The Ultimate Guide: Best Target-Date Funds for 2045 Retirement

By Peiman Daneshgar

Table of Contents

- Introduction: The Simplicity of Target-Date Funds

- What is a Target-Date Fund and How Does It Work?

- Why 2045 is a Pivotal Retirement Year

- How We Evaluated the Best 2045 Target-Date Funds

- The Best Target-Date Funds for 2045 Retirement

- Detailed Fund Analysis

- Active vs. Passive: Understanding the Construction

- Glide Paths: Not All Funds Are Created Equal

- Fees: The Certainty in an Uncertain World

- Where to Access These Funds

- Frequently Asked Questions

- Conclusion

Introduction: The Simplicity of Target-Date Funds

For millions of Americans saving for retirement, the question isn’t whether to invest, but how. With thousands of mutual funds, ETFs, and individual stocks available, the sheer volume of choices can be paralyzing. This is where target-date funds (TDFs) have become the dominant solution, particularly in employer-sponsored 401(k) plans. They offer a simple, elegant answer to a complex problem: a single fund that handles asset allocation, diversification, and rebalancing automatically.

For those planning to retire around the year 2045, choosing the right fund is a decision that will compound over nearly two decades of work and then support you through decades of retirement. But with so many options from Vanguard, Fidelity, T. Rowe Price, and others, how do you identify the best target-date funds for 2045 retirement?

This comprehensive guide will answer that question definitively. We will analyze the leading 2045 target-date funds using the most current 2026 data, evaluating them on fees, performance, risk-adjusted returns, and investment philosophy. Whether you are a DIY investor or simply want to understand the default option in your 401(k), this guide will provide the clarity you need to make an informed decision about the best target-date funds for 2045 retirement.

What is a Target-Date Fund and How Does It Work?

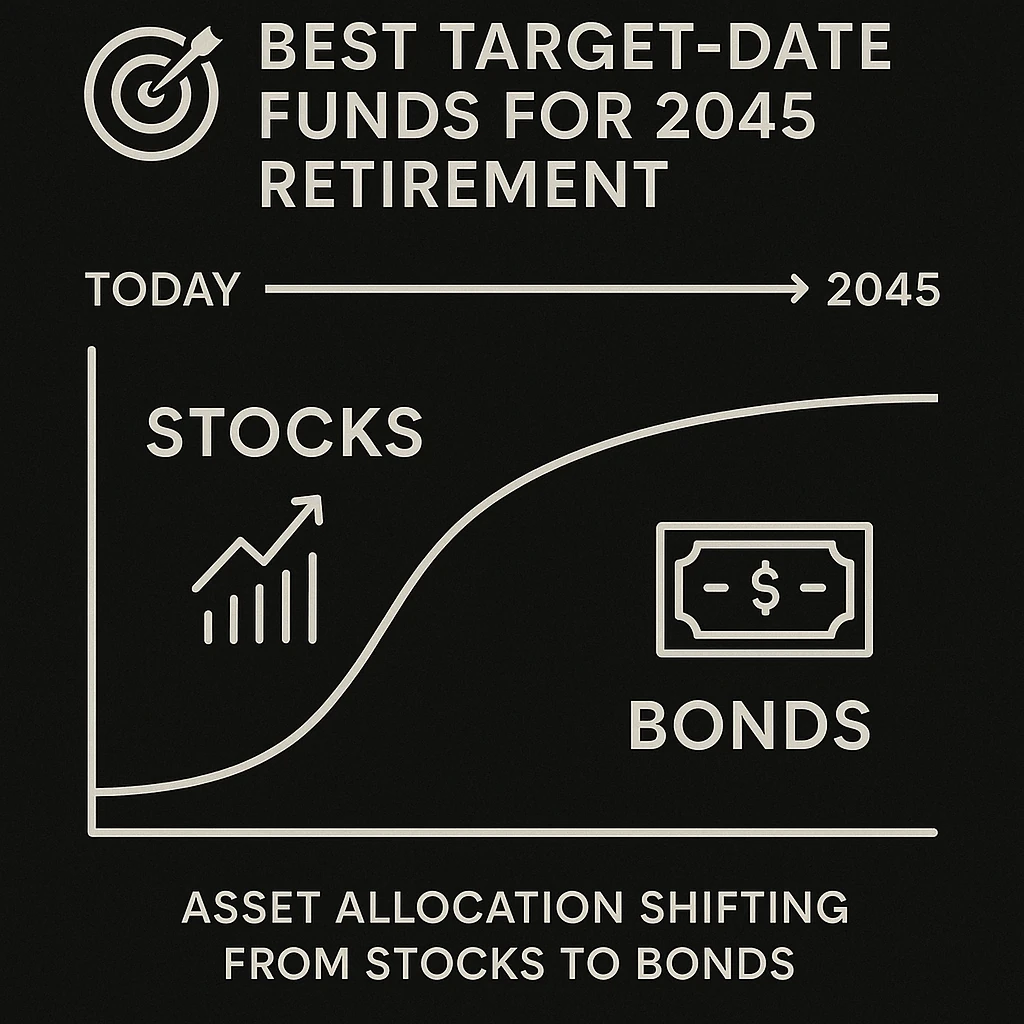

A target-date fund is a mutual fund or collective investment trust offered by an investment company that automatically adjusts its asset allocation—the mix of stocks, bonds, and other investments—to become more conservative as a specified “target” retirement date approaches .

best stocks for dividend income for beginners

The Core Concept: Set It and Forget It

The primary appeal of a target-date fund is its simplicity. By investing in a single fund, you gain exposure to a globally diversified portfolio that is professionally managed and rebalanced for you .

The Glide Path

The fund’s changing asset allocation over time is known as its “glide path.” In the early years, when retirement is far away, the fund is heavily weighted toward stocks (equities) to maximize growth potential. As the target date nears, the fund gradually shifts toward bonds and cash equivalents to preserve capital and reduce volatility .

Beyond the Target Date

Many target-date funds continue to evolve after the target date, eventually settling into a final “retirement income” or “distribution” phase. This phase is designed to provide ongoing income and preservation for retirees who may live another 20-30 years .

how to invest in S&P 500 from Europe (or UK, Germany, etc.)

Why 2045 is a Pivotal Retirement Year

The year 2045 is approximately 19 years from now. For an investor targeting retirement in 2045, this represents a critical transition point in their financial lifecycle .

The Transition Zone

According to industry analysis, 2045 target-date funds typically sit at a “transition point” on the glide path . Equity exposure remains significant—often still in the majority—but the glide path has started to shift more meaningfully toward fixed income. These strategies balance continued growth with the early stages of risk moderation as retirement moves into clearer view .

What This Means for Investors

- Growth is Still a Priority: With nearly two decades until retirement, you cannot afford to be overly conservative. The portfolio needs growth to outpace inflation and fund a potentially long retirement.

- Risk Management is Emerging: The sequence of returns risk—the danger of a major market downturn just before or after retirement—becomes a growing concern. The fund’s gradual shift toward bonds helps mitigate this risk.

- Active vs. Passive Matters More: At this stage, the fund’s construction, fees, and glide path design begin to have a more pronounced impact on outcomes compared to funds with target dates further out.

How We Evaluated the Best 2045 Target-Date Funds

To identify the best target-date funds for 2045 retirement, we evaluated funds based on the following criteria, using the most recent data available as of February 2026:

1. Expense Ratio

Cost is one of the few variables in target-date fund design that investors can assess with certainty . Since TDFs are intended for long holding periods, even small differences in expense ratios can significantly impact compounded returns over time . We prioritized funds with below-average costs.

Is Investing in Cryptocurrency Safe for Beginners?

2. Risk-Adjusted Performance

Raw returns can be misleading because higher returns usually reflect higher risk, not superior fund design . We considered metrics like the Sharpe Ratio, which measures return per unit of risk, and Morningstar risk-adjusted ratings .

3. Glide Path Design

We assessed the fund’s underlying investment philosophy. Does it follow a “through” glide path (continuing to adjust after retirement) or a “to” glide path (settling at retirement)? Is the equity exposure aggressive or moderate? .

4. Fund Company and Management (People & Parent)

A fund’s parent organization and management team are critical. We considered Morningstar’s “People” and “Parent” Pillar ratings, which evaluate the quality of the management team and whether the parent company’s priorities align with investors’ interests .

5. Underlying Investment Philosophy

Is the fund built primarily from low-cost index funds (passive), actively managed funds, or a blend of both? Each approach has implications for cost and potential performance .

How to Choose Your First Mutual Fund

The Best Target-Date Funds for 2045 Retirement

Based on our analysis, the following funds stand out as top contenders for investors targeting a 2045 retirement. They represent a range of investment philosophies, from pure index to active management.

| Fund Name (Ticker) | Expense Ratio | Key Philosophy | Standout Feature |

|---|---|---|---|

| Vanguard Target Retirement 2045 Fund (VTIVX) | 0.08% (estimate) | Pure Index | Ultra-low cost, simplicity, 4-fund portfolio |

| T. Rowe Price Retirement Blend 2045 Fund (TRBQX) | 0.42% | Blend (Active + Index) | High-equity glide path, skilled management, lower cost than pure active |

| Fidelity Freedom 2045 Fund (FFFGX) | 0.75% | Active Management | Massive assets, experienced team, recent strategic updates |

| American Funds 2045 Target Date Retirement Fund (FATTX) | 0.81% (Class F-1) | Active Management | Strong long-term track record, objectives-based framework |

Also Consider: Index Alternatives

- Fidelity Freedom Index 2045 Fund (FIOFX): If you prefer Fidelity but want an index-based approach, this is an excellent low-cost alternative to the actively managed FFFGX. Expense ratios are typically below 0.12%.

- BlackRock LifePath Index 2045 Fund: A dominant player in the 401(k) space, often offered as a Collective Investment Trust (CIT) with very low fees. If this is an option in your plan, it is a top-tier choice .

Detailed Fund Analysis

1. Vanguard Target Retirement 2045 Fund (VTIVX)

The Benchmark for Low-Cost Index Investing

Vanguard’s target-date series is built on a simple, elegant four-fund index structure that provides broad exposure to U.S. and international stocks and bonds . The fund follows a “through” glide path that continues to become more conservative for years after retirement.

- Expense Ratio: Approximately 0.08% , making it one of the cheapest options available. This cost advantage is a powerful predictor of long-term success .

- Performance: As of February 2026, VTIVX has shown strong recent performance, with a 1-year return of +19.11% and a 3-year return of +16.39% , consistently ranking in the top quartiles of its Morningstar category .

- Risk Statistics: The fund demonstrates excellent risk-adjusted performance, with a 3-year Sharpe Ratio of 1.09 relative to its benchmark, indicating strong returns for the level of risk taken . Its high R-squared value (above 98) shows it tracks its benchmark closely, as expected for an index fund .

- Best For: Investors who prioritize rock-bottom costs, simplicity, and a “set-it-and-forget-it” philosophy. It is the standard against which all other target-date funds should be measured.

2. T. Rowe Price Retirement Blend 2045 Fund (TRBQX)

The High-Equity, Lower-Cost Hybrid

T. Rowe Price is known for its research-driven, active management approach. The “Blend” series offers a compelling compromise: it uses the same high-equity glide path as the firm’s flagship Retirement series but combines active and passive underlying funds to lower costs .

- Expense Ratio: 0.42% . This is significantly lower than a fully active fund but higher than a pure index fund .

- Investment Philosophy: The fund maintains a higher allocation to equities throughout the lifecycle than many peers. This reflects the firm’s view that higher growth potential is necessary to address longevity risk and relatively low savings rates .

- Management: Morningstar analysts describe the series’ managers as “skilled” and the firm’s resources as “deep,” making it “one of the strongest target-date options around” .

- Best For: Investors who want the potential upside of active management and a higher equity allocation but appreciate the cost savings of incorporating index funds. It is an excellent choice for those with a higher risk tolerance.

- investment mistakes to avoid in your 20s

3. Fidelity Freedom 2045 Fund (FFFGX)

The Active Heavyweight with Recent Enhancements

Fidelity Freedom is one of the largest and most widely held target-date series in the world. It is an actively managed fund-of-funds, meaning Fidelity’s managers select and combine a portfolio of other Fidelity funds .

- Expense Ratio: 0.74% . This is typical for an actively managed target-date fund .

- Recent Changes: Morningstar notes that the series “recently underwent changes” that keep it “a strong choice for retirement savers” . These updates have refined its investment process and asset allocation.

- Asset Size: With over $24.8 billion in assets, it benefits from massive scale and resources .

- Top Holdings: The fund invests in a wide range of Fidelity’s specialized funds, including Fidelity Series Growth Company, Fidelity Series Emerging Markets Opps, and Fidelity Series International Value, providing broad diversification .

- Best For: Investors who believe in active management and trust Fidelity’s extensive research capabilities. It is a solid choice if available in your 401(k).

4. American Funds 2045 Target Date Retirement Fund (FATTX)

The Long-Term Performer

American Funds is known for its disciplined, long-term, active management approach. Their target-date strategies are built from actively managed funds using an “objectives-based framework” that allocates assets across broad categories .

- Expense Ratio: 0.81% (Class F-1) .

- Long-Term Track Record: The fund has shown remarkable long-term performance, ranking in the 9th percentile in its category over the 15-year period (top 9% of all funds) . Its 10-year return of +12.28% also outpaces the category average .

- Recent Performance: FATTX has had a strong 2026, with a year-to-date return of +2.87% as of early February, well ahead of the S&P 500 and its category average .

- Best For: Investors with a long time horizon who value a proven, active management team with a strong record of delivering for shareholders over decades.

Active vs. Passive: Understanding the Construction

One of the most important distinctions among the best target-date funds for 2045 retirement is whether they are actively managed, passively managed, or a blend .

Passive (Index) Funds

- How They Work: Invest in index funds that track broad market benchmarks (e.g., S&P 500, Total Bond Market).

- Pros: Ultra-low fees, predictable performance relative to the market, no manager risk.

- Cons: Will never outperform the market; strictly matches it.

- Examples: Vanguard Target Retirement, Fidelity Freedom Index, BlackRock LifePath Index .

Active Funds

- How They Work: Fund managers actively select investments to try and outperform the market.

- Pros: Potential for higher returns, ability to adapt to changing market conditions.

- Cons: Higher fees, risk of manager underperformance.

- Examples: Fidelity Freedom, American Funds Target-Date .

Blend Funds

- How They Work: Combine actively managed funds for some asset classes with low-cost index funds for others.

- Pros: Lower cost than pure active, retains some potential for active management to add value.

- Cons: More complex than a pure index approach.

- Examples: T. Rowe Price Retirement Blend, Capital Group Target-Date Retirement Blend .

Glide Paths: Not All Funds Are Created Equal

The glide path is the roadmap that determines how your asset allocation changes over time. It is a fundamental aspect of a target-date fund’s design.

snowball vs avalanche method calculator

“To” vs. “Through” Glide Paths

- “To” Glide Paths: The fund’s asset allocation becomes most conservative at the target date and stops changing significantly afterward.

- “Through” Glide Paths: The fund continues to become more conservative for years after the target date, managing risk throughout retirement.

Equity Exposure Varies

Some fund families, like T. Rowe Price, maintain higher equity exposure than average throughout the lifecycle, aiming for higher growth to combat longevity risk . Others, like Vanguard, follow a more moderate path. American Century’s One Choice portfolio describes its approach as “intentionally moderate,” seeking to create a “smoother path” and moderate the potential to lock in a loss in the event of a market downturn near retirement .

Fees: The Certainty in an Uncertain World

When evaluating the best target-date funds for 2045 retirement, cost is the one variable you can control with certainty .

The Impact of Fees

A 1% higher fee might not seem like much, but over 20 years, it can consume a significant portion of your potential returns. For example, on a $100,000 portfolio growing at 6% annually, a 1% fee costs you over $40,000 in lost growth over 20 years.

how to negotiate lower credit card interest rates

What to Look For

- Index Funds: Aim for expense ratios under 0.15% .

- Blend Funds: Expense ratios between 0.30% and 0.50% are reasonable.

- Active Funds: Expense ratios up to 0.75% – 0.90% are typical, but you should expect strong management and potential outperformance to justify the higher cost .

Where to Access These Funds

Employer-Sponsored Plans (401(k), 403(b))

This is where most investors encounter target-date funds. Your plan will have a specific lineup of funds, which may include Vanguard, Fidelity, T. Rowe Price, or BlackRock options . If your plan offers a low-cost index series (like Vanguard or BlackRock LifePath Index), that is an excellent choice. If only actively managed versions are offered, evaluate them based on the criteria above.

IRAs and Brokerage Accounts

You can purchase any of the mutual funds discussed in this article directly through a brokerage account at firms like Vanguard, Fidelity, Schwab, or others . Be mindful of any transaction fees or minimum investment requirements, which can range from $1,000 to $2,500 for some funds .

Collective Investment Trusts (CITs)

These are often found in 401(k) plans. They are similar to mutual funds but typically have even lower fees. They are not available in retail IRAs. The Vanguard Target Retirement CITs, for example, are a low-cost option within many plans .

best debt consolidation loans for good credit 2024

Frequently Asked Questions

Q1: What is the best target-date fund for 2045 overall?

There is no single “best” fund, as it depends on your personal preferences. However, the Vanguard Target Retirement 2045 Fund (VTIVX) is the standard-bearer for low-cost index investing. For those seeking active management with a higher equity allocation, the T. Rowe Price Retirement Blend 2045 Fund (TRBQX) is a top-tier choice that balances cost and active potential .

Q2: What is the average expense ratio for a 2045 target-date fund?

Expense ratios vary widely. Index-based funds can be as low as 0.08% . Actively managed funds typically range from 0.50% to 0.90% . The funds in our analysis range from approximately 0.08% to 0.89% .

Q3: Should I choose an active or passive target-date fund?

If you prioritize the lowest possible cost and a guarantee of matching market returns, choose a passive (index) fund. If you believe skilled active managers can outperform the market over time and are willing to pay higher fees for that potential, choose an active fund .

Q4: What happens to my 2045 target-date fund after 2045?

Most funds continue to manage your money. They typically transition to a more conservative “retirement income” or “distribution” phase, with a stable asset allocation designed to provide income and preserve capital for the remainder of your life .

Q5: Can I lose money in a target-date fund?

Yes. Target-date funds are invested in the stock and bond markets, which fluctuate in value. The principal value of the funds is not guaranteed at any time, including after the target date . However, the fund’s design aims to reduce risk as you approach retirement.

how to get out of payday loan debt fast

Q6: Are the best target-date funds the same in every 401(k) plan?

No. Your 401(k) plan will offer a specific, limited menu of funds. The “best” fund for you is often the best option available in your plan. You may need to evaluate the choices provided using the criteria in this guide.

Q7: What is the difference between Fidelity Freedom and Fidelity Freedom Index?

Fidelity Freedom Index funds are passively managed, investing in low-cost index funds. Fidelity Freedom funds are actively managed, investing in a selection of other actively managed Fidelity funds . The Index series has a much lower expense ratio.

Q8: How often should I review my target-date fund choice?

While the fund is designed to be a “set it and forget it” solution, it is wise to review your choice annually or after major life changes. Ensure the fund’s glide path and risk level still align with your overall retirement plan.

Q9: What is a good 10-year return for a 2045 target-date fund?

As of early 2026, leading 2045 funds like VTIVX and FATTX have delivered 10-year annualized returns in the range of 11% to 12% . Past performance is not a guarantee of future results.

Q10: I’m retiring in 2045. Should I be 100% in stocks?

Generally, no. While you still have time to grow your portfolio, a 2045 target-date fund will typically have a significant but not 100% allocation to stocks, with a growing allocation to bonds to manage risk . A 100% stock portfolio would be very risky this close to retirement.

does debt settlement hurt your credit score?

Conclusion

Choosing the best target-date funds for 2045 retirement is a decision that balances cost, risk, and investment philosophy. The leading contenders—Vanguard, T. Rowe Price, Fidelity, and American Funds—each offer distinct approaches, from ultra-low-cost indexing to actively managed strategies with the potential for outperformance.

For most investors, the simplicity and cost-effectiveness of a fund like Vanguard Target Retirement 2045 (VTIVX) are hard to beat. For those with a higher risk tolerance and a belief in active management, the T. Rowe Price Retirement Blend 2045 (TRBQX) offers a compelling, research-driven alternative.

Whichever fund you choose, the most important step is to start saving consistently and let the power of compounding and professional asset allocation work for you. With nearly two decades until your target retirement date, time is your greatest ally.