By: Peiman Daneshgar | Email: daneshgar781@gmail.com**

Published: February 19, 2026**

Table of Contents

- How to Get a Free FICO Score from Your Bank (Without Paying a Dime or Getting Scammed)

- Introduction: The $29.95 Trap

- What This Article Will Actually Give You

- Part 1: The Short Answer—Yes, You Probably Already Have Access

- Part 2: Why FICO Matters More Than Those Other Scores

- Part 3: The FICO Score Open Access Program—Your Secret Weapon

- Part 4: Major Banks That Give You Free FICO Scores

- Part 5: Credit Unions That Offer Free FICO Scores

- Part 6: What If You Don’t Have an Account? (No Problem)

- Part 7: How to Find Your Free Score in Your Bank’s App

- Part 8: What to Do If Your Bank Doesn’t Offer It

- Part 9: Common Questions About Free Bank FICO Scores

- Part 10: What to Do With Your Free FICO Score

- Frequently Asked Questions

- The Emotional Bottom Line

Introduction: The $29.95 Trap

I know that feeling.

You’re lying in bed, scrolling through your phone, and you see an ad. “Get your credit score instantly!” “See what lenders see!” “Unlock your financial future!”

You click. You enter your email. You enter your name. You enter your credit card information “just to verify your identity.”

And then, thirty days later, you see a $29.95 charge on your statement. Then another one next month. And another. And suddenly that “free” credit score is costing you $360 a year.

You’ve been trapped in a subscription you never wanted.

Sound familiar?

Maybe you’ve been paying for credit monitoring because you thought that was the only way to see your FICO score. Maybe you’ve been using free sites that give you a score, but you’re not sure if it’s the real score—the one lenders actually use. Maybe you’ve just been avoiding checking altogether because you don’t want to get tricked into another monthly fee.

Here’s the truth that credit bureaus and marketing companies don’t want you to know: Your bank already gives you your FICO score for free. You just don’t know where to look.

🧠 Quick Reality Check:

If you have a checking account, a savings account, or a credit card with any major bank, you almost certainly have free access to your FICO score. You’ve had it for years. You just never knew it was there.

What This Article Will Actually Give You

Here’s the deal. Most articles will tell you “check with your bank” and leave you to figure it out.

This one is different.

By the time you finish reading, you’ll know:

- Exactly which banks and credit unions offer free FICO scores (with a massive list you can check right now) .

- Why FICO matters more than the scores you get from Credit Karma or other free sites .

- How to find your score in your bank’s app or website in under 60 seconds .

- What to do if your bank doesn’t offer it (including free options that work for anyone) .

- The difference between FICO and VantageScore—and why it matters when you apply for credit .

This is the treasure map. Let’s go find your score.

costs of buying a home besides the down payment

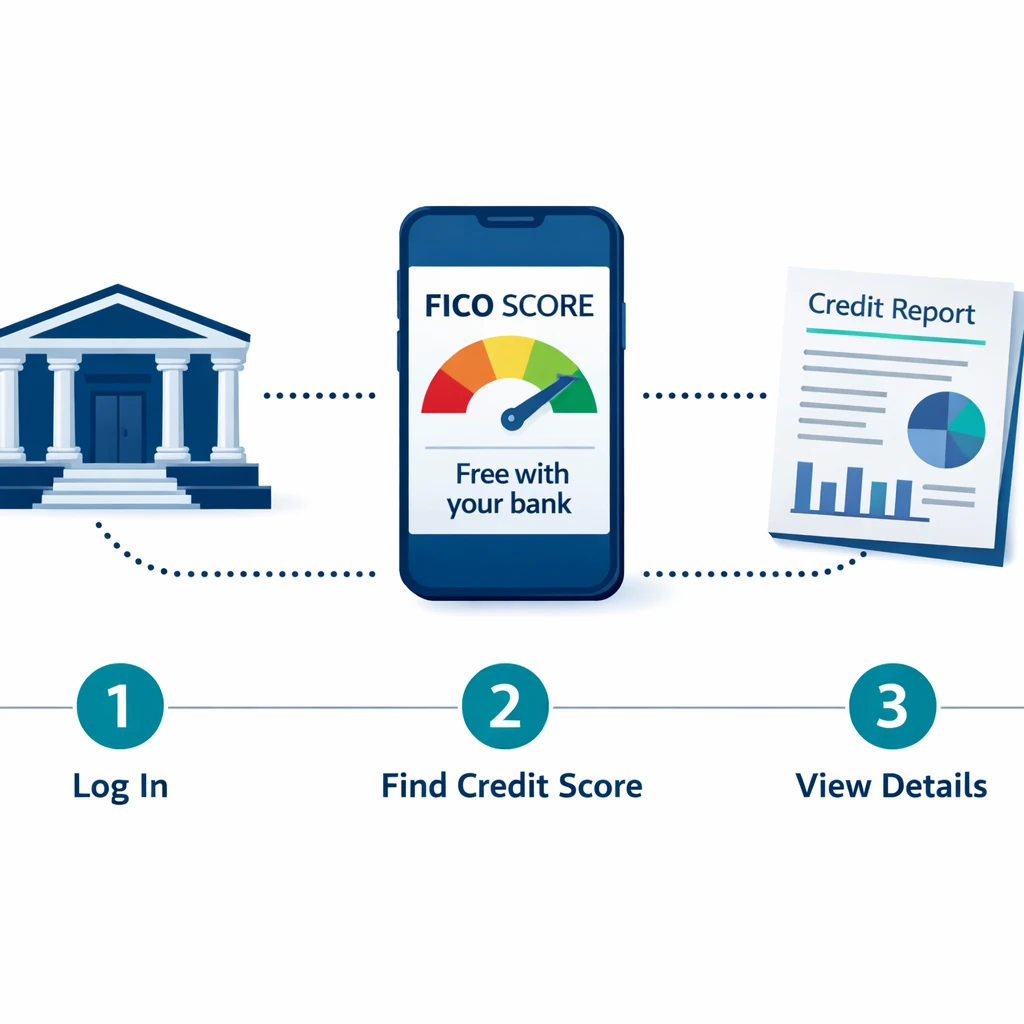

Part 1: The Short Answer—Yes, You Probably Already Have Access

If you’re in a hurry, here’s the short version:

Yes. Most major banks and credit unions now offer free FICO scores to their customers.

You don’t need to sign up for anything. You don’t need to pay a fee. You don’t need to enter a credit card.

You just need to log in to your online banking or mobile app and look for a section called:

- “Credit Score”

- “FICO Score”

- “Credit Health”

- “Financial Wellness”

It’s usually hiding in the same place as your account statements, your credit card rewards, or your financial tools. A few clicks, and it’s there. Waiting for you. Free.

And the best part? Checking it doesn’t hurt your credit, because it’s a soft inquiry .

🤔 Pause and Think:

When’s the last time you actually explored your bank’s app? Like, really clicked through all the menus? Your free FICO score has been sitting there the whole time.

Part 2: Why FICO Matters More Than Those Other Scores

Before we get into the “how,” let’s talk about the “why.”

You’ve probably seen free credit scores from sites like Credit Karma, Credit Sesame, or NerdWallet. Those are useful tools. But they usually give you VantageScore, not FICO .

FICO vs. VantageScore: The Showdown

Both scores range from 300 to 850. Both look at similar factors. But they’re calculated differently, and they’re used differently.

FICO:

- Created by the Fair Isaac Corporation in 1989 .

- Used in 90% of lending decisions in the United States .

- When a mortgage lender, auto dealer, or credit card issuer pulls your credit, they’re almost certainly looking at a FICO score .

- Different industries use different FICO versions (FICO Auto Score for car loans, FICO Bankcard Score for credit cards, etc.) .

VantageScore:

- Created jointly by the three credit bureaus (Equifax, Experian, TransUnion) in 2006 .

- Used by some lenders, but far less common than FICO .

- Popular on consumer websites because it’s cheaper for them to provide .

- Still a valid score, but not the one most lenders see .

The “Lenders Use This” Factor

Here’s why this matters:

If you check your Credit Karma score and see 720, you might think you’re in great shape. But if your lender pulls your FICO score and sees 680, you could get a higher interest rate—or even a denial.

The FICO score from your bank is the real score . It’s the one lenders actually use. It’s not a “educational score” or a “simulated score.” It’s the number that determines whether you get approved and what interest rate you pay .

how to improve credit score before applying for a mortgage

📊 FICO Score Breakdown

Category Weight Payment History 35% Amounts Owed 30% Length of Credit History 15% Credit Mix 10% New Credit 10% Source: myFICO.com

Part 3: The FICO Score Open Access Program—Your Secret Weapon

So how did all these banks suddenly start giving away free FICO scores?

It’s not charity. It’s the FICO Score Open Access program .

How Open Access Works

FICO partnered with over 200 financial institutions—banks, credit unions, and even credit counseling organizations—to let them offer free FICO scores to their customers .

The banks pay FICO for the scores. They give them to you for free. Everyone wins:

- You get your real FICO score without paying.

- The bank builds customer loyalty and trust.

- FICO gets more people familiar with their brand.

- is it better to rent or buy a home right now?

Why Banks Joined This Program

Banks realized that customers who understand their credit are better customers. They’re more likely to qualify for loans, less likely to default, and more likely to use the bank’s products.

So they started offering free scores as a perk. And now it’s so common that if your bank doesn’t offer it, they’re behind the times .

💡 The Secret:

More than 138 banks, credit unions, and financial websites now offer free credit scores. FICO alone has over 200 partners. You have options .

Part 4: Major Banks That Give You Free FICO Scores

Here’s the list you’ve been waiting for. These major banks all offer free FICO scores to customers .

Bank of America

What they offer: FICO Score (based on TransUnion data)

Who gets it: Credit cardholders

Where to find it: Online banking or mobile app under “Account Details” or “Financial Wellness”

Bank of America was one of the early adopters of free FICO scores. If you have a Bank of America credit card, your score is waiting for you .

mortgage pre-approval process step-by-step

Chase

What they offer: Chase Credit Journey (VantageScore from Experian)

Who gets it: Anyone (you don’t even need to be a Chase customer)

Where to find it: Chase mobile app or chase.com/creditjourney

Technically, Chase uses VantageScore, not FICO. But it’s free, it’s updated weekly, and it includes credit monitoring. If you’re a Chase customer, check the app .

Citi

What they offer: FICO Bankcard Score 8 (based on Experian data)

Who gets it: Citi cardholders

Where to find it: Online banking under “Account Management” or “Credit Score”

Citi provides FICO scores to all cardholders. You’ll see it when you log in to manage your credit card .

Capital One

What they offer: FICO Score (based on TransUnion data)

Who gets it: Anyone (you don’t need to be a Capital One customer)

Where to find it: Capital One mobile app or capitalone.com/creditwise

Capital One’s CreditWise tool is free for everyone, not just customers. It gives you your TransUnion VantageScore, plus credit monitoring. For FICO specifically, Capital One cardholders can see their score in the app .

Wells Fargo

What they offer: FICO Score 9 (based on Experian data)

Who gets it: Wells Fargo consumer customers (checking accounts, credit cards, etc.)

Where to find it: Online banking under “Account Summary” or “Credit Score”

Wells Fargo provides FICO scores to customers through their online banking portal .

Discover

What they offer: FICO Score 8 (based on Experian data)

Who gets it: Anyone (even non-customers)

Where to find it: discover.com/credit-scorecard

FHA loan vs Conventional loan requirements

Discover is the hero of this story. They were the first major issuer to offer free FICO scores to everyone, not just their own cardholders . You don’t need a Discover card. You don’t need to sign up for anything. Just go to their website and check your score. It’s updated monthly and includes credit monitoring .

U.S. Bank

What they offer: VantageScore 3.0 (based on TransUnion data)

Who gets it: U.S. Bank customers

Where to find it: Online banking or mobile app

U.S. Bank provides VantageScore to customers through its digital banking platform .

PNC

What they offer: FICO Score

Who gets it: PNC customers with eligible accounts

Where to find it: Online banking

PNC offers FICO scores to customers through its online banking portal.

Truist

What they offer: VantageScore (based on Experian data)

Who gets it: Truist customers

Where to find it: Online banking or mobile app

Truist (the merger of BB&T and SunTrust) offers credit scores to customers through their digital tools .

how much house can I afford on a $70,000 salary?

FNBO (First National Bank of Omaha)

What they offer: FICO Score

Who gets it: FNBO customers

Where to find it: Online banking

FNBO partners with FICO to give customers free access to their scores, along with educational resources about credit factors .

Part 5: Credit Unions That Offer Free FICO Scores

Credit unions are often ahead of banks when it comes to member benefits. Here are some that offer free FICO scores .

Navy Federal Credit Union

What they offer: FICO Score

Who gets it: Navy Federal members

Where to find it: Online banking or mobile app

Navy Federal, the largest credit union in the U.S., provides FICO scores to its members .

PenFed Credit Union

What they offer: FICO Score (based on Experian data)

Who gets it: PenFed members

Where to find it: Online banking

PenFed offers FICO scores to members through its online platform .

Mountain America Credit Union

What they offer: FICO Score

Who gets it: Members with a checking account or loan

Where to find it: Mobile app

Mountain America provides free FICO scores to members through their mobile banking app .

Rogue Credit Union

What they offer: FICO Score

Who gets it: Members

Where to find it: Online banking or mobile app under “Financial Wellness”

Rogue Credit Union offers free FICO scores to members, updated every two months, along with tools to track progress and understand score factors .

Digital Federal Credit Union (DCU)

What they offer: FICO Score (based on Equifax data)

Who gets it: DCU members

Where to find it: Online banking

DCU provides FICO scores to members through their online banking portal .

first-time home buyer grants and programs 2024

State Employees’ Credit Union

What they offer: FICO Score

Who gets it: Qualifying members

Where to find it: Online banking

SECU offers FICO scores to members who meet certain criteria .

Affinity Federal Credit Union

What they offer: FICO Score

Who gets it: Affinity members

Where to find it: Online banking

Affinity provides FICO scores to members through their digital banking tools .

And this is just a sample. Nav’s 2026 list includes dozens more credit unions offering free scores .

Part 6: What If You Don’t Have an Account? (No Problem)

Maybe you don’t have a bank account. Maybe your bank doesn’t offer FICO scores. Maybe you just want another option.

You still have free ways to get your FICO score.

Option 1: Open a Free Account

Open a free checking account or savings account at any of the banks listed above. Many have no monthly fees and no minimum balance. Once you’re in, your FICO score is waiting.

Option 2: Use Discover’s Credit Scorecard (Open to Everyone)

This is the easiest option. Go to discover.com/credit-scorecard. No Discover card required. No credit card needed. Just your name, address, and Social Security number .

You’ll get:

- Your FICO Score 8 (based on Experian data)

- Updated monthly

- Credit monitoring alerts

- Social Security number monitoring

Discover pioneered this in 2016, and it’s still one of the best free tools out there .

is debt consolidation a good idea?

Option 3: Experian’s Free Tier

Experian offers free access to your FICO Score 8 through its website and mobile app .

Go to experian.com/freecreditscore or download the Experian app. You’ll get:

- Your Experian FICO Score

- Your Experian credit report

- Basic credit monitoring

- Updated every 30 days

No credit card required. Free forever .

Option 4: FICO’s Own Free Program

FICO itself now offers free scores to everyone. Through their partnership with Equifax, you can get your FICO Score 8 (based on Equifax data) for free, along with monthly Equifax credit monitoring .

Part 7: How to Find Your Free Score in Your Bank’s App

If you have a bank account but can’t find your score, here’s how to hunt it down.

The Treasure Hunt Method

Step 1: Log in to your online banking or mobile app.

Step 2: Look for these sections:

- Account summary or dashboard

- Credit card details (if you have a card with them)

- Financial wellness tools

- Security center

- Help or support

- “More” menu (often where hidden features live)

Step 3: Search for these terms:

- “Credit score”

- “FICO score”

- “Credit health”

- “Financial wellness”

- “Credit monitoring”

Step 4: Click around.

I know that sounds vague, but every bank organizes things differently. You might have to tap through a few screens. It’s worth it.

What to Look For

Once you find it, you’ll typically see:

- Your three-digit score

- A graph showing your score over time

- Factors affecting your score (like payment history or utilization)

- Tips to improve

Take a screenshot. You earned it.

🤔 Think About This:

If your bank’s app has a search function, type “credit score” right now. You might find it in 10 seconds.

Part 8: What to Do If Your Bank Doesn’t Offer It

Maybe you checked and your bank doesn’t offer free FICO scores. Now what?

Option 1: Ask them. Call customer service or send a message through online banking. Ask: “Do you offer free FICO scores to customers?” Sometimes it’s available but hidden, or only for certain account types.

Option 2: Switch banks. If free FICO scores matter to you (and they should), consider moving your money to a bank that offers them. Many online banks have no fees and great apps.

Option 3: Use one of the free options above. Discover, Experian, and FICO itself all offer free scores to anyone. You don’t need to switch banks.

Part 9: Common Questions About Free Bank FICO Scores

Is it really free?

Yes. No fees, no subscriptions, no trials that turn into charges. Banks pay for this as a customer perk .

Does checking it hurt my credit?

No. This is a soft inquiry, which doesn’t affect your score at all .

How often is it updated?

Most banks update monthly. Some update weekly or with every statement .

Which version of FICO am I seeing?

Most banks show FICO Score 8, but some show industry-specific versions (like FICO Bankcard Score 8) .

Why is it different from my Credit Karma score?

Credit Karma usually shows VantageScore, which is calculated differently. Your bank’s FICO score is the one lenders actually use .

Do I need to have a credit card with the bank?

Sometimes. Some banks only offer FICO scores to credit card customers. Others offer it to anyone with a checking account .

Can I get my score if I only have a savings account?

It depends on the bank. Some require a checking account or credit card. Check your bank’s policy.

Part 10: What to Do With Your Free FICO Score

Okay, you found it. Now what?

Step 1: Don’t Panic

Whatever number you see, it’s just data. It’s not who you are. It’s just where you are right now.

Step 2: Look at the Factors

Most bank score tools show you what’s helping and hurting your score:

- Payment history: Are there any late payments?

- Utilization: How much of your available credit are you using?

- Length of history: How old are your accounts?

- New credit: Have you applied for anything recently?

These factors tell you what to work on .

Step 3: Track It Over Time

Check your score monthly. Watch it go up as you pay down debt and make on-time payments. Watch it dip if you miss something (so you can fix it fast).

Step 4: Plan Your Next Move

- If your score is below 580, focus on building positive history (secured cards, credit-builder loans).

- If it’s 580-669, work on paying down balances and catching up any late payments.

- If it’s 670-739, you’re in good shape—maintain it.

- If it’s 740+, you’re golden. Enjoy those low interest rates .

Frequently Asked Questions

Q: How do I get my free FICO score from my bank?

A: Log in to your online banking or mobile app and look for “Credit Score,” “FICO Score,” or “Financial Wellness.” Most major banks offer it .

Q: Which banks offer free FICO scores?

A: Bank of America, Citi, Capital One, Wells Fargo, Discover, FNBO, and many others. Credit unions like Navy Federal, PenFed, and Mountain America also offer them .

Q: Is the FICO score from my bank accurate?

A: Yes. It’s the same score lenders see when they pull your credit .

Q: How often is my FICO score updated?

A: Most banks update monthly. Some update weekly or with every credit card statement .

Q: Does checking my FICO score through my bank hurt my credit?

A: No. This is a soft inquiry and doesn’t affect your score .

Q: What if my bank doesn’t offer free FICO scores?

A: Use Discover’s Credit Scorecard (open to everyone), Experian’s free tier, or FICO’s free program .

Q: Is Credit Karma a FICO score?

A: Usually not. Credit Karma provides VantageScore, which is different from FICO .

Q: Why is my FICO score different from my Credit Karma score?

A: Different scoring models. FICO and VantageScore weigh factors differently .

Q: Do I need a credit card to get my free FICO score?

A: Sometimes. Some banks only offer scores to credit card customers. Others offer them to anyone with a checking account .

Q: Can I get my FICO score for free without a bank account?

A: Yes. Use Discover’s Credit Scorecard, Experian’s free tier, or FICO’s free program .

Q: What’s a good FICO score?

A: Generally, 670-739 is considered good. 740+ is very good to exceptional .

The Emotional Bottom Line

Look, I’m not going to pretend that checking your credit score is fun.

It can be scary. It can be disappointing. It can feel like looking at a report card from a class you barely passed.

But here’s the thing: You can’t fix what you don’t see.

That free FICO score sitting in your bank app? It’s not just a number. It’s a tool. It’s a map. It’s the first step toward better interest rates, better loan terms, and better financial opportunities.

And the best part? You’ve already paid for it. Every month you keep money in that bank, every credit card bill you pay, every time you log in—you’ve earned that free score.

So go find it. Right now. Open your banking app. Click around. Take those 60 seconds.

Your future self—the one getting approved for that mortgage, that car loan, that dream credit card—will thank you.

You’ve got this.