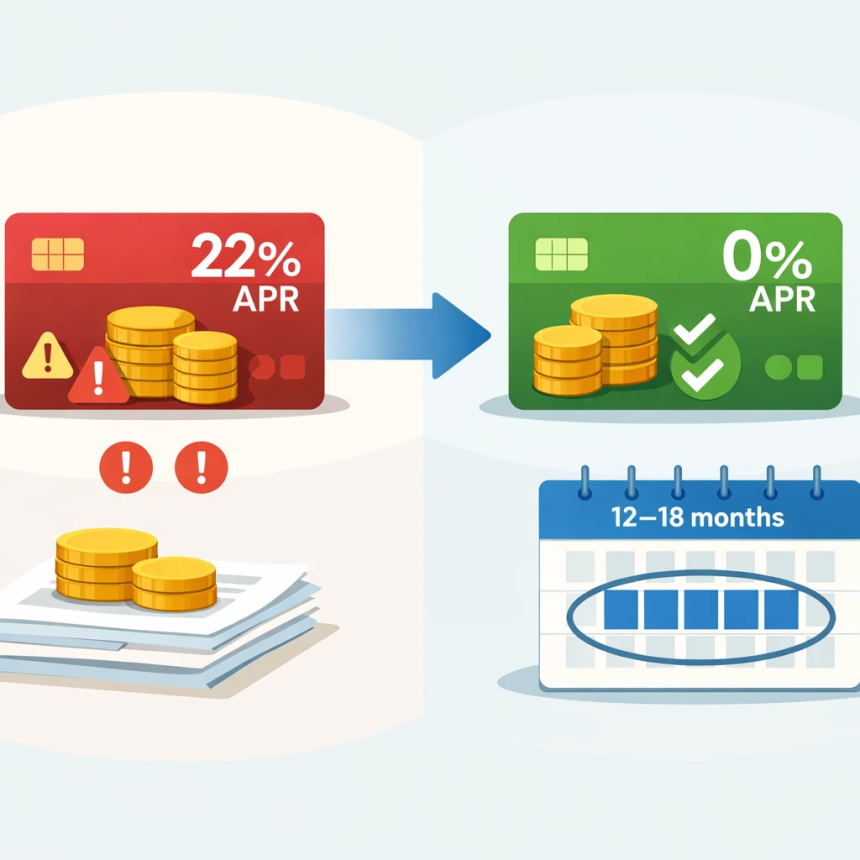

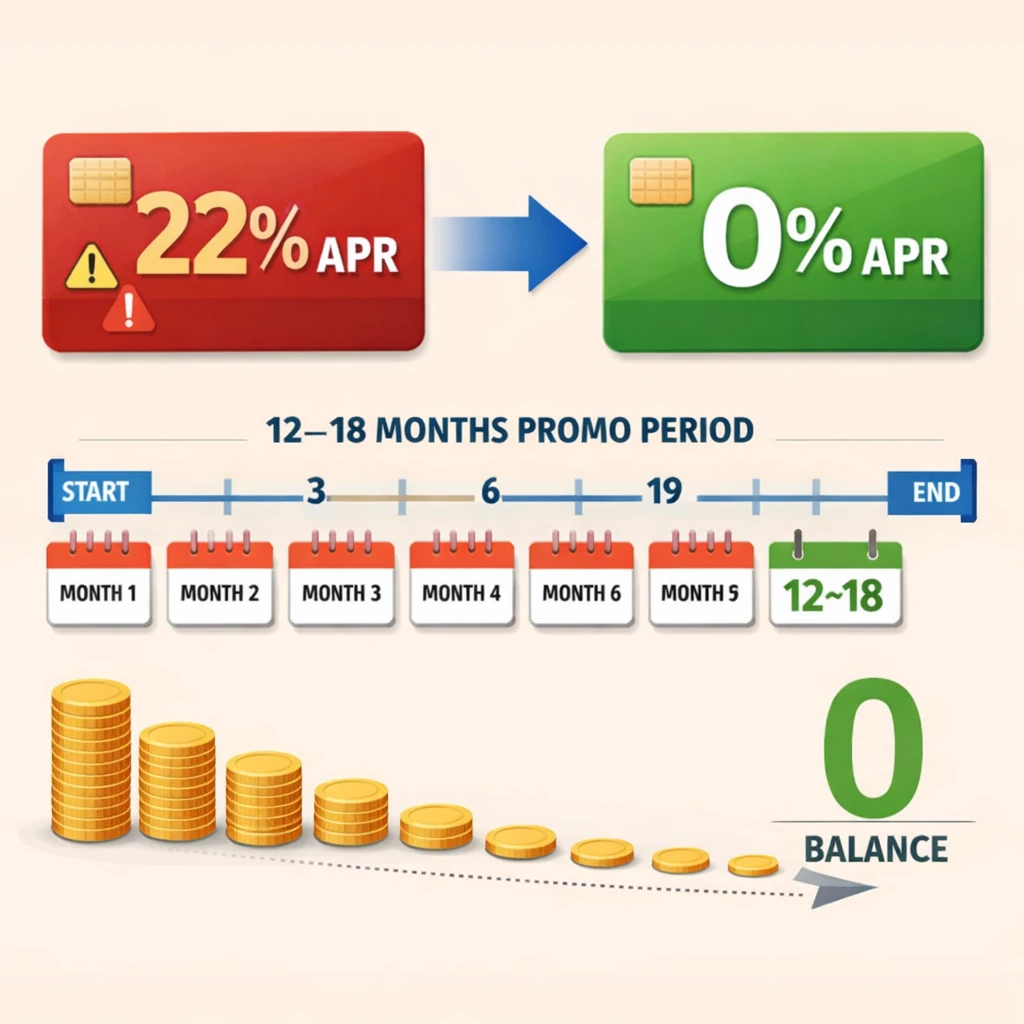

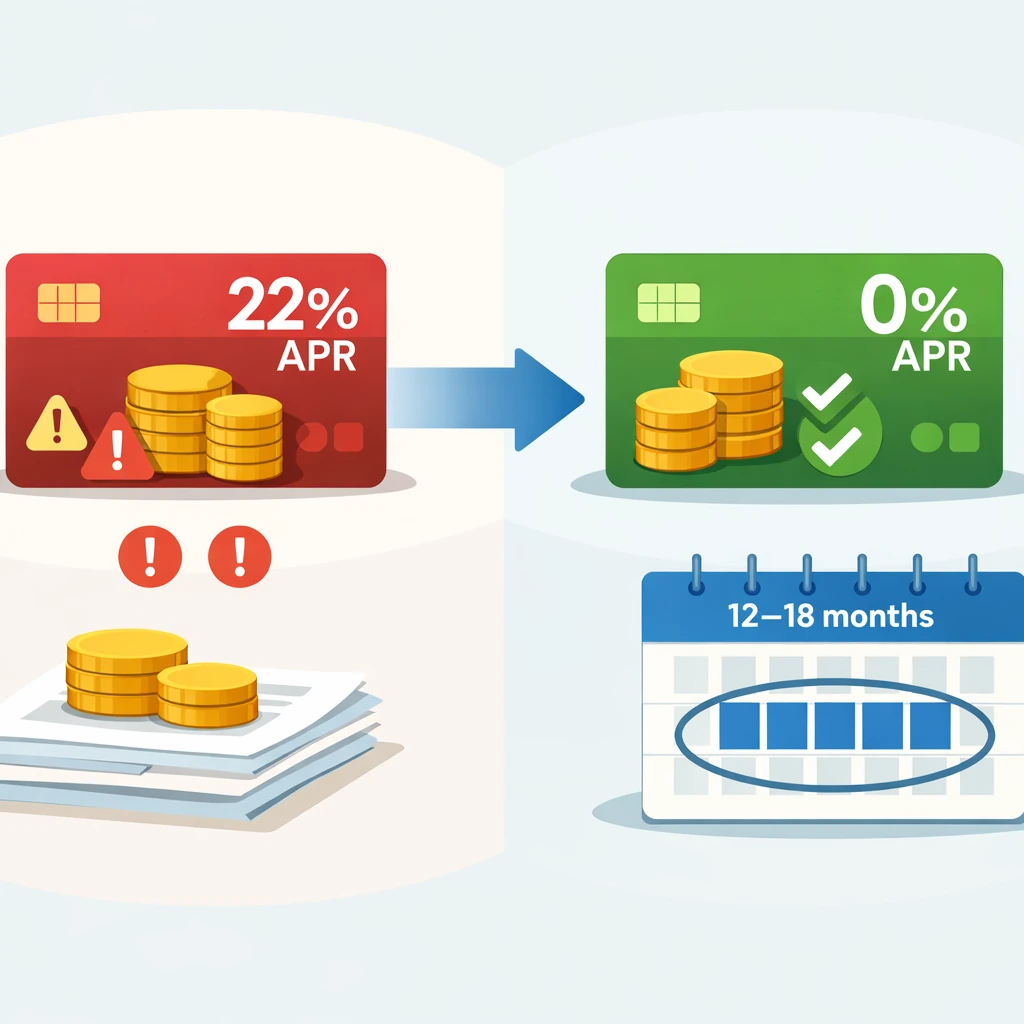

A balance transfer allows you to move existing high-interest debt to a new credit card, ideally one with a 0% introductory annual percentage rate (APR) . This means that for a set period—often 12 to 21 months, and in some cases up to 38 months—every dollar you pay goes directly toward reducing your principal balance, not lining the pockets of the bank with interest .

However, here is the critical truth: a balance transfer card is a powerful financial tool, but it is not magic. If used incorrectly, it can actually make your debt situation worse. The key lies in understanding exactly how to use a balance transfer card wisely.

This comprehensive guide is designed to be the only resource you will ever need on this topic. We will walk you through the mechanics, the math, the potential pitfalls, and the proven strategies to ensure that a balance transfer becomes the turning point in your journey to becoming debt-free.

Table of Contents

- What is a Balance Transfer Card?

- The 2026 Landscape: Why Now is a Great Time to Transfer

- Step 1: Do the Math—Is a Balance Transfer Worth It?

- Step 2: Choosing the Right Card for Your Situation

- Step 3: The Application and Transfer Process

- The Golden Rules: How to Use a Balance Transfer Card Wisely

- The Single Biggest Mistake People Make

- Advanced Strategies: Multiple Transfers and “Rate Chasing”

- What If You Can’t Get a 0% Card?

- Frequently Asked Questions (FAQs)

- Conclusion: Your Path to Debt Freedom

What is a Balance Transfer Card?

A balance transfer credit card is a standard credit card that offers a special promotional period, typically with a 0% APR on balances transferred from other cards . Think of it like this: you owe money to Card A at 22% interest. You apply for Card B, which offers 0% for 18 months. Card B pays off Card A on your behalf. Now, instead of owing Card A, you owe Card B the same amount, but with one crucial difference—you have 18 months to pay it off without accruing a single penny in interest .

This process is designed to help consumers consolidate debt and save money on interest, accelerating the path to being debt-free .

sinking funds: what are they and how to set them up

The 2026 Landscape: Why Now is a Great Time to Transfer

If you are considering a balance transfer in 2026, you are in luck. The market for 0% balance transfer cards is incredibly competitive right now.

According to recent data, the average length of a 0% balance transfer period rose to a three-year high at the end of 2025. In December 2024, the average introductory period was just 512 days. By December 2025, that average had jumped to 585 days (approximately 19.5 months) .

Some of the market leaders are offering even more breathing room. Barclaycard and Tesco Bank, for example, have increased their 0% balance transfer periods to a market-leading 36 months . This means eligible borrowers could have up to three full years to pay off their debt without incurring any interest charges—a massive opportunity to get ahead.

However, it’s not all good news. The average balance transfer fee has crept up slightly, from 2.44% to 2.51% over the same period . This makes it more important than ever to do the math before you apply.

zero-based budgeting vs. 50/30/20 rule

Step 1: Do the Math—Is a Balance Transfer Worth It?

Before you apply for any card, you must calculate whether the transfer will actually save you money. The two main factors are the balance transfer fee and the promotional period.

The Fee Calculation

Most cards charge a fee of 3% to 5% of the amount you transfer . If you are transferring $5,000, a 3% fee costs you $150 upfront. This fee is typically added to your new balance.

Is it Worth It?

Ask yourself: Will the interest you save during the 0% period be greater than the transfer fee?

- Example: You have $5,000 at 22% APR. If you pay $250 a month, you will pay about $1,535 in interest over 27 months .

- With a Transfer: You pay a $150 fee (3%) and have 18 months at 0%. If you pay $286 a month, you pay it off in 18 months with $0 interest. You save $1,385 (minus the $150 fee = $1,235 net savings).

If you cannot pay off the balance within the 0% period, the remaining balance will be subject to the card’s standard APR (often 20% to 25%), and your savings will evaporate .

how to save for a house down payment in 2 years

Step 2: Choosing the Right Card for Your Situation

Not all balance transfer cards are created equal. To use a balance transfer card wisely, you must match the card’s features to your financial plan .

1. The Length of the 0% Period

- If you need a long time: Look for cards offering 18 to 21 months (or even 36 months, depending on your location and credit) . These are best if you need smaller monthly payments.

- If you can pay quickly: A shorter 0% period (12-15 months) often comes with a lower transfer fee, sometimes even 0% .

2. The Balance Transfer Fee

- Longer terms usually have higher fees (3% to 5%) .

- Shorter terms sometimes have no fee at all. If you can clear the debt in under a year, a no-fee card is the absolute cheapest option .

3. The Post-Promotional APR (The “Go-To” Rate)

While you plan to pay off the balance before the promo ends, life happens. Look at the standard APR that will apply after the 0% period. A lower “go-to” rate is a safety net .

4. Check Your Eligibility

Before applying, use an eligibility calculator. In the UK, sites like MoneySavingExpert offer tools that show your chances of approval without affecting your credit score . In the US, many bank sites offer pre-approval tools. Applying for cards you are unlikely to get results in hard inquiries that can lower your score .

how to stop impulse buying online

Step 3: The Application and Transfer Process

Once you have chosen a card, follow these steps to ensure the transfer goes smoothly .

- Apply for the Card: Complete the application. You will need the details of your existing debt.

- Request the Transfer: You can usually request a balance transfer during the application process. You will need the account number and the amount you wish to transfer from your old card .

- Know the Window: Most cards require you to complete the transfer within a specific window (e.g., 60 to 90 days of account opening) to qualify for the 0% rate. Do not delay! .

- Wait for Processing: Transfers typically take a few days to a couple of weeks . Crucially, continue making payments on your old card until the transfer is complete to avoid late fees and damage to your credit score .

- what is dollar-cost averaging and how to set it up

The Golden Rules: How to Use a Balance Transfer Card Wisely

Getting the card is the easy part. Using it wisely requires discipline. Here are the non-negotiable rules to follow .

Rule 1: Create a Hardcore Payoff Plan

A 0% APR is a gift of time, but it is ticking. Do not just “pay what you can.”

- Calculate your monthly payment: Take your total debt (including the transfer fee) and divide it by the number of months in the 0% period.

- Example: $5,150 debt / 18 months = $286 per month.

- Set up an automatic payment for this amount. Treat it like a non-negotiable bill .

Rule 2: Never, Ever Miss a Payment

Missing a payment can have severe consequences. It may trigger a penalty APR (which could be as high as 29.99%) and cause you to lose your 0% promotional offer immediately . Always set up autopay for at least the minimum payment as a backup.

Rule 3: Stop Using the Card for New Purchases

This is the most common trap. You transfer a balance to a 0% card, but then you start using that same card for everyday spending.

- The Problem: Payments you make typically go toward the lowest-interest balance first (your transferred debt). Your new purchases sit there accruing interest at the regular purchase APR (which is rarely 0%) .

- The Solution: Use your balance transfer card exclusively as a debt repayment tool. Keep it in a drawer. Use a different card or cash for daily expenses.

Rule 4: Don’t Close Your Old Card (Yet)

Once the transfer is complete, you might be tempted to close the old account. This can actually hurt your credit score.

- Credit Utilization: Closing a card reduces your total available credit, which can increase your overall credit utilization ratio and lower your score .

- The Strategy: Keep the old account open, but cut up the physical card to avoid using it. This preserves your credit history length and available credit .

- how to open a brokerage account for the first time

The Single Biggest Mistake People Make

According to financial experts, the single biggest mistake people make with balance transfer cards is treating the 0% APR window as a permanent solution rather than a short-term opportunity .

When people see that their debt isn’t growing, they lose the sense of urgency. They relax. They make only the minimum payment. They might even start spending again because the “pressure is off.”

The result? When the 0% period ends, they still owe thousands of dollars, and suddenly that debt is accruing interest at 25% again. They are right back where they started, but now with another hard inquiry on their credit report .

How to avoid it: Treat the 0% period as a ticking clock. Write down the end date on your calendar. Remind yourself every month that the goal is a zero balance by that date.

how to start investing with $100 or less

Advanced Strategies: Multiple Transfers and “Rate Chasing”

For disciplined borrowers, there is a strategy known as “rate surfing” or “chasing” 0% offers.

How It Works

If you have a large debt that you cannot pay off within a single 0% period, you can transfer the remaining balance to another new 0% APR card when the first promotional period ends .

The Benefits

- Extended Interest-Free Time: You can effectively keep your debt at 0% for years by moving it from card to card.

- Debt Consolidation: You can continue to save on interest while you chip away at the principal.

The Risks

- Transfer Fees: You will pay a 3-5% fee each time you transfer. Over multiple transfers, these fees add up .

- Credit Score Impact: Each new card application results in a hard inquiry, which temporarily lowers your score. Opening multiple new cards also lowers the average age of your accounts .

- The “Trap”: This strategy requires flawless organization and credit discipline. If you miss a payment or time it wrong, you could get stuck with high interest.

Verdict: Multiple transfers can work, but they are best reserved for those with excellent credit and a very clear, long-term payoff plan.

What If You Can’t Get a 0% Card?

Balance transfer cards with the best 0% offers are typically reserved for people with good to excellent credit (scores generally above 670) . If you don’t qualify, or if you don’t think you can pay off the balance in time, consider these alternatives .

1. Personal Loan (Debt Consolidation Loan)

A personal loan from a bank, credit union, or online lender provides a lump sum of cash at a fixed interest rate. You use it to pay off your credit cards.

- Pros: Fixed monthly payment, fixed payoff date, and interest rates (while not 0%) are often much lower than credit card rates (e.g., 8% to 15%) .

- Cons: Requires a credit check, and you may have to pay an origination fee.

2. Credit Counseling / Debt Management Plan (DMP)

If your debt feels overwhelming, contact a nonprofit credit counseling agency .

- How it works: A counselor negotiates with your creditors to lower your interest rates (sometimes to 7% or 8%). You make a single monthly payment to the agency, which distributes the funds.

- Pros: You don’t need perfect credit, and you get professional support.

- Cons: You may have to close your credit card accounts, which can temporarily hurt your score.

3. 0% Purchase Cards (for new spending)

If your goal is to manage new expenses, look for a card with a 0% intro APR on purchases, not just balance transfers. This can help you spread the cost of a large purchase over time without interest .

best stocks for dividend income for beginners

Frequently Asked Questions (FAQs)

1. Will a balance transfer hurt my credit score?

Initially, yes, it may cause a small, temporary dip. Applying for a new card results in a hard inquiry (usually a 5-10 point drop) . Opening a new account also lowers your average account age. However, in the long term, if you use the card to pay down debt and lower your credit utilization, your score will likely improve .

2. How long does a balance transfer take?

It typically takes 5 to 14 days for a balance transfer to process, depending on the card issuers involved . Keep paying your old card until you see the balance is zero.

3. Can I transfer a balance from a card to another card from the same bank?

Generally, no. Most issuers do not allow you to transfer a balance between two cards that they themselves issue . You need to transfer the debt to a card from a different bank.

4. What happens if I don’t pay off the balance before the 0% period ends?

When the promotional period ends, the standard purchase APR (which could be 20% to 25%) will apply to any remaining balance . You will then start accruing interest on that balance every month.

5. Can I transfer a balance from a store card or a loan?

Most balance transfer cards are designed for credit card debt. However, some issuers allow you to transfer balances from store cards or even personal loans, but this is less common. Check the specific card terms .

6. What is the difference between a balance transfer and a money transfer?

A balance transfer moves debt from one credit card to another. A money transfer involves borrowing cash from your credit card into your bank account. Money transfers often come with their own fees and interest rates and are used for paying off overdrafts or other non-card debt .

7. Is it better to get a long 0% term with a fee or a short term with no fee?

It depends on your repayment speed .

- If you can pay off the debt in under a year, a no-fee, shorter-term card is mathematically better.

- If you need more than a year, it is worth paying a fee for a longer 0% term to guarantee you avoid high interest later.

8. Can I use my balance transfer card for purchases?

You can, but it is not wise if you are carrying a transferred balance . Payments are usually applied to the lowest-interest portion first (your transferred debt), meaning your new purchases will sit there accruing interest at the standard purchase rate. Keep the card strictly for repayment.

9. How much should I pay each month?

To use a balance transfer card wisely, you should calculate Total Debt (including fees) ÷ Months of 0% APR. Paying this amount each month ensures you will hit zero right as the interest kicks in .

10. What should I do if my balance transfer is denied?

If you are denied, check the reason. It may be due to your credit score, income, or existing debt levels. Your next steps could be: checking your credit report for errors, paying down some debt to lower your utilization, or looking into a debt consolidation loan or credit counseling as alternatives .

Conclusion: Your Path to Debt Freedom

A balance transfer card is one of the most effective weapons available in the fight against high-interest debt. When used correctly, it can save you thousands of dollars, simplify your finances, and give you a clear, defined timeline to becoming debt-free.

The key takeaway is this: the card is merely the tool. Your discipline is the engine. By doing the math, choosing the right card, creating a strict payoff plan, and avoiding the temptation to spend, you can transform a 0% APR offer from a temporary bandage into a permanent solution.

Take control of your debt today. Review your balances, check your credit score, and find the card that fits your timeline. The path to financial freedom is paved with smart decisions—and using a balance transfer card wisely is one of the smartest you can make.