The Ultimate Guide to Sinking Funds: What They Are and How to Set Them Up for Financial Success

Executive Summary

Sinking funds are a powerful, proactive financial tool that transforms how you manage large, irregular expenses. Unlike emergency funds, which cover unexpected costs, sinking funds are strategic savings pots designed for anticipated, non-monthly expenses. This comprehensive guide will explore everything from the fundamental principles of sinking funds to advanced implementation strategies, ensuring you have a complete roadmap to financial predictability and peace of mind.

Chapter 1: Understanding Sinking Funds – The Foundation of Predictable Finances

1.1 What Exactly Is a Sinking Fund?

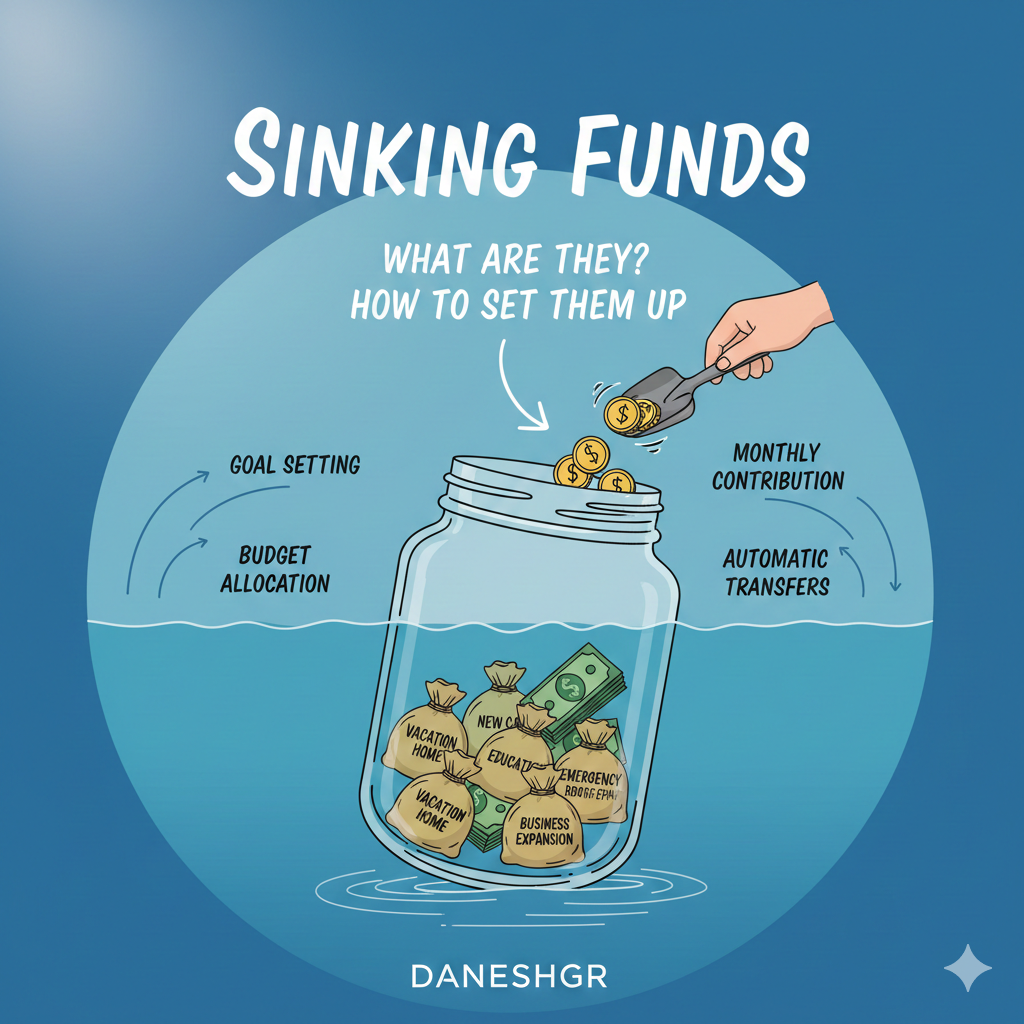

A sinking fund is a dedicated savings account or sub-account reserved for a specific future expense. The term originates from corporate finance, where companies set aside money regularly to repay debt or replace assets. In personal finance, it’s a disciplined method of breaking down large, foreseeable costs into manageable monthly savings increments. This proactive approach prevents financial shocks and avoids reliance on credit cards or loans when these expenses arise.

1.2 The Critical Difference: Sinking Fund vs. Emergency Fund

Many confuse sinking funds with emergency funds, but their purposes are distinct:

- Emergency Fund: For true, unexpected emergencies—job loss, major medical events, urgent car or home repairs. This is your financial safety net.

- Sinking Fund: For expected, irregular expenses—yearly insurance premiums, holiday gifts, car maintenance, property taxes, vacations. This is your financial planning tool.

A complete financial system includes both. The emergency fund handles the “uh-oh” moments, while sinking funds handle the “I knew this was coming” expenses.

how to create a budget for beginners step by step

1.3 The Psychology and Benefits of Using Sinking Funds

The benefits extend beyond mere practicality:

- Eliminates Financial Stress: Knowing money is set aside for annual bills creates immense psychological relief.

- Prevents Debt Accumulation: By saving in advance, you avoid high-interest debt for planned purchases.

- Promotes Intentional Spending: You spend with purpose, aligning your money with your priorities.

- Creates Financial Transparency: You see exactly what your future obligations are, enabling better budgeting.

- Builds Financial Discipline: Regular contributions cultivate a savings habit.

Chapter 2: Identifying Your Sinking Fund Categories – A Comprehensive Audit

2.1 Conducting a Financial Expense Audit

Start by reviewing 12-24 months of bank and credit card statements. Look for non-monthly expenditures. Common categories include:

Home-Related:

- Property taxes (if not escrowed)

- Homeowners or renters insurance (annual premium)

- Home maintenance (1-2% of home value annually)

- Appliance replacement fund

- HOA fees (if quarterly or annually)

- Major renovations

best budgeting method for irregular income

Automotive:

- Car insurance (if paid every 6 months)

- Vehicle registration and taxes

- Routine maintenance (oil changes, tire rotations)

- New tires or brakes

- Future down payment for next vehicle

Personal & Family:

- Holiday gifts and celebrations

- Birthday gifts and parties

- Vacation and travel

- Back-to-school expenses

- Subscriptions (annual memberships)

- Clothing (seasonal updates)

Medical & Wellness:

- Out-of-pocket medical expenses (deductibles, co-pays)

- Dental work (cleanings, procedures)

- Vision care (glasses, contacts)

- Fitness memberships or equipment

Other Obligations:

- Professional certifications or dues

- Continuing education

- Charitable giving (annual donations)

- Tax preparation fees (if not included in monthly budgeting)

2.2 Calculating Your Target Amounts

For each category, determine:

- Total Annual Cost: Estimate the yearly expense.

- Monthly Contribution: Divide the annual cost by 12.

Example: A $1,200 annual car insurance premium requires a $100 monthly sinking fund contribution.

For variable expenses (like home maintenance), use a percentage-based approach (e.g., 1% of home value saved annually) or a historical average.

Chapter 3: Setting Up Your Sinking Fund System – A Step-by-Step Guide

3.1 Choosing the Right Financial Vessel

Where you keep your sinking funds matters for accessibility, growth, and mental accounting:

50/30/20 rule calculator excel template free

High-Yield Savings Accounts (HYSAs):

- Best for: Most users. Offers separation from checking, easy transfers, and some interest.

- Recommendation: Use a single HYSA with sub-accounts or “buckets” (features offered by Ally Bank, Capital One, etc.).

Separate Savings Accounts:

- Best for: Those who prefer complete physical separation.

- Drawback: Can become cumbersome with multiple accounts.

Cash Envelopes:

- Best for: Cash-based budgeters or certain short-term goals (like holiday cash).

- Drawback: No interest, security risks.

Money Market Accounts:

- Best for: Larger sinking funds where you want slightly better interest with check-writing access.

Avoid: Investing sinking funds in stocks or volatile assets. The principle must be protected for its intended use.

3.2 The Setup Process

- List All Categories: From your audit, list every sinking fund you need.

- Assign Dollar Amounts: Calculate the monthly contribution for each.

- Choose Your Bank: Open or designate an account.

- Set Up Automatic Transfers: Schedule transfers from checking to sinking fund right after each payday. Automation is key to success.

- Track Balances: Use a spreadsheet, app, or your bank’s tracking tools to monitor each category’s balance.

- Spend Guilt-Free: When the expense occurs, transfer the money and pay it, knowing you planned perfectly.

3.3 Integration with Your Overall Budget

Sinking funds are a line item in your monthly budget. Treat contributions as non-negotiable expenses. Popular budgeting methods that incorporate sinking funds include:

- Zero-Based Budgeting: Assign every dollar, including sinking fund contributions, a job.

- The 50/30/20 Rule: Sinking funds typically fall into the “Needs” (50%) or “Savings/Debt” (20%) categories, depending on the expense.

- Envelope System: Digital or physical envelopes for each category.

how to save money on a tight income

Chapter 4: Advanced Strategies and Optimization

4.1 Tiered Sinking Funds

Create urgency-based tiers:

- Tier 1 (High Priority/Short-Term): Funds needed within 12 months (taxes, insurance). Keep in most accessible account.

- Tier 2 (Medium-Term): Funds for 1-3 years (new car fund, roof repair). Could consider a CD ladder for slightly better rates.

- Tier 3 (Long-Term): Funds for 5+ years (future vehicle replacement, large renovation). Could mix with conservative investments, but understand the risk.

4.2 The Sinking Fund “Float”

Once your system is mature, you’ll have a constant “float” of money across all categories. This collective balance can earn meaningful interest in a HYSA, effectively giving you a discount on your future expenses.

4.3 Handling Surpluses and Shortfalls

- Surplus: If you have money left in a category after an expense (e.g., a cheaper vacation), you can: roll it over to next year’s goal, redistribute to an underfunded category, or put it toward a financial goal.

- Shortfall: If you underestimate, avoid using the emergency fund. Instead, adjust future monthly contributions upward or temporarily reduce contributions to a lower-priority sinking fund to cover the gap.

4.4 Technology to Manage Your Sinking Funds

- Banking Apps with Buckets: Ally, Capital One, SoFi.

- Budgeting Apps: YNAB (You Need A Budget) is built on this philosophy. Also, Goodbudget, EveryDollar.

- Simple Spreadsheets: Offer complete customization.

Chapter 5: Common Pitfalls and How to Avoid Them

- Not Starting Small: Begin with 2-3 most pressing categories. Don’t try to fund 15 categories from day one.

- Commingling Funds: Never mix sinking funds with your checking or emergency fund. Separation ensures the money is preserved for its purpose.

- Forgetting to Replenish: After spending from a fund, immediately resume—or adjust—your monthly contributions for the next cycle.

- Underestimating Costs: Regularly review and adjust your target amounts for inflation and changing circumstances.

- Using It for Unintended Purposes: The “vacation fund” is not for a spontaneous shopping spree. Maintain discipline.

Chapter 6: Sinking Funds in Action – Case Studies

Case Study 1: The Young Professional

Challenge: Maria, 28, was consistently stressed by her $800 semi-annual car insurance payment and $1,500 annual vacation.

Solution: She created two sinking funds: $134/month for insurance and $125/month for vacation in an HYSA.

Outcome: She now pays both expenses seamlessly, earns interest on her savings, and has eliminated her reliance on credit cards for these costs.

Case Study 2: The Growing Family

Challenge: The Carter family was overwhelmed by irregular expenses: holidays, back-to-school, sports fees, and home maintenance.

Solution: They implemented a “Family Sinking Fund System” with 8 categories, contributing a total of $450 monthly.

Outcome: They experience no financial surprises, can participate in all family activities without stress, and are teaching their children valuable money management skills.

Frequently Asked Questions (FAQs)

Q1: How many sinking funds should I have?

A: There’s no magic number. Start with 3-5 for your most stressful expenses. Over time, you may have 10-15. The right number is what covers your predictable expenses without being too complex to manage.

Q2: Where is the best place to keep sinking funds?

A: A high-yield savings account with sub-account/bucket features is ideal for most people. It offers a good blend of yield, accessibility, and organizational tools.

Q3: What if I don’t have enough money to fund all categories?

A: Prioritize. Rank your sinking fund categories by necessity (e.g., property taxes before vacation fund). Fund the essentials first, and add more as your budget allows.

Q4: Can I use sinking funds for debt repayment?

A: Absolutely. A “Debt Payoff Sinking Fund” can be used to accumulate money for a lump-sum settlement offer or to pay off a smaller debt in full. However, for standard debt repayment, a consistent monthly payment plan is usually more effective.

Q5: How do sinking funds work with variable income?

A: Calculate your needed annual contributions. In high-income months, fund several months ahead. In low-income months, make minimum contributions to the highest priority funds. A larger-than-usual emergency fund is also crucial for variable income.

Q6: Should I earn interest on my sinking funds?

A: Yes, but safety and accessibility are paramount. Prioritize a high-yield savings account over riskier investments. The goal is capital preservation for planned spending, not aggressive growth.

Q7: What’s the difference between a sinking fund and a savings goal?

A: They are closely related. A sinking fund is typically for expenses (often recurring), while a savings goal is for a purchase or achievement (like a down payment). The mechanics of saving are identical.

Q8: How often should I review my sinking funds?

A: Conduct a quick review monthly when you budget. Do a thorough annual audit of all categories and contribution amounts to adjust for life changes and inflation.

money saving challenges for couples

Conclusion: Mastering Your Financial Future

Implementing a sinking fund system is one of the most transformative actions you can take for personal financial health. It moves you from a reactive, stressed financial stance to a proactive, confident one. By breaking down large, scary expenses into small, manageable monthly steps, you take the power back from your calendar and your bills.

Start today. Pick one expense—perhaps the next one you’re dreading—and calculate its monthly sinking fund contribution. Open that dedicated savings account and set up the first automatic transfer. This single step is the beginning of a journey toward true financial control and the profound peace of mind that comes with knowing you are prepared for what the future holds. Sinking funds are not just about saving money; they are about designing a predictable, intentional, and successful financial life.