The Ultimate Guide to FHA Loan vs Conventional Loan Requirements (2026)

By Peyman Daneshgar

Choosing the right mortgage is one of the most consequential financial decisions you will ever make. For most homebuyers, the choice ultimately comes down to two popular options: an FHA loan or a conventional loan. While both can help you finance a home, they operate under very different rules, costs, and qualification criteria.

The question isn’t which loan is “better” in a general sense—it’s which loan is better for your unique financial situation. An FHA loan might be your only path to homeownership if you have a lower credit score or limited savings. A conventional loan could save you thousands over the long term if you have strong credit and a solid down payment.

This guide is the definitive resource for understanding FHA loan vs conventional loan requirements in 2026. We will break down every requirement, compare costs, analyze the latest 2026 updates, and provide clear guidance to help you make an informed decision. By the end, you’ll know exactly which loan type aligns with your financial goals.

Table of Contents

- What Are FHA Loans and Conventional Loans?

- FHA Loan vs Conventional Loan Requirements: Quick Comparison

- Credit Score Requirements

- Down Payment Requirements

- Debt-to-Income Ratio (DTI) Requirements

- Mortgage Insurance: FHA MIP vs Conventional PMI

- Loan Limits for 2026

- Property Requirements and Occupancy

- Which Loan is Cheaper? A Cost Comparison

- FHA Loan vs Conventional Loan: Pros and Cons

- How to Choose the Right Loan for You

- The 2026 Credit Score Changes: What Borrowers Need to Know

- Frequently Asked Questions (FAQs)

- Conclusion: Making Your Decision

What Are FHA Loans and Conventional Loans?

Before diving into the requirements, it’s essential to understand the fundamental difference between these two loan types.

FHA Loans (Government-Backed)

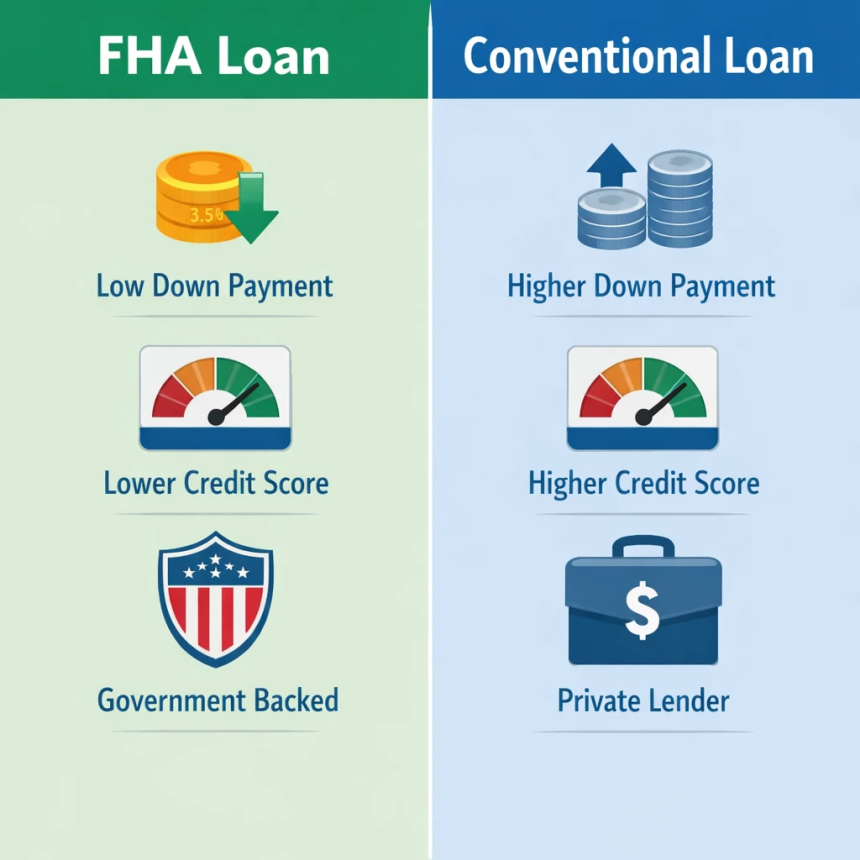

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD) . The FHA doesn’t lend money directly; instead, it provides insurance to private lenders, protecting them if a borrower defaults. This insurance reduces the risk for lenders, allowing them to offer loans to borrowers who might not qualify for conventional financing .

Because the government backs these loans, they feature more flexible credit requirements, lower down payments, and higher debt tolerance . They are particularly popular among first-time homebuyers.

how much house can I afford on a $70,000 salary?

Conventional Loans (Not Government-Backed)

A conventional loan is a mortgage that is not insured or guaranteed by a government agency . These loans are originated and funded by private lenders and are often sold to government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac . Because the government does not back them, lenders take on more risk, which typically translates to stricter qualification requirements .

Conventional loans are the most popular type of mortgage in the United States, accounting for the majority of home loans . Borrowers with strong credit and a solid down payment often find conventional loans to be more cost-effective over the long term.

first-time home buyer grants and programs 2024

FHA Loan vs Conventional Loan Requirements: Quick Comparison

Here is a side-by-side comparison of the core requirements for FHA and conventional loans in 2026.

| Requirement | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Credit Score | 580 for 3.5% down; 500-579 for 10% down | 620 (typical); no official minimum, but lender standards apply |

| Minimum Down Payment | 3.5% | 3% for first-time buyers; 5% for others |

| Maximum DTI Ratio | Up to 50% with compensating factors; 43% standard | 36% preferred; up to 43-45% typically; 50% for some programs |

| Mortgage Insurance | Upfront MIP (1.75%) + Annual MIP (0.15%-0.75%) | PMI required if down payment <20% |

| Mortgage Insurance Removal | MIP for life if down payment <10%; after 11 years if ≥10% down | PMI cancels automatically at 22% equity; can request at 20% |

| 2026 Loan Limits (Most Areas) | $541,287 (floor); $1,249,125 (ceiling) | $832,750 (conforming limit) |

| Property Type | Primary residence only; 1-4 units | Primary residence, second home, investment property |

| Property Standards | Stricter FHA appraisal and property requirements | Less stringent; based on lender and property type |

Credit Score Requirements

Your credit score is often the first hurdle in the mortgage approval process. The requirements differ significantly between FHA and conventional loans.

FHA Credit Score Requirements

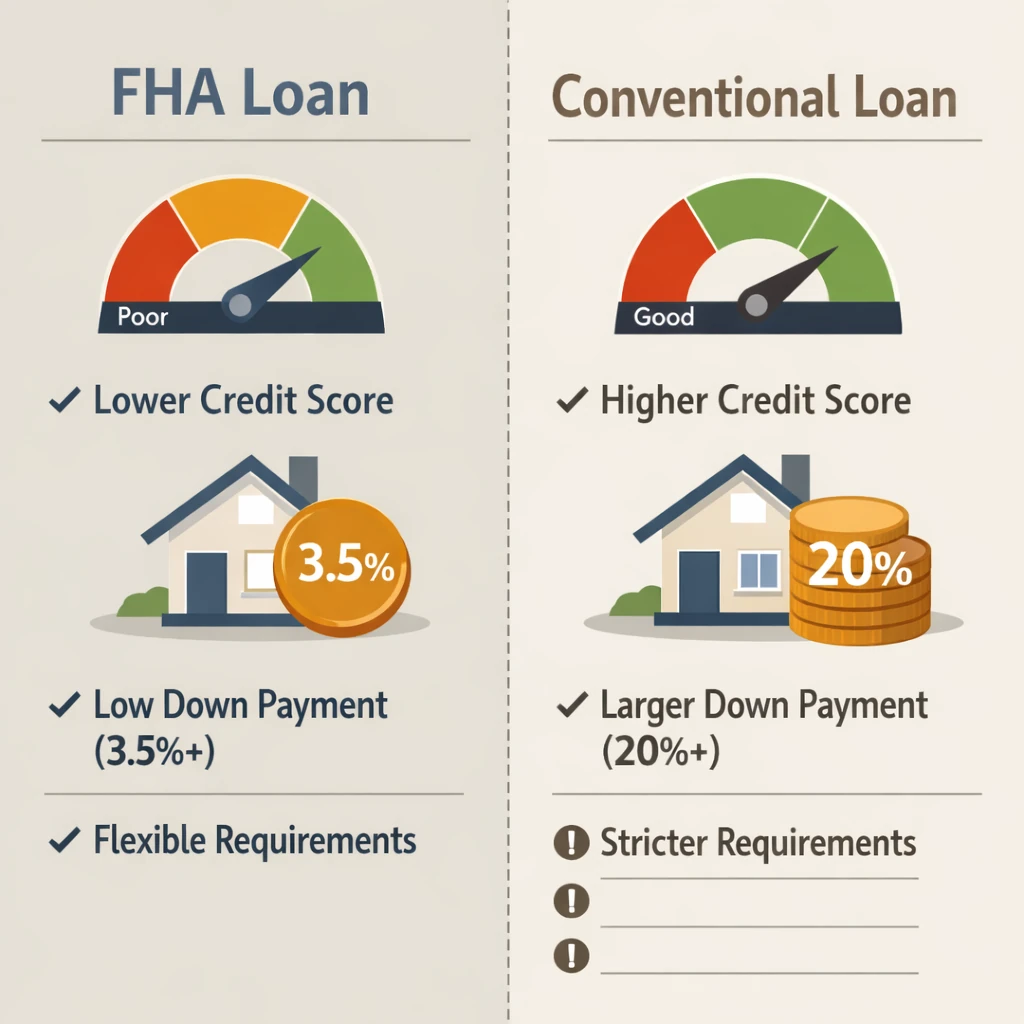

FHA loans are renowned for their flexibility with credit scores . The official HUD guidelines state:

- 580 or higher: You qualify for the minimum 3.5% down payment .

- 500 to 579: You may still qualify, but you must make a 10% down payment .

- Below 500: You generally will not qualify for an FHA loan through standard channels .

However, there is an important caveat: lender overlays. While the FHA sets these minimums, individual lenders can impose stricter requirements . Many lenders require a minimum credit score of 620 for an FHA loan, even though the FHA technically allows lower scores . This means you need to shop around for a lender willing to work with your specific credit profile.

is debt consolidation a good idea?

Conventional Credit Score Requirements

Conventional loans have traditionally required a minimum credit score of 620 . However, 2026 brings significant changes to this landscape.

Historically, a 620 score was the firm threshold. But as of late 2025, Fannie Mae has eliminated its minimum credit score requirement . This doesn’t mean anyone can get a loan; it means the risk assessment is now based on “a broad set of factors, such as borrower reserves, debt levels, property characteristics, and loan purpose” . Freddie Mac is following suit with new credit modeling .

In practice, most lenders still look for scores in the 620-640 range for conventional loans. Borrowers with scores below this may struggle to find a lender, even with the new FHFA guidelines. The key takeaway: a higher credit score (think 740+) will always get you the best interest rates on a conventional loan .

Winner for Low Credit Scores: FHA Loan.

how to talk to creditors when you can’t pay

Down Payment Requirements

The amount of cash you need upfront is another critical differentiator.

FHA Down Payment

The FHA program is designed to minimize the upfront cash required .

- Minimum down payment: 3.5% of the purchase price for borrowers with credit scores of 580 or higher .

- Down payment for scores 500-579: 10% .

FHA also allows the down payment to come from gift funds from family members, employers, or approved nonprofits, making it easier to assemble the necessary cash .

Conventional Down Payment

Conventional loans offer more variety in down payment options .

- Minimum down payment for first-time buyers: As low as 3% through Fannie Mae’s HomeReady® or Freddie Mac’s HomeOne® programs .

- Minimum down payment for repeat buyers: Typically 5% .

- The 20% ideal: Putting 20% down is the “gold standard” because it allows you to avoid paying Private Mortgage Insurance (PMI) entirely .

Like FHA, conventional loans allow down payment funds to come from gifts, though the source restrictions may be slightly tighter .

Winner for Low Down Payment: Tie. Both offer 3-3.5% down options.

government programs for medical debt relief

Debt-to-Income Ratio (DTI) Requirements

Your debt-to-income ratio (DTI) compares your monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to manage monthly payments .

FHA DTI Requirements

FHA loans are known for their flexibility with DTI .

- Standard maximum: Lenders typically prefer a DTI of 43% or lower .

- With compensating factors: FHA allows DTIs up to 50%, and in some cases even 57%, if you have strong compensating factors such as significant cash reserves or a strong payment history .

Conventional DTI Requirements

Conventional loans are generally stricter on DTI .

- Ideal ratio: Lenders like to see a DTI of 36% or lower .

- Maximum: They will typically accept up to 43-45% .

- Program exceptions: Some specific programs, like Fannie Mae’s HomeReady®, may allow DTIs up to 50% for lower-income borrowers .

Winner for High DTI: FHA Loan.

how to use a balance transfer card wisely

Mortgage Insurance: FHA MIP vs Conventional PMI

Mortgage insurance protects the lender if you default. It is required on both loan types when you put down less than 20% . However, the structure and cost differ significantly.

FHA Mortgage Insurance Premiums (MIP)

FHA loans require two types of mortgage insurance :

- Upfront MIP (UFMIP): 1.75% of the base loan amount. This is typically rolled into the loan balance, so you don’t pay it out of pocket .

- Annual MIP: Ranges from 0.15% to 0.75% of the loan amount, paid in monthly installments .

When can you remove MIP? This is the crucial drawback :

- If your down payment is less than 10% , MIP lasts for the entire life of the loan (30 years).

- If your down payment is 10% or more , MIP drops off after 11 years.

Conventional Private Mortgage Insurance (PMI)

Conventional loans require PMI only if your down payment is less than 20% .

- Cost: PMI costs vary but are generally lower than FHA MIP for borrowers with good credit .

- Removal: PMI is automatically canceled once your loan-to-value (LTV) ratio reaches 78% (i.e., you have 22% equity). You can request cancellation at 80% LTV (20% equity) .

Winner for Long-Term Cost: Conventional Loan (because PMI can be removed).

Strategies to Pay Off $30,000 in Student Loans

Loan Limits for 2026

Both loan types have maximum limits that vary by county.

FHA Loan Limits for 2026

FHA loan limits are calculated as a percentage of the conforming loan limit .

- Floor limit (low-cost areas): $541,287 for a single-family home .

- Ceiling limit (high-cost areas): $1,249,125 for a single-family home .

- Special exception areas (Alaska, Hawaii, etc.): Up to $1,873,687 .

These limits represent a 3.26% increase from 2025, reflecting continued home price appreciation .

Conventional Conforming Loan Limits for 2026

The Federal Housing Finance Agency (FHFA) sets the conforming loan limits for Fannie Mae and Freddie Mac .

- Baseline limit (most areas): $832,750 for a single-family home .

- High-cost areas: Up to $1,249,125 .

- Multi-unit properties: Limits increase for 2-4 unit properties .

Loans above these limits are considered jumbo loans and have different, stricter requirements .

Winner for High Loan Amounts: Conventional (higher baseline limits).

does debt settlement hurt your credit score?

Property Requirements and Occupancy

The type of property you can buy and how you must use it also differs.

FHA Property Requirements

FHA loans have stricter property standards because the home must be safe, sound, and secure to protect the FHA’s investment .

- Minimum property standards: The home must pass an FHA appraisal that checks for safety, security, and structural soundness .

- Occupancy: You must live in the home as your primary residence. You cannot use an FHA loan for a second home or investment property .

- Property types: You can buy 1-4 unit properties, as long as you live in one of the units .

Conventional Property Requirements

Conventional loans are more flexible regarding property type .

- Property standards: While an appraisal is still required, the standards are generally less stringent than FHA’s. The focus is on market value rather than strict habitability checklists.

- Occupancy: You can use a conventional loan for a primary residence, second home, or investment property .

- Property types: Includes single-family homes, condos, townhomes, and multi-unit properties.

Winner for Flexibility: Conventional Loan.

how to get out of payday loan debt fast

Which Loan is Cheaper? A Cost Comparison

To truly understand FHA loan vs conventional loan requirements, you must look at the bottom line. Let’s compare a $400,000 home purchase with a 3.5% down payment (FHA) versus a 3% down payment (conventional) based on rates from late 2025 .

| Cost Comparison | 30-Year Fixed FHA Loan | 30-Year Fixed Conventional Loan |

|---|---|---|

| Home Price | $400,000 | $400,000 |

| Down Payment | 3.5% ($14,000) | 3% ($12,000) |

| Loan Amount | $386,000 | $388,000 |

| Interest Rate | 6.75% | 6.37% |

| Principal & Interest | $2,504 | $2,419 |

| Upfront Mortgage Insurance | $6,755 (1.75% MIP) | $0 |

| Monthly Mortgage Insurance | $177 (MIP) | $317 (PMI) |

| Total Monthly Payment (P&I + MI) | $2,861 | $2,736 |

| Interest Paid Over 30 Years | ~$515,000 | ~$483,000 |

*Data source: Bankrate *

Analysis:

In this scenario, the conventional loan has a lower monthly payment and lower total interest over the life of the loan, even though the PMI payment is higher. Why? Because the FHA loan has a higher interest rate and its mortgage insurance (MIP) is effectively permanent, whereas the conventional loan’s PMI will eventually drop off.

However, the FHA loan was accessible with a slightly lower credit score. This illustrates the trade-off: FHA offers access, while conventional offers long-term savings for those who qualify.

FHA Loan vs Conventional Loan: Pros and Cons

FHA Loan Pros

- Lower credit score requirements (as low as 500 with 10% down) .

- Higher DTI tolerance (up to 50%+) .

- Low 3.5% down payment .

- Down payment can be 100% gifted .

FHA Loan Cons

- Mortgage insurance for life if you put less than 10% down .

- Upfront mortgage insurance premium (1.75% of loan amount) .

- Stricter property standards can limit your options .

- Lower loan limits compared to conforming conventional loans .

Conventional Loan Pros

- PMI can be removed once you reach 20% equity .

- No upfront mortgage insurance .

- Higher loan limits ($832,750 baseline) .

- Flexible property types (second homes, investment properties) .

- Lower overall cost for borrowers with good credit .

Conventional Loan Cons

- Higher credit score required (typically 620+) .

- Stricter DTI limits .

- PMI can be expensive if you have a lower credit score .

- May require more cash reserves .

How to Choose the Right Loan for You

Use this decision guide to determine which path to pursue.

Consider an FHA loan if:

- Your credit score is below 620 .

- You have a higher DTI ratio (above 43%) .

- You have limited savings and need the lowest possible down payment .

- You are a first-time homebuyer with less-than-perfect credit .

- You have recently experienced a bankruptcy or foreclosure (FHA waiting periods are shorter) .

Consider a Conventional loan if:

- Your credit score is 620 or higher, ideally 740+ for the best rates .

- You can put at least 5-10% down .

- You want to avoid mortgage insurance or want a clear path to cancel it .

- You are buying a second home or investment property .

- You need a loan amount above $541,287 in most areas .

- You plan to stay in the home long-term and want to minimize total interest costs .

Many experts advise that if you qualify for both, the conventional loan is usually the better financial choice because of the lower long-term costs and easier mortgage insurance removal . However, the FHA loan remains an invaluable tool for those who cannot qualify for conventional financing.

The 2026 Credit Score Changes: What Borrowers Need to Know

2026 is a landmark year for mortgage credit scoring. The Federal Housing Finance Agency (FHFA) has mandated that Fannie Mae and Freddie Mac adopt new credit scoring models .

What’s Changing?

- New Models: Lenders will now use FICO 10T and VantageScore 4.0 , in addition to classic FICO scores .

- Trended Data: These new models use “trended data,” which analyzes your credit behavior over time (e.g., are you paying down debt or accumulating more?) .

- Alternative Data: They can also consider alternative data like rent payments, utility bills, and phone bills .

What This Means for You

- More Access: Approximately 5 million more borrowers could qualify for mortgages because their positive rent and utility payment history will now be considered .

- No More Minimum? Fannie Mae has technically eliminated its minimum credit score requirement, moving to a holistic risk assessment .

- Still Matters: Despite these changes, a higher credit score still gets you a better interest rate. The new models simply allow more people to enter the scoring system .

The bottom line: If you have a “thin” credit file or no traditional credit score, 2026 may be the year you can finally qualify for a mortgage, especially a conventional loan, by using your rent and utility payment history.

Frequently Asked Questions (FAQs)

1. Which is better, an FHA or conventional loan?

There is no universal “better” loan. FHA loans are better if you have lower credit (below 620) or higher debt. Conventional loans are better if you have good credit (620+) and want to save on long-term costs by avoiding lifetime mortgage insurance .

2. Is FHA harder to qualify for than conventional?

No. In fact, FHA loans are generally easier to qualify for because they have lower credit score minimums and higher DTI allowances .

3. Can I switch from an FHA loan to a conventional loan later?

Yes. This is a common strategy called refinancing. Many borrowers use an FHA loan to get into a home and then refinance into a conventional loan once their credit improves and they build equity, allowing them to drop the FHA mortgage insurance .

4. Do FHA loans have higher interest rates?

Not necessarily. FHA loan interest rates can sometimes be lower than conventional rates because the government backing reduces risk for lenders . However, when you add the mandatory mortgage insurance premiums, the total monthly payment on an FHA loan can be higher than a conventional loan’s payment .

5. What is the minimum down payment for an FHA vs conventional loan?

FHA requires 3.5% down for borrowers with a 580 credit score . Conventional loans offer 3% down for first-time buyers through specific programs .

6. How does mortgage insurance work on both loan types?

FHA loans require an upfront premium (1.75%) and annual MIP (0.15%-0.75%) . Conventional loans require PMI if you put down less than 20% . The key difference: FHA MIP often lasts the life of the loan, while conventional PMI can be canceled at 20% equity .

7. What are the 2026 loan limits for FHA and conventional loans?

For 2026, the FHA floor limit is $541,287 . The conventional conforming limit is $832,750 . Both have higher limits in high-cost areas.

best debt consolidation loans for good credit 2024

8. Can I use an FHA loan for an investment property?

No. FHA loans are strictly for primary residences . Conventional loans can be used for investment properties .

9. What credit score do I need for an FHA loan in 2026?

You need a 580 for the 3.5% down option. You can qualify with a score as low as 500 if you put 10% down . However, individual lenders may have higher requirements (overlays) .

10. How will the new 2026 credit score rules affect my mortgage application?

The new rules (FICO 10T and VantageScore 4.0) could help you qualify if you have a thin credit file, as they consider rent and utility payments . However, having a good traditional credit score remains the best way to secure a low interest rate .

Conclusion: Making Your Decision

Choosing between an FHA and a conventional loan comes down to your personal financial snapshot. There is no one-size-fits-all answer to the FHA loan vs conventional loan requirements question—only the answer that fits your credit score, your savings, and your long-term goals.

If you are just starting out, have had some credit challenges, or have limited savings, the FHA loan offers a forgiving path to homeownership. It is designed for you. If you have maintained good credit, saved a decent down payment, and are focused on minimizing your total interest costs over the life of the loan, the conventional loan is likely your best bet.

The most important step you can take is to speak with multiple lenders. Get quotes for both loan types. Compare the Loan Estimates side-by-side. Ask them to explain the costs and the conditions for removing mortgage insurance. With the information in this guide and professional advice tailored to your numbers, you can confidently choose the mortgage that will help you achieve and sustain the dream of homeownership.