The Ultimate Guide: How Much to Save for Retirement by Age 30, 40, and 50

By Peiman Daneshgar

Table of Contents

- Introduction: The Power of Milestones

- Why Retirement Planning is Different in 2026

- The Golden Rules: Two Ways to Calculate Your Target

- How Much to Save for Retirement by Age 30

- How Much to Save for Retirement by Age 40

- How Much to Save for Retirement by Age 50

- A Note for Our European Readers

- The Math Behind the Multiples: Why Starting Early Matters

- What If You’re Behind? A Catch-Up Plan

- Advanced Strategies for 2026

- Frequently Asked Questions

- Conclusion: Your Future Self Will Thank You

Introduction: The Power of Milestones

Planning for retirement can feel like navigating a ship across an endless ocean. The destination is clear—a comfortable and secure future—but the route can seem hazy, and the sheer distance can be daunting. One of the most common and pressing questions for anyone on this journey is: “How much to save for retirement by age 30, 40, and 50?”

These age milestones are not arbitrary numbers. They are powerful checkpoints that allow you to measure your progress, adjust your sails, and ensure you are on course. Whether you are just starting your career or are in your peak earning years, having a clear target is the first step to hitting it. In the financial landscape of 2026, with evolving contribution limits and shifting economic tides, having a firm grasp on these benchmarks is more critical than ever.

This guide is designed to provide you with definitive, research-backed answers. We will explore the most respected guidelines from leading financial institutions, break down the “why” behind the numbers, and provide a roadmap for both US and European investors to achieve their retirement goals. By the end of this article, the question of how much to save for retirement by age 30, 40, and 50 will be transformed from a source of anxiety into a clear, actionable plan.

Why Retirement Planning is Different in 2026

Before diving into the specific numbers, it’s important to understand the context of retirement planning in the current year.

1. Increased Contribution Limits

The IRS has adjusted contribution limits for 2026, providing a greater opportunity to save on a tax-advantaged basis :

- 401(k), 403(b), and most 457 plans: The employee contribution limit has increased to $24,500. For those aged 50 and over, the catch-up contribution is $8,000, bringing the total to $32,500. Notably, a new provision allows those aged 60-63 to make even higher catch-up contributions of up to $11,250 .

- IRAs (Traditional and Roth): The total contribution limit is now $7,500, with a $1,100 catch-up for those 50 and older .

2. The “Secure Act 2.0” Changes

A significant rule took effect on January 1, 2026. Under the SECURE 2.0 Act, if you are aged 50 or older and earned more than $150,000 in FICA wages in the previous year, your 401(k) catch-up contributions must be made to a Roth account . This means you pay taxes on these contributions now in exchange for tax-free withdrawals in retirement, a crucial consideration for high-earners approaching retirement.

how to create a budget for beginners step by step

3. Evolving Withdrawal Rate Strategies

The classic “4% Rule” is being revisited. Recent market data and analyses suggest that a slightly higher initial withdrawal rate, perhaps 4.7%, might be sustainable for a 30-year retirement, offering a bit more income for retirees .

Understanding these 2026-specific factors is essential when calculating how much you need to save.

best budgeting method for irregular income

The Golden Rules: Two Ways to Calculate Your Target

There are two primary, complementary ways to think about your retirement savings goals: the Income Multiplier Method and the 4% Rule. Both help answer the question of how much to save for retirement by age 30, 40, and 50.

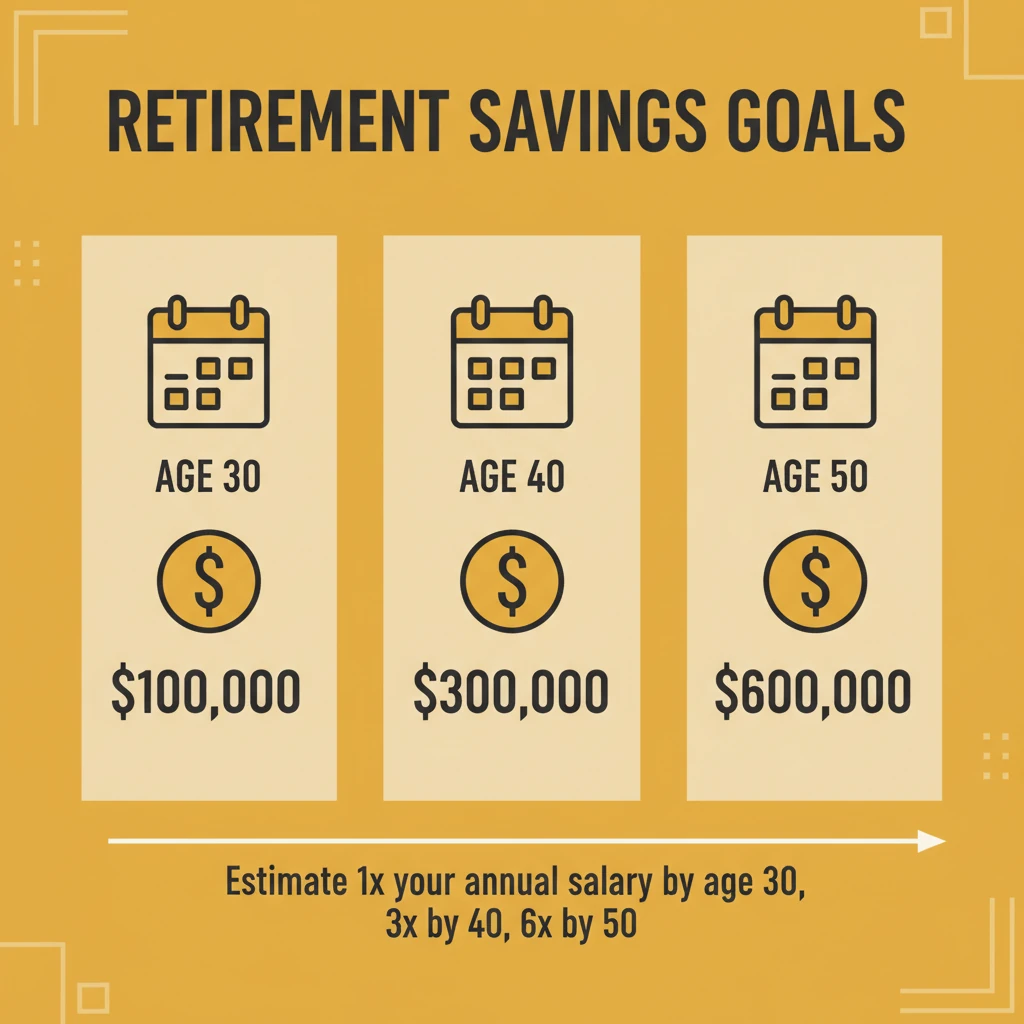

Method 1: The Income Multiplier (Your Age-Based Benchmark)

This is the most straightforward and widely recommended method. It suggests that by certain ages, you should have a multiple of your annual salary saved. The table below consolidates guidelines from leading financial experts like Fidelity, Schwab, and T. Rowe Price .

| Age | Target Retirement Savings (Multiple of Annual Salary) |

|---|---|

| 30 | 1x |

| 40 | 3x |

| 50 | 6x |

| 60 | 8x |

| 67 | 10x |

How to Use This Table:

- Find your current age in the left column.

- Multiply your current gross annual salary by the corresponding number.

- The result is a general estimate of what your total retirement savings (in all accounts combined) should be.

- 50/30/20 rule calculator excel template free

Important Nuances:

- Income Level: If you earn over $250,000, you may need to aim for the higher end of the multiplier ranges, as Social Security will replace a smaller percentage of your pre-retirement income .

- Lifestyle Goals: If you plan to travel extensively or have expensive hobbies in retirement, aim higher. If you expect a more modest lifestyle, the lower end of the range may suffice .

- Pensions: If you have a generous defined-benefit pension, you can factor that into your calculations and potentially aim for a lower multiplier.

Method 2: The 4% Rule (Your Final Number)

The 4% Rule helps you determine the total nest egg you need on the day you retire. Created by financial planner William Bengen, it states that if you withdraw 4% of your portfolio in your first year of retirement, and then adjust that dollar amount for inflation each subsequent year, your savings should last for 30 years .

how to save money on a tight income

Example:

If you estimate you will need $60,000 per year in retirement to live comfortably:

$60,000 / 0.04 = $1,500,000

You would need a $1.5 million portfolio to generate that income stream. In 2026, Bengen himself has suggested that a 4.7% withdrawal rate might be safe for new retirees, which would lower the required nest egg slightly .

How Much to Save for Retirement by Age 30

Reaching age 30 is a significant financial milestone. By now, the habits of your 20s should be solidifying into a sustainable financial plan.

The Benchmark: 1x Your Annual Salary

If you earn $60,000 at age 30, you should aim to have approximately $60,000 saved across all your retirement accounts .

Your Financial Focus in Your 30s

- Harness the Power of Compounding: Your greatest ally is time. A dollar saved at 30 has decades to grow. For example, investing $7,000 a year starting at age 25 could grow to over $2.1 million by age 67, while waiting until 35 to start could cut that number in half . This exponential growth is the magic of compound interest .

- Prioritize Employer Match: If you have a 401(k) with an employer match, this is the closest thing to “free money” in finance. Contribute at least enough to get the full match .

- Build an Emergency Fund: Aim for 3-6 months of living expenses in a readily accessible savings account. This protects your retirement savings from being raided for unexpected car repairs or medical bills .

- Automate Your Savings: Set up automatic contributions to your 401(k) and IRA. This “pay yourself first” strategy ensures you save consistently without having to think about it .

- money saving challenges for couples

How Do You Compare? (UK Data)

For our European readers, particularly in the UK, data from HMRC provides a snapshot of how others are saving. For the 25-34 age group, the average ISA savings is £10,556, and the median pension pot is £18,800 . Remember, these are averages that include many who are not on track, so aiming for the 1x salary benchmark is a more robust goal.

How Much to Save for Retirement by Age 40

Your 40s are often considered the “peak earning years.” Financial responsibilities are typically at their highest, with mortgages and childcare costs, but it’s also a critical time to accelerate your savings.

The Benchmark: 3x Your Annual Salary

If you earn $100,000 at age 40, your target savings should be approximately $300,000 .

Your Financial Focus in Your 40s

- Maximize Contributions: With your income likely at its peak, strive to max out your 401(k) and IRA contributions. For 2026, that’s a powerful combination of up to $32,000 ($24,500 + $7,500) in tax-advantaged space .

- Review Your Asset Allocation: Your investment strategy should mature. While you still have a long time horizon, it’s wise to start dialing down the risk slightly. A common rule of thumb is to hold a higher percentage of stocks in your 20s and 30s, and gradually increase your allocation to bonds as you age to protect your nest egg from market volatility .

- Plug Spending Leaks: Review your bank and credit card statements. Identify subscriptions you don’t use or areas where you can cut back, like dining out. Redirect that cash flow to your retirement accounts .

- Get Serious About Projections: Start using online retirement calculators to model different scenarioser picture of your projected expenses in retirement and identify any potential income gaps .

- sinking funds: what are they and how to set them up

How Do You Compare? (UK Data)

For the 35-44 age group in the UK, the average ISA savings is £14,254, and the median pension pot is £39,500 . The jump from the 30s benchmark is clear, but aiming for 3x your salary remains the gold standard for a comfortable retirement.

How Much to Save for Retirement by Age 50

Age 50 is a pivotal moment. It’s the “final stretch” before retirement. The government recognizes this by allowing “catch-up contributions.” This is the time for a final assessment and a concerted push.

The Benchmark: 6x Your Annual Salary

If you earn $120,000 at age 50, you should aim to have approximately $720,000 saved .

Your Financial Focus in Your 50s

- Aggressively Use Catch-Up Contributions: Take full advantage of the higher contribution limits for those over 50. For 2026, you can contribute up to $32,500 to your 401(k) and up to $8,600 to your IRA ($7,500 + $1,100 catch-up) . This is your most powerful tool to accelerate your savings.

- Map Out Retirement Income Sources: Start to formalize your vision. What age will you claim Social Security? (Remember, delaying past your full retirement age increases your benefit by about 8% per year up to age 70 ). Do you have a pension? What will your healthcare costs look like? .

- Test Your Retirement Budget: Try living on your projected retirement budget for a few months. This “test run” can reveal hidden costs and help you refine your spending assumptions .

- Consider Long-Term Care: Healthcare is one of the biggest unknowns in retirement. Explore options like long-term care insurance to protect your savings from being depleted by a major health event .

How Do You Compare? (UK Data)

For the 45-54 age group in the UK, the average ISA savings is £25,316, and the median pension pot is £80,000 . The gap between these averages and the 6x salary benchmark highlights the challenge many face, but it also underscores the importance of the 50s as a decade for supercharged saving.

best cash envelope system wallets 2024

A Note for Our European Readers

While the benchmarks in this article (1x, 3x, 6x) are based on US research, the core principles are universal and provide excellent targets for European investors. However, there are key differences to keep in mind.

- State Pensions are Often More Robust: Many European countries (like France, Germany, and the Nordic nations) have more generous state pension systems than the US Social Security. This means your personal savings might not need to replace as much of your pre-retirement income. The income multiplier targets could be adjusted downward slightly.

- Different Tax-Advantaged Vehicles: Your savings will likely be in vehicles like a Stocks and Shares ISA (UK), a PEL (France), or a Riester-Rente (Germany). The tax treatment of contributions and withdrawals varies significantly by country.

- The “25-Year” Standard: In the UK, a 25-year mortgage is common, and retirement planning often revolves around being mortgage-free by retirement. The Fidelity UK guidelines recommend slightly different multiples, such as 1x by 30, 2x by 40, 4x by 50, and 6x by 60 . This reflects a different balance between state and private pension expectations.

- Focus on the Percentage: For European readers, the most important takeaway is the savings rate. Aim to save 12-15% of your gross income annually, including any employer contributions . This consistent habit is the true driver of long-term success, regardless of which country you call home.

- zero-based budgeting vs. 50/30/20 rule

The Math Behind the Multiples: Why Starting Early Matters

To truly understand how much to save for retirement by age 30, 40, and 50, you must appreciate the math of compounding. Let’s look at a hypothetical example.

The Scenario:

- Target Retirement Age: 67

- Target Nest Egg: $1.5 Million (to generate ~$60,000/year using the 4% Rule)

The Saver:

- Starts at Age 25: Needs to save approximately $700 per month (assuming a 7% average annual return) to reach $1.5M by 67.

- Starts at Age 35: Needs to save approximately $1,400 per month—double the amount—to reach the same goal.

- Starts at Age 45: Needs to save approximately $3,000 per month to catch up .

This dramatic increase illustrates the “double whammy” of waiting: you have fewer years for your money to grow, and you must save much more each month to compensate. This is why hitting the 1x by 30 benchmark is so powerful; it puts the forces of compounding to work for you, not against you.

What If You’re Behind? A Catch-Up Plan

If you’ve reviewed the benchmarks and feel you’re behind, do not panic. Financial futures are built with consistent action, not perfection. Here is a step-by-step catch-up plan.

Step 1: Don’t Panic, Do Act

The worst thing you can do is nothing. Acknowledging the gap is the first step to closing it .

Step 2: Save More Now

- Increase Your 401(k) Contribution: Boost your contribution by just 1% or 2%. You likely won’t miss it from your paycheck, but it will make a huge difference over time .

- Automate the Increase: Set up an automatic annual increase of 1% on your 401(k) contributions. This is a painless way to steadily boost your savings rate .

- Capture the Full Employer Match: If you aren’t already, prioritize getting every dollar of free money your employer offers .

- how to stop impulse buying online

Step 3: Slash Expenses and Debt

- Conduct a Spending Audit: Use a budgeting app or review your statements. Cut unused subscriptions and reduce discretionary spending like dining out .

- Attack High-Interest Debt: Paying off a credit card with an 18% interest rate is a guaranteed 18% return on your money. Use the “avalanche” method (focus on the highest interest rate first) or the “snowball” method (focus on the smallest balance first) to eliminate this wealth killer .

Step 4: Stay Flexible

- Consider Working Longer: Even an extra year or two of work can significantly boost your savings and delay the need to tap into them .

- Plan for Part-Time Work in Retirement: A “phased retirement” with a part-time job can reduce the drawdown on your portfolio and provide extra income.

- Reassess Your Retirement Lifestyle: Be open to a slightly more modest retirement vision. The goal is a happy and secure retirement, which is often more about flexibility and planning than hitting an arbitrary number .

Advanced Strategies for 2026

Once you’re on track with the basics, consider these advanced strategies for 2026.

The “Backdoor” and “Mega Backdoor” Roth IRA

For high earners whose income exceeds the limits for direct Roth IRA contributions, the “backdoor Roth IRA” is a legal loophole that allows you to convert a Traditional IRA to a Roth. Some 401(k) plans even allow for a “mega backdoor Roth,” which lets you contribute after-tax money to your 401(k) and then convert it to a Roth, supercharging your tax-free savings.

The Power of an HSA as a Retirement Vehicle

A Health Savings Account (HSA) is a “triple tax-advantaged” powerhouse .

- Contributions are tax-deductible.

- The money grows tax-free.

- Withdrawals for qualified medical expenses are tax-free.

After age 65, you can withdraw funds for any purpose without penalty (though you’ll pay ordinary income tax on non-medical withdrawals). For 2026, you can contribute up to $4,400 for individual coverage and $8,750 for family coverage, plus a $1,000 catch-up for those 55+ . Maxing out your HSA and investing it for the long term is one of the smartest retirement moves you can make.

Optimize Your Withdrawal Strategy

As you approach retirement, your strategy shifts from accumulation to distribution. Work with a financial planner to create a tax-efficient withdrawal order. This might involve drawing from taxable accounts first, letting your tax-deferred accounts (Traditional 401k/IRA) grow longer, and preserving your tax-free Roth accounts for last .

Frequently Asked Questions

Q1: Is the 1x salary by 30 benchmark realistic for everyone?

While challenging, it’s a powerful goal. The most important thing is to establish a high savings rate early. Even if you have 0.5x saved by 30, you’re on the right track. The key is to start now and be consistent .

Q2: What counts as “retirement savings” for these benchmarks?

This includes all money specifically earmarked for retirement: 401(k)s, 403(b)s, IRAs (Traditional and Roth), SEP IRAs, and taxable brokerage accounts that you intend to use for retirement. It does not include your emergency fund or the equity in your home (unless you plan to sell and downsize in retirement).

Q3: I’m 45 with nothing saved. Is it too late?

Absolutely not. It’s not too late, but it requires urgent and aggressive action. You need to maximize your 401(k) and IRA contributions, utilize catch-up contributions when you turn 50, and potentially plan to work a few years longer than you originally intended .

Q4: How do Social Security or a state pension affect these numbers?

They reduce the amount you need to save. The income multiplier method is a simple starting point. A more precise method is to estimate your annual retirement expenses, subtract your expected Social Security or state pension income, and then apply the 4% Rule to the remaining amount to find the nest egg you need to fund yourself .

Q5: Should I prioritize paying off debt or saving for retirement?

It depends on the interest rate. If you have high-interest debt (like credit cards over 10-15%), prioritize paying that off first—it’s a guaranteed return. If you have low-interest debt (like a mortgage under 5%), it’s generally better to prioritize investing for retirement, especially if you have access to an employer match .

Q6: What is the ideal savings rate?

Most financial experts recommend saving 15% of your gross income per year for retirement, including any employer match . If you started later, you may need to bump that up to 20-25%.

Q7: How do the 2026 contribution limits affect my plan?

The higher limits ($24,500 for 401(k)s and $7,500 for IRAs) give you more tax-advantaged space to save. If you can afford to, increasing your contributions to these new limits is a fantastic way to accelerate your progress .

Q8: What is the best investment mix for my 401(k)?

A common rule of thumb is to hold a diversified portfolio of low-cost index funds. A popular choice is a Target-Date Fund, which automatically adjusts your asset allocation (stocks vs. bonds) to become more conservative as you approach your target retirement date.

Q9: How do I calculate my target if my income changes?

Your retirement savings target is a moving goalpost. You should recalculate it annually. If you get a raise, try to save a portion of it rather than spending it all. This keeps your savings multiple on track .

Q10: Should I pay a financial advisor?

For many people, especially as their finances become more complex in their 40s and 50s, a fee-only fiduciary financial advisor can provide immense value. They can help you create a comprehensive retirement plan, optimize your tax strategy, and provide the discipline to stay the course .

Conclusion: Your Future Self Will Thank You

Understanding how much to save for retirement by age 30, 40, and 50 transforms a vague anxiety into a clear set of goals. The benchmarks of 1x, 3x, and 6x your salary are not about creating stress; they are about providing a roadmap. They illuminate the path and help you measure your progress.

Whether you are right on track, slightly behind, or even ahead, the most important step is the next one. In the 2026 landscape of higher contribution limits and new tax rules, the opportunities to save have never been greater. Start where you are. Automate your savings, capture your employer match, and harness the incredible power of compounding.

The journey to a secure retirement is a marathon, not a sprint. By understanding these milestones and taking consistent, deliberate action, you are not just saving money; you are building the foundation for the future life you deserve. Your future self will thank you for the clarity and discipline you apply today.