By: Peiman Daneshgar | Email: daneshgar781@gmail.com**

Published: February 22, 2026**

Table of Contents

- What Does Renters Insurance Actually Cover? (The Stuff You Own vs. The Stuff You’d Never Think Of)

- Introduction: The “It Won’t Happen to Me” Lie

- What This Article Will Actually Give You

- Part 1: The Big Misconception (Your Landlord’s Insurance Doesn’t Cover You)

- Part 2: The Four Pillars of Renters Insurance

- Part 3: The “Wait, That’s Covered?” Surprises

- Part 4: The Fine Print—What’s NOT Covered

- Floods and Earthquakes (Nature’s Biggest Middle Finger)

- Pests (Sorry, Bed Bugs Are on You)

- Your Roommate’s Stuff (The Awkward Conversation)

- Your Car (That’s What Auto Insurance Is For)

- Intentional Damage (Obviously)

- Wear and Tear (You Can’t Blame the Insurance Company)

- High-Value Items (The Engagement Ring Problem)

- Part 5: Actual Cash Value vs. Replacement Cost (The $400 TV Math)

- Part 6: How Much Coverage Do You Actually Need?

- Part 7: How Much Does It Cost? (Spoiler: It’s Cheap)

- Part 8: International Notes (UK and Canada)

- Frequently Asked Questions

- The Emotional Bottom Line

Introduction: The “It Won’t Happen to Me” Lie

I know that feeling.

You just moved into a new apartment. Maybe it’s your first place without roommates. Maybe it’s a studio that’s slightly too small but has good light. You’re standing in the middle of it, looking at everything you own—the couch your mom helped you pick, the TV you saved up for, the coffee table you assembled while fighting with an Allen wrench.

It’s yours. All of it.

Then your landlord slides a piece of paper across the table during the lease signing. “You need renters insurance,” they say. “It’s required.”

You nod, take the paper, and immediately forget about it. Because renters insurance is for people who worry about bad things happening. And bad things don’t happen to you.

Sound familiar?

You’re not alone. Nearly two-thirds of the 81 million people who rent their homes don’t have renters insurance . They think their landlord’s insurance covers them. They think they don’t have enough stuff to matter. They think nothing bad will ever happen.

Then something bad happens.

A fire. A burglary. A guest slips on your wet floor and decides to sue. And suddenly, you’re staring at a $30,000 loss and realizing that “it won’t happen to me” was never a plan.

what to do if you can’t pay your taxes on time

🧠 Quick Reality Check:

Your landlord’s insurance covers the building—the walls, the roof, the appliances they own. Your stuff? Your clothes, your electronics, your furniture, your life? That’s on you . And if someone gets hurt in your apartment and sues, that’s on you too.

What This Article Will Actually Give You

Here’s the deal. Most insurance articles are either sales pitches or so full of jargon you need a translator.

This one is different.

By the time you finish reading, you’ll know:

- The four main things renters insurance covers—and why each one matters .

- The surprising stuff that’s covered (your bike at a coffee shop, your food in the freezer, your stuff in storage) .

- The things it doesn’t cover (floods, earthquakes, your roommate’s stuff) .

- Actual cash value vs. replacement cost—the $300 difference you need to understand .

- How much coverage you need and how much it costs (spoiler: it’s cheap) .

This is the playbook. Let’s run it.

can I deduct home office expenses in 2024?

Part 1: The Big Misconception (Your Landlord’s Insurance Doesn’t Cover You)

The Four Walls Myth

Let’s clear this up immediately: Your landlord’s insurance covers the building, not your stuff.

If a fire destroys your apartment, your landlord’s insurance will pay to rebuild the structure. It will not replace your couch, your TV, your clothes, or your books. That’s your problem .

The same goes for liability. If someone gets hurt in your apartment and sues, your landlord’s insurance covers the landlord—not you. You’re on your own .

What’s Actually at Stake

Add up what you own. Seriously. Walk through your apartment in your head:

- Laptop: $1,000

- Phone: $800

- TV: $500

- Bed and mattress: $1,000

- Dresser and clothes: $2,000

- Couch and coffee table: $800

- Kitchen stuff: $500

- Books, games, random stuff: $500

That’s $7,100. And that’s a modest estimate. If you have nicer stuff or more of it, you could easily be at $20,000+ .

Now imagine having to replace all of it tomorrow. Out of pocket. That’s what’s at stake.

tax deductions for freelancers and gig workers

🤔 Pause and Think:

If you had to buy everything in your apartment again tomorrow, how much would it cost? That number is why renters insurance exists.

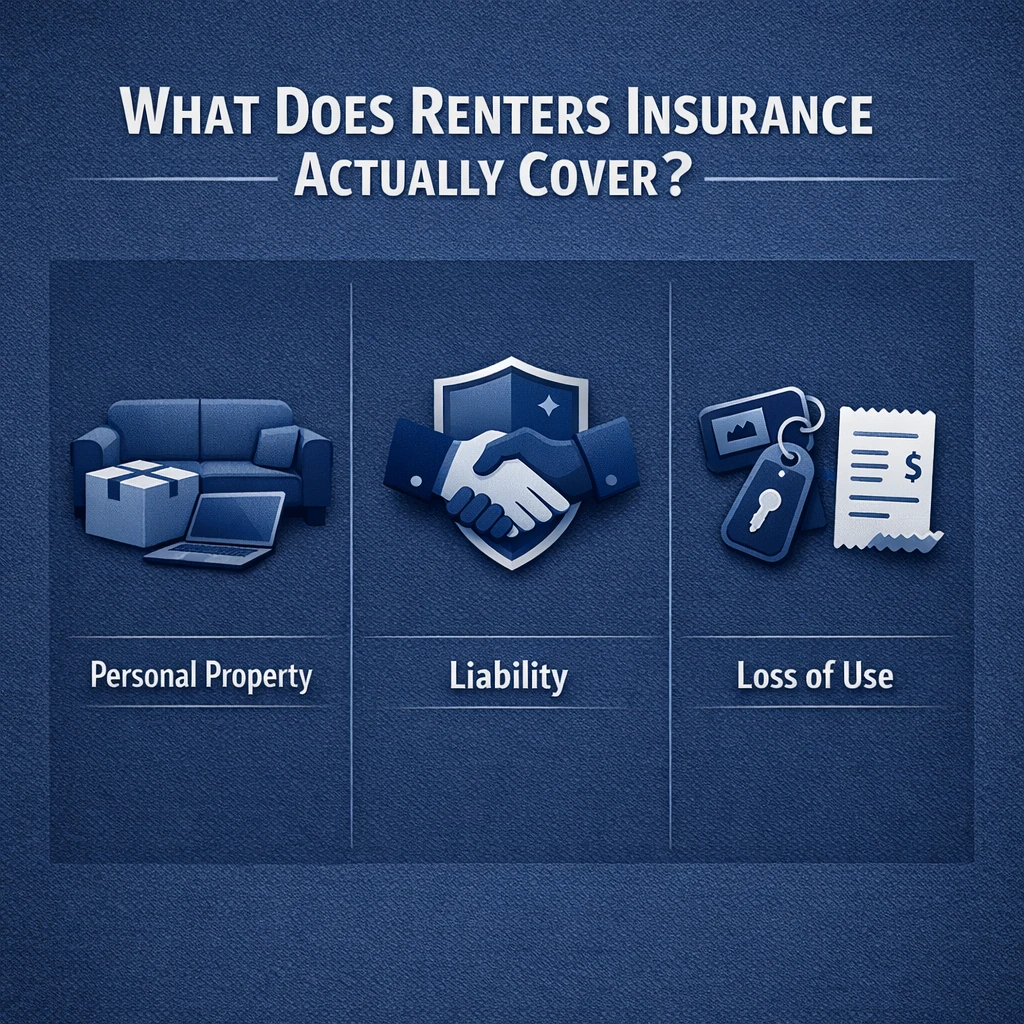

Part 2: The Four Pillars of Renters Insurance

Standard renters insurance policies cover four main areas .

Pillar 1: Personal Property—Your Stuff, Wherever It Is

This is the core of renters insurance. It covers your belongings if they’re damaged, destroyed, or stolen by a covered peril . Covered perils typically include:

- Theft

- Fire and smoke

- Lightning

- Vandalism

- Explosions

- Windstorms

- Water damage from plumbing issues (not floods)

- Electrical surges

Here’s the key: It doesn’t just cover stuff inside your apartment. If your bike is stolen while locked up at a coffee shop, it’s covered . If your luggage is stolen at the airport, it’s covered . Your stuff is covered anywhere in the world, up to your policy limits.

Pillar 2: Personal Liability—The “You Got Sued” Protection

This is the one people forget about until it’s too late.

If someone is injured in your apartment and sues you, personal liability coverage pays for:

- Their medical bills

- Your legal defense costs

- Court judgments against you (up to your policy limit)

Typical policies offer $100,000 in liability coverage . Some landlords require this much in their leases .

It also covers damage you cause to others. If your apartment floods because you left the bathtub running and it damages the unit below you, your liability coverage pays for the repairs .

authorized user vs co-signer: which helps credit more?

Pillar 3: Additional Living Expenses—The Hotel and Pizza Fund

If your apartment is damaged by a covered event (like a fire) and you can’t live there while it’s being repaired, Additional Living Expenses (ALE) coverage kicks in .

It pays for:

- Hotel stays

- Restaurant meals (since you can’t cook)

- Other extra costs above your normal living expenses

This turns a catastrophe into a temporary inconvenience. Without it, you’d be paying for a hotel out of pocket while still paying rent.

Pillar 4: Medical Payments to Others—No-Fault Band-Aids

This covers minor medical expenses for guests injured in your home, regardless of who’s at fault .

If a friend trips on your rug and twists an ankle, medical payments coverage pays their urgent care bill without them having to sue you. It’s usually up to $1,000–$5,000 per person.

Important: It doesn’t cover you or your family members. Just guests.

how to get a free FICO score from your bank

Part 3: The “Wait, That’s Covered?” Surprises

Beyond the four main pillars, renters insurance covers some things you might not expect .

Stolen Bike (Even at the Coffee Shop)

Your personal property coverage follows you. If your bike is stolen while you’re at a café, your renters insurance covers it . If your laptop is stolen from your car, covered .

Spoiled Food (The Freezer Disaster)

If a power outage ruins all the food in your freezer, your renters insurance will typically pay for it . Some policies have a sub-limit (like $500), but it’s better than nothing.

Your Stuff in Storage

If you have a storage unit, your belongings there are usually covered, but often at a lower limit—typically around 10% of your personal property coverage . If you have $20,000 in coverage, that’s $2,000 for storage.

Credit Card Fraud

If your wallet is stolen and someone uses your credit cards, your renters insurance might help recoup those losses . Check your policy.

Water Damage (But Only the Right Kind)

If a pipe bursts or your toilet overflows and ruins your stuff, that’s covered . If a river floods your apartment, that’s not. More on that below.

Your Dog Bites Someone (Maybe)

Liability coverage typically includes dog bites, but certain breeds may be excluded . Pit bulls, Rottweilers, and other breeds deemed “aggressive” might not be covered. Check with your insurer.

impact of credit card applications on your score

📋 Quick Checklist: Surprising Coverages

Item/Situation Covered? Bike stolen at coffee shop ✅ Yes Food in freezer after power outage ✅ Yes (up to limit) Stuff in storage unit ✅ Yes (usually 10%) Credit card fraud ✅ Yes (sometimes) Burst pipe damage ✅ Yes Flood from river ❌ No Dog bite (most breeds) ✅ Yes Dog bite (restricted breeds) ❌ Maybe not

Part 4: The Fine Print—What’s NOT Covered

Renters insurance is great, but it’s not everything. Here’s what it won’t cover .

Floods and Earthquakes (Nature’s Biggest Middle Finger)

Standard renters insurance does not cover flood, earthquake, or sinkhole damage . If you live in an area prone to these, you need separate policies or endorsements.

The National Flood Insurance Program offers flood insurance. Earthquake insurance is available in quake-prone states. It’s extra, but worth it if you’re at risk.

Pests (Sorry, Bed Bugs Are on You)

Renters insurance won’t cover damage from rodents, bed bugs, or other infestations . That’s considered a maintenance issue, and it’s your landlord’s responsibility to fix, but your stuff is still on you.

Your Roommate’s Stuff (The Awkward Conversation)

Your policy covers your belongings. Not your roommate’s . If you share a policy, the coverage limit is shared, which may not be enough for two people’s stuff. Most experts recommend separate policies for each roommate .

Your Car (That’s What Auto Insurance Is For)

Damage to your vehicle isn’t covered . That’s what auto insurance is for. However, items stolen from your car (like a laptop or backpack) are covered under personal property.

Intentional Damage (Obviously)

If you intentionally damage your own stuff or someone else’s, renters insurance won’t help . It’s for accidents and unforeseen events, not “I got mad and punched a hole in the wall.”

Wear and Tear (You Can’t Blame the Insurance Company)

Your old laptop that finally dies? Not covered. Insurance is for sudden, accidental damage, not things wearing out over time .

High-Value Items (The Engagement Ring Problem)

Standard policies have sub-limits on certain categories of items :

- Jewelry: Often $1,000–$2,000 total

- Electronics: Sometimes capped

- Art and collectibles: Limited

If you have an engagement ring worth $5,000, your standard policy might only cover $1,500. You’ll need a scheduled personal property endorsement (also called a “rider”) to cover the full value .

how to dispute an error on your credit report

Part 5: Actual Cash Value vs. Replacement Cost (The $400 TV Math)

When you buy renters insurance, you have to choose how your belongings will be valued if they’re destroyed or stolen . This choice matters a lot.

Actual Cash Value (The Depreciation Hammer)

Actual Cash Value (ACV) means the insurance company pays you what your items were worth at the time of loss, factoring in depreciation .

Example: You bought a TV for $400 five years ago. Today, it’s worth maybe $100. If it’s stolen, ACV coverage pays you $100. Good luck buying a new TV for that.

Replacement Cost (The “Get a New One” Option)

Replacement Cost Value (RCV) means the insurance company pays what it would cost to buy a new version of the item today .

Same TV: You get $400 (or whatever a comparable new TV costs). You can actually replace it.

what is a good credit score to buy a car?

The Verdict

Replacement cost coverage costs a little more in premiums, but it’s absolutely worth it . The difference between getting $100 and $400 for a stolen TV is the difference between being made whole and being screwed.

| Valuation Method | You Get | Can You Replace It? |

|---|---|---|

| Actual Cash Value | Depreciated value | Probably not |

| Replacement Cost | Cost of new item | Yes |

Part 6: How Much Coverage Do You Actually Need?

Step 1: Inventory Your Stuff

Walk through your apartment and add up what everything would cost to replace . Be honest. Use a spreadsheet or an app. Include:

- Furniture

- Electronics

- Clothing

- Kitchen items

- Books and media

- Sports equipment

- Jewelry

- Tools

- Anything else of value

This number is your personal property coverage need.

Step 2: Pick Your Liability Limit

$100,000 is standard and recommended . Many landlords require it . If you have significant assets (like a 401k or savings), consider higher limits or an umbrella policy for extra protection.

Step 3: Consider Endorsements

- Scheduled personal property for expensive jewelry, art, or collectibles

- Sewer backup coverage if you’re in a basement or older building

- Identity theft coverage

- Flood or earthquake insurance if applicable

The Quick Rule of Thumb

Most renters need $20,000–$50,000 in personal property coverage and $100,000 in liability. But the only way to know is to inventory your stuff.

does checking your credit score lower it?

Part 7: How Much Does It Cost? (Spoiler: It’s Cheap)

The National Association of Insurance Commissioners puts the average cost of renters insurance at $14 per month .

In the UK, NatWest reports 50% of new customers paid £9.92 or less per month .

In Canada, premiums range from $15 to $50 per month depending on coverage and location .

Factors that affect your rate:

- Where you live

- How much coverage you buy

- Your deductible (higher deductible = lower premium)

- Discounts (bundling with auto insurance, paying annually vs. monthly)

For less than the cost of two fancy coffees a month, you can protect tens of thousands of dollars in stuff and shield yourself from lawsuits. It’s one of the best deals in personal finance .

Part 8: International Notes (UK and Canada)

United Kingdom: Contents Insurance

In the UK, what Americans call “renters insurance” is usually called contents insurance . It covers your belongings inside your rented home.

- NatWest offers policies from £9.92/month covering £5,000–£25,000 of contents .

- Policies typically include “new for old” replacement (like replacement cost coverage).

- Check if you’re already covered under your parents’ home insurance if you’re a student .

Canada: Tenant Insurance Basics

In Canada, tenant insurance is similar to US renters insurance :

- Covers personal belongings, liability, and additional living expenses

- Average cost $15–$50/month

- Optional coverages: sewer backup, identity theft, overland water

- Not legally required but often required by landlords

- Bundling with auto insurance can save money

- best secured credit cards to build credit 2024

Frequently Asked Questions

Q: What does renters insurance cover?

A: Four main things: personal property (your stuff), personal liability (if you get sued), additional living expenses (hotel if you can’t live there), and medical payments to others (guest injuries) .

Q: Does renters insurance cover theft outside my apartment?

A: Yes. If your bike is stolen from a coffee shop or your laptop from your car, it’s covered .

Q: Does renters insurance cover my roommate’s stuff?

A: No. Your policy covers only your belongings. Roommates need their own policies .

Q: Does renters insurance cover water damage?

A: It depends. Burst pipes and overflow from appliances are covered. Floods from natural disasters are not .

Q: Does renters insurance cover dog bites?

A: Usually yes, but some breeds may be excluded . Check with your insurer.

Q: What’s the difference between actual cash value and replacement cost?

A: Actual cash value pays depreciated value (your 5-year-old TV for $100). Replacement cost pays what it costs to buy a new one ($400) .

Q: How much renters insurance do I need?

A: Enough to replace all your stuff. Do an inventory. Most people need $20,000–$50,000 in personal property coverage .

Q: How much does renters insurance cost?

A: Average is about $14/month in the US , £10/month in the UK , and $15–$50/month in Canada .

Q: Is renters insurance required?

A: Not by law, but many landlords require it in the lease . Even if not required, it’s a smart purchase.

Q: Does renters insurance cover my engagement ring?

A: Standard policies have low limits for jewelry (often $1,000–$1,500). You need a separate endorsement to cover expensive items .

Q: What’s not covered by renters insurance?

A: Floods, earthquakes, pests, your roommate’s stuff, your car, intentional damage, and wear and tear .

The Emotional Bottom Line

Look, I’m not going to pretend that renters insurance is exciting.

It’s not. It’s boring paperwork that costs a few bucks a month and sits in a drawer doing nothing. It’s the definition of an expense you hope you never need to use.

But here’s the thing: Insurance isn’t for the things that happen every day. It’s for the one thing that happens once.

The fire. The burglary. The guest who falls and decides to sue. These things don’t happen often. But when they do, they can wipe out years of savings in an instant.

Renters insurance is cheap—literally the cost of a pizza or two a month. For that tiny price, you get peace of mind that your stuff is protected anywhere in the world, that you won’t be bankrupted by a lawsuit, and that if your apartment becomes uninhabitable, you’ve got a place to stay.

Sixty percent of renters don’t have it . Don’t be one of them.

Get the policy. Inventory your stuff. Sleep better.

You’ve got this.