By: Peiman Daneshgar | Email: daneshgar781@gmail.com**

Published: February 21, 2026**

Table of Contents

- How to File Taxes as a Married Couple for the First Time (Without Killing Each Other)

- Introduction: The First Big Fight

- What This Article Will Actually Give You

- Part 1: The Most Important Thing Nobody Tells Newlyweds

- Part 2: The Big Question—Joint or Separate?

- Part 3: The Side-by-Side Comparison (Joint vs. Separate)

- Part 4: What Changes When You File Jointly (The Good Stuff)

- Part 5: What You Need to File (The Document Checklist)

- Part 6: The W-4 Nightmare (Fix This Now or Pay Later)

- Part 7: The New Tax Breaks for 2025-2026 (Don’t Miss These)

- Part 8: Step-by-Step—How to Actually File

- Frequently Asked Questions

- The Emotional Bottom Line

Introduction: The First Big Fight

I know that feeling.

You’ve been married for… what, six months? A year? The wedding photos are still on your phone. You’re still figuring out whose turn it is to do the dishes. And now April is creeping up, and you have to do something you’ve never done before:

File taxes. Together.

Suddenly you’re sitting at the kitchen table with a pile of papers that looks like a confetti factory exploded. W-2s. 1099s. Mortgage statements. Student loan papers. Receipts for… is that your honeymoon? Can you deduct that? (Spoiler: no.)

mortgage pre-approval process step-by-step

And then comes the question that starts the first real argument of your marriage:

“Should we file jointly or separately?”

You’ve both been doing your own taxes for years. You know your stuff. But now there’s another person involved, with their own income, their own deductions, their own… everything. And every website you check gives you a different answer.

Your coworker says joint is always better. Your brother-in-law says separate saved him thousands. Your mom says she and dad have always filed jointly and you should too. Who’s right?

Sound familiar?

You’re not alone. Every year, millions of newly married couples stare at their tax returns and wonder if they’re doing it wrong. The tax code doesn’t come with a marriage manual. And the IRS? They’re not exactly sending you a congratulations card with instructions.

🧠 Quick Reality Check:

The good news? Filing taxes as a married couple isn’t actually harder than filing single. It’s just different. And once you understand a few key rules, you’ll be fine. Maybe even better than fine—because marriage comes with some pretty sweet tax breaks.

What This Article Will Actually Give You

Here’s the deal. Most tax articles are written by CPAs for other CPAs. They’re full of jargon and footnotes that make your eyes glaze over.

This one is different.

By the time you finish reading, you’ll know:

- The single most important thing you need to do right now (before you even think about filing) .

- Whether you should file jointly or separately—with real reasons for each choice .

- The exact documents you need to gather from both of you .

- How to fix your W-4 withholding so you don’t get a nasty surprise next year .

- The new tax breaks for 2025-2026 that could save you thousands .

- A step-by-step plan to get this done without fighting .

This is the playbook. Let’s run it.

FHA loan vs Conventional loan requirements

Part 1: The Most Important Thing Nobody Tells Newlyweds

Before you even think about deductions or credits or filing status, there’s something you need to do. And if you skip it, your refund could be delayed for months.

The December 31 Rule

Here’s the first thing to know: Your marital status on December 31 determines your filing status for the entire year .

Got married on January 5th? You file as single for the previous year. Got married on December 30th? Congratulations—you’re filing jointly (or separately) for the whole year, even though you were single for 364 days .

This catches a lot of people off guard. If you got married in 2025, even on December 31st, you’re filing as a married couple for the 2025 tax year .

The Name Change Trap

If you changed your name after getting married, you need to tell the Social Security Administration. Now.

Not the IRS. The SSA .

Here’s why: The IRS matches the name on your tax return with what’s in the SSA’s database. If they don’t match, your refund gets held up. Sometimes for months .

The fix: File Form SS-5 (Application for a Social Security Card) with your new name. You can do it online at SSA.gov, by phone, or at a local SSA office . Do this before you file your taxes.

The Address Update

If you moved in together (or to a new place), update your address with:

- The post office

- Your employers

- The IRS (Form 8822, Change of Address)

- how much house can I afford on a $70,000 salary?

This ensures all your tax documents—W-2s, 1099s, IRS notices—actually reach you.

🤔 Pause and Think:

If you changed your name and haven’t updated it with the SSA yet, stop reading and do that now. Seriously. It takes 10 minutes online and could save you months of waiting for your refun

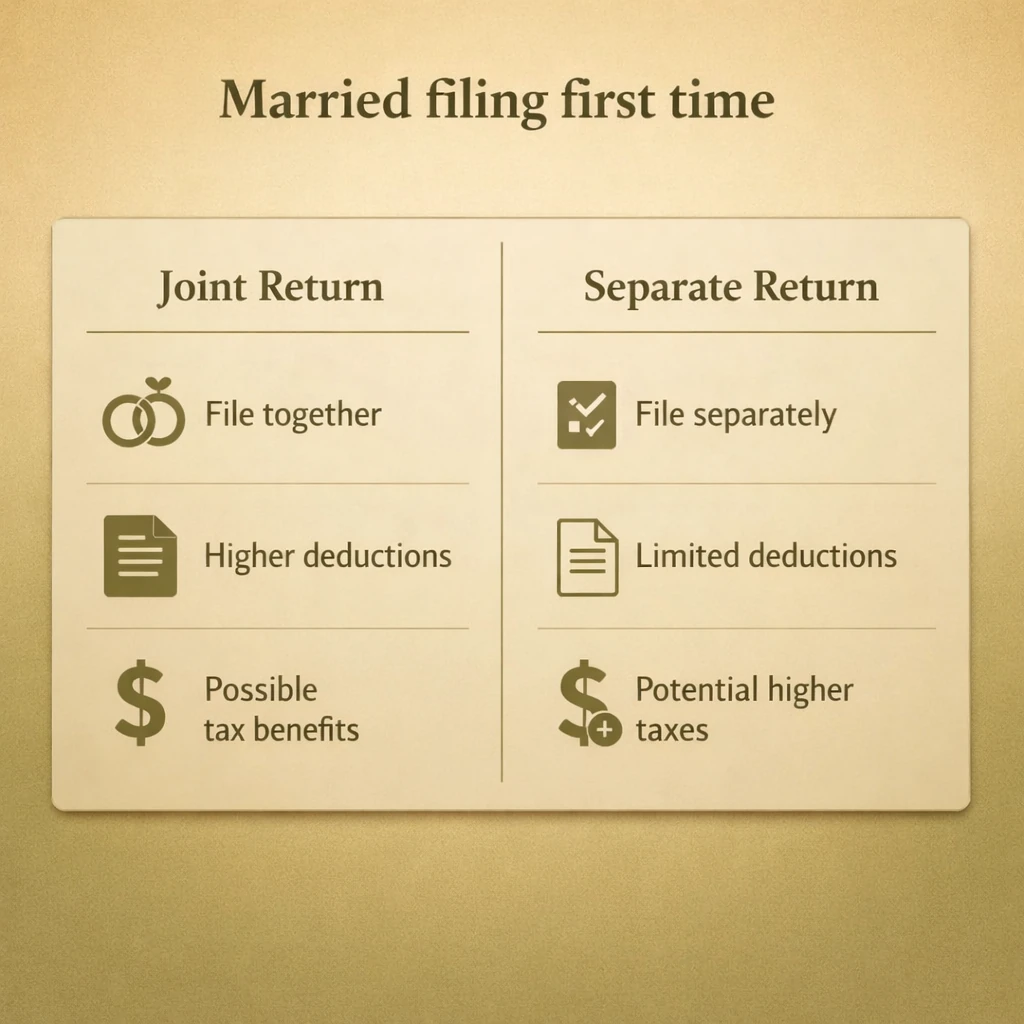

Part 2: The Big Question—Joint or Separate?

This is the question every married couple faces. And the answer is almost always the same.

The Simple Answer (For Most Couples)

For the vast majority of married couples, filing jointly is the better choice .

Why? Because joint filers get:

- A much higher standard deduction

- Access to valuable tax credits

- Generally lower tax rates

- Higher income limits for deductions and credits

The TaxAct blog puts it bluntly: “Married filing jointly generally offers more tax advantages for married couples, while filing separately often limits deductions and credits” .

The “Marriage Penalty” Myth (And When It’s Actually Real)

You may have heard about the “marriage penalty”—the idea that getting married makes you pay more taxes. Is it real?

Sometimes.

When both spouses earn similar high incomes, filing jointly can push you into a higher tax bracket than you’d be in as two single filers . The TaxSlayer article notes that “combining incomes can sometimes push couples into a higher tax bracket, resulting in a larger overall tax bill compared to filing separately” .

But for most couples—especially those with one higher earner and one lower earner—the marriage bonus outweighs any penalty.

first-time home buyer grants and programs 2024

When Filing Separately Actually Makes Sense

There are specific situations where filing separately is worth considering :

1. Income-driven student loan repayment. If one spouse has student loans and is on an income-driven repayment plan, filing separately can keep payments lower because only that spouse’s income counts .

2. High medical expenses. Medical expenses are only deductible if they exceed 7.5% of your adjusted gross income . If one spouse has huge medical bills and the other has a high income, filing separately might allow that spouse to clear the threshold and deduct more .

3. Protecting one spouse from the other’s tax issues. If one spouse owes back taxes, has garnishments, or is being audited, filing separately can shield the other spouse from liability .

4. Significant miscellaneous itemized deductions. If one spouse has deductions that are limited by AGI, a lower separate AGI might make them usable .

5. Legal separation or divorce planning. Couples who are separated but not yet divorced might prefer to keep finances separate .

The Community Property State Complication

If you live in a community property state (like California, Texas, or Arizona), filing separately gets complicated .

In these states, income is generally split 50/50 between spouses, even if only one person earned it . That can reduce or eliminate the benefits of filing separately, because your separate return still includes half your spouse’s income.

is debt consolidation a good idea?

The Only Way to Know for Sure

Here’s the truth: You can’t know which is better until you calculate both ways .

The IRS itself says: “While filing jointly is usually more beneficial, it’s best to figure the tax both ways to find out which makes the most sense” .

Good tax software will do this automatically. It’ll calculate your taxes both ways and show you which one saves you more money . If you’re using a tax pro, they’ll do the same thing.

📊 Quick Rule of Thumb

Situation Likely Best Choice Similar incomes, both under $200k Joint One high earner, one low earner Joint Both high earners ($300k+) Calculate both Income-driven student loans Possibly Separate Huge medical bills for one spouse Possibly Separate One spouse has major tax problems Separate

Part 3: The Side-by-Side Comparison (Joint vs. Separate)

Let’s put them next to each other so you can see exactly how they differ .

| Factor | Married Filing Jointly | Married Filing Separately |

|---|---|---|

| Standard Deduction (2025) | $31,500 | $15,750 each |

| Tax Brackets | Wider brackets, lower rates | Narrow brackets, higher rates |

| Child Tax Credit | Available | Usually not available |

| Earned Income Tax Credit | Available | Not available |

| Education Credits | Available | Not available |

| Student Loan Interest Deduction | Available (up to $2,500) | Not available |

| Roth IRA Contributions | Higher income limits | Lower income limits |

| Medical Expense Deduction | 7.5% of combined AGI | 7.5% of individual AGI |

| Liability | Both responsible for full tax | Each responsible for own |

| Filing Complexity | One return | Two returns |

Part 4: What Changes When You File Jointly (The Good Stuff)

If you decide to file jointly (and you probably will), here’s what you get.

The Standard Deduction Just Doubled (Almost)

For 2025 taxes (filed in 2026), the standard deduction for married couples filing jointly is $31,500 .

Compare that to:

- Single filers: $15,750

- Married filing separately: $15,750 each

That’s almost double the single deduction. You’re basically getting two deductions in one .

For 2026 taxes (filed in 2027), it goes up to $32,200 .

how to talk to creditors when you can’t pay

Tax Brackets Get Bigger

Tax brackets for joint filers are exactly twice as wide as for single filers, up to a point .

For 2026:

- The 12% bracket goes up to $24,800 for joint filers (vs. $12,400 for single)

- The 22% bracket goes up to $100,800 for joint filers (vs. $50,400 for single)

- The 24% bracket goes up to $211,400 for joint filers (vs. $105,700 for single)

This means more of your income is taxed at lower rates.

Credits You Couldn’t Get Before

Many valuable tax credits are simply not available to married couples filing separately :

- Earned Income Tax Credit (EITC)

- Child Tax Credit (in most cases)

- Child and Dependent Care Credit

- Adoption Credit

- American Opportunity Credit

- Lifetime Learning Credit

- Saver’s Credit

If you qualify for any of these, filing jointly is almost certainly better.

government programs for medical debt relief

The Home Sale Loophole

When you sell your primary residence, married couples filing jointly can exclude up to $500,000 of capital gains from taxes .

Single filers? Only $250,000.

If you’re planning to sell a home anytime soon, that’s a huge advantage.

Retirement Benefits

Filing jointly can also affect your retirement planning :

- Higher income limits for Roth IRA contributions

- Ability to deduct Traditional IRA contributions even if one spouse isn’t covered by a workplace plan

- Spousal IRAs for non-working spouses

Part 5: What You Need to File (The Document Checklist)

Before you start, gather everything. Having it all in one place makes the process infinitely easier .

Personal Identification

- Social Security numbers for both spouses

- Photo IDs (driver’s licenses or state IDs)

- Dates of birth for both

Income Documents (Both of You)

- W-2s from all employers

- 1099s for freelance work, contract gigs, or side hustles

- 1099-INT, 1099-DIV for interest and dividends

- 1099-G for unemployment benefits

- 1099-R for retirement distributions

- K-1s if you’re in a partnership or S-corp

- Records of self-employment income and expenses

Deduction Documents

- Mortgage interest statement (Form 1098)

- Property tax records

- State and local income taxes paid (or sales tax records)

- Charitable donation receipts

- Medical expense receipts (if you plan to itemize)

- Student loan interest statements (Form 1098-E)

- IRA contribution records

- Educator expense records (up to $300 for teachers)

Credit Documents

- Child care expense records (provider name, address, tax ID)

- Education expense statements (Form 1098-T)

- Adoption expense records

- Energy-efficient home improvement receipts

- how to use a balance transfer card wisely

💡 Pro Tip:

Create a shared folder—physical or digital—and both of you throw everything in there as it arrives. Much easier than hunting for papers on April 14th.

Part 6: The W-4 Nightmare (Fix This Now or Pay Later)

Here’s something nobody tells newlyweds, but it’s critically important:

After you get married, you need to update your W-4 forms with your employers .

The Two-Income Problem

When you were both single, your employers withheld taxes based on single rates. Now that you’re married, those withholding amounts are probably wrong .

If you both work and don’t adjust your withholding, you might end up underwithholding—meaning you’ll owe money at tax time. Possibly a lot.

Why? Because the single tax tables assume your income is the only income in your household. When you combine two incomes, you can get pushed into higher brackets that your individual withholdings didn’t account for .

How to Fix It

Within 10 days of getting married, you should give each employer a new Form W-4, Employee’s Withholding Certificate .

The IRS has a Tax Withholding Estimator on their website that can help you figure out the right settings .

The key section for married couples is Step 2, where you indicate that your spouse also works. This helps your employer withhold the right amount .

🤔 Pause and Think:

If you got married in 2025 and haven’t updated your W-4s yet, you might be in for a nasty surprise come April. Do this now—it takes 10 minutes per person.

Part 7: The New Tax Breaks for 2025-2026 (Don’t Miss These)

The One Big Beautiful Bill Act, signed into law July 4, 2025, created several new tax breaks you need to know about .

New Senior Deduction

For tax years 2025-2028, taxpayers age 65 and older can claim an additional deduction of up to $6,000 per person (or $12,000 for a married couple if both qualify) .

This phases out for incomes above $75,000 ($150,000 for joint filers) and is completely phased out at $175,000 ($250,000 for joint filers) .

If you or your spouse turned 65 in 2025, this could save you real money.

Tip Deduction

For 2025-2028, workers in tipped occupations can deduct up to $25,000 of tips from their taxable income .

This applies to a wide range of occupations, including restaurant workers, hairdressers, rideshare drivers, and even digital content creators who receive tips or donations .

The deduction phases out for incomes above $150,000 ($300,000 for joint filers) .

Strategies to Pay Off $30,000 in Student Loans

Overtime Deduction

For 2025-2028, hourly workers can deduct the “premium” portion of overtime pay—basically, the extra half of time-and-a-half—up to $12,500 ($25,000 for joint filers) .

Auto Loan Interest Deduction

For 2025-2028, you can deduct interest on auto loans for vehicles assembled in the United States, up to $10,000 per year .

The vehicle must be for personal use (not business) and have final assembly in the U.S. .

Part 8: Step-by-Step—How to Actually File

Okay, you’ve gathered your documents, chosen your filing status, and checked your withholding. Now let’s actually file.

Step 1: Gather Everything

Use the checklist in Part 5. Make sure you have everything from both of you .

Step 2: Choose Your Method

You have two main options :

Tax Software:

- Good for most couples

- Step-by-step guidance

- Automatically calculates both filing statuses to find the better option

- Cheaper than a pro (often free for simple returns)

Tax Professional:

- Good for complex situations (businesses, rentals, investments)

- Provides peace of mind

- Can offer personalized advice

- Costs $100-$300+ depending on complexity

- does debt settlement hurt your credit score?

Step 3: Run the Numbers Both Ways

If you’re using software, it will do this automatically. If you’re working with a pro, ask them to calculate your taxes both jointly and separately so you can see which saves more .

Step 4: File (and Breathe)

The deadline for 2025 taxes is April 15, 2026 .

If you need more time, you can file for an extension (Form 4868), which pushes the filing deadline to October 15 . But remember: an extension to file is NOT an extension to pay. Your taxes are still due April 15 .

If you can’t pay in full, file anyway and set up a payment plan with the IRS .

Frequently Asked Questions

Q: Do we have to file jointly?

A: No. You can choose to file jointly or separately each year .

Q: Which is better—joint or separate?

A: For most couples, joint is better. But you should calculate both ways to be sure .

Q: What’s the standard deduction for married couples in 2025?

A: $31,500 for joint filers, $15,750 each for separate filers .

Q: Do I need to change my name with the IRS?

A: No. Change it with the Social Security Administration first. The IRS gets updates from them .

Q: When do I need to update my W-4?

A: Within 10 days of getting married, you should give your employer a new W-4 .

Q: What if we got married in December 2025?

A: Your marital status on December 31 determines your filing status for the entire year. You file as married for 2025 .

Q: Can we file jointly if we lived apart for part of the year?

A: Yes. As long as you’re legally married on December 31, you can file jointly regardless of where you lived .

Q: What’s the new senior deduction for 2025?

A: Up to $6,000 per eligible person ($12,000 for couples) if both are 65+ and income is under $75,000/$150,000 .

Q: Can I still deduct student loan interest if we file jointly?

A: Yes. Joint filers can deduct up to $2,500 of student loan interest, subject to income limits . Separate filers cannot deduct it at all .

Q: What documents do we need to file?

A: W-2s, 1099s, Social Security numbers, mortgage statements, donation receipts, and any other income/deduction records for both spouses .

Q: What if we can’t pay our taxes by April 15?

A: File anyway and set up a payment plan. The failure-to-file penalty is much higher than the failure-to-pay penalty .

Q: Do we have to file state taxes differently?

A: State rules vary. Some states require you to use the same filing status as your federal return. Check your state’s guidelines .

The Emotional Bottom Line

Look, I’m not going to pretend that filing taxes as a married couple is romantic.

It’s not. It’s paperwork. It’s math. It’s sitting at the kitchen table trying to remember if that receipt from the hardware store is deductible (it’s not).

But here’s the thing: This is your first joint financial act as a married couple. It’s practice for all the big decisions you’ll make together—buying a house, having kids, saving for retirement, maybe starting a business.

The couples who get through tax season without killing each other? They’re the ones who communicate, who share the load, who remember that it’s just taxes—not a judgment on their relationship.

So sit down together. Spread out the papers. Order pizza. Make it a thing.

And if you mess something up? That’s what amendments are for. You’ll figure it out together.

You’ve got this.