By Peyman Daneshgar

High-interest debt is one of the most significant obstacles to building wealth in the modern world. With the average credit card annual percentage rate (APR) hovering near historic highs—often exceeding 22% to 24% —carrying a balance can feel like running on a financial treadmill . You make payments, but a large portion is eaten up by interest, leaving the principal balance barely touched.

However, a common misconception is that your interest rate is set in stone. The truth is far more empowering: you can negotiate lower credit card interest rates. In fact, recent data suggests that a vast majority of people who ask for a lower rate are successful. A LendingTree survey found that 83% of cardholders who asked for a lower APR in the past year got one .

This comprehensive guide is designed to be the only resource you will ever need on this topic. We will walk you through the exact strategies, scripts, and psychological tactics required to successfully negotiate lower credit card interest rates, regardless of whether you have perfect credit or are facing financial hardship. By implementing these steps, you can save thousands of dollars, pay off debt faster, and regain control of your financial future.

Table of Contents

- Why Negotiating Your Credit Card APR is a Financial Game-Changer

- Preparation: The Foundation of Success in Negotiating Lower Credit Card Interest Rates

- Step-by-Step Guide: How to Negotiate Lower Credit Card Interest Rates

- Advanced Negotiation Tactics

- What If They Say No? Alternative Strategies to Lower Your Rate

- Long-Term Strategies: Keeping Your Rates Low

- Frequently Asked Questions (FAQs)

- Conclusion: Take Action Today to Secure a Lower Rate

Why Negotiating Your Credit Card APR is a Financial Game-Changer

Before we dive into the “how,” it is vital to understand the “why.” Negotiating lower credit card interest rates isn’t just about saving a few dollars a month; it has a compounding positive effect on your entire financial life.

When you secure a lower APR, more of your monthly payment goes toward paying down the principal—the actual money you borrowed—rather than just covering the interest charges. This creates a virtuous cycle: you pay down the balance faster, which lowers your credit utilization ratio (a key factor in your credit score), which in turn makes you an even more attractive candidate for lower rates in the future.

Consider this example:

Imagine you have a $6,000 balance on a credit card.

- At a 23% APR: If you make the minimum payment (approx. 3% of the balance), it will take you nearly 20 years to pay off the debt, and you will pay over $10,000 in total interest .

- If you negotiate lower credit card interest rates to 16%: You could cut years off your repayment timeline and save thousands of dollars in interest charges.

This is not just about debt; it is about wealth preservation. Every dollar saved on interest is a dollar that can be invested, saved for a home, or used for experiences that enrich your life.

how to open a brokerage account for the first time

Preparation: The Foundation of Success in Negotiating Lower Credit Card Interest Rates

Walking into a negotiation unprepared is the fastest way to get a “no.” Credit card companies are data-driven; you need to counter their data with your own. Preparation is the single most important factor in determining whether you will successfully negotiate lower credit card interest rates .

Know Your Numbers and Your Credit Score

You must know your current APR. This is found on your monthly statement. Also, know your current credit score. If your score has improved since you first opened the card, you have a strong case. If you have a FICO score of 700 or above, you are in a prime position to negotiate . You can check your score for free through services like Experian, WalletHub, or your bank’s app.

The Power of Competitive Offers

This is your strongest weapon. Spend 15 minutes browsing websites like WalletHub, NerdWallet, or Bankrate. Look for credit cards that offer lower APRs than your current rate. It doesn’t matter if you actually want to switch cards; having these offers ready gives you leverage. You are essentially telling your current bank, “I have options.”

Identifying Your Leverage

Before you call, write down your leverage points:

- Loyalty: “I have been a customer for X years.”

- Payment History: “I have never missed a payment.”

- Improved Creditworthiness: “My credit score has increased by 50 points since I opened this account.”

- Market Competition: “I have pre-approved offers for cards with APRs under 18%.”

- ETF vs index fund: which is better for a beginner?

Step-by-Step Guide: How to Negotiate Lower Credit Card Interest Rates

Armed with your research, it is time to make the call. Remember, the goal is to be polite, professional, and persistent.

Step 1: Prioritize Which Card to Call First

If you have multiple cards, start with the one you have held the longest, especially if you have a strong payment history with them. Loyalty matters to issuers, and they are more likely to reward a long-term customer . Alternatively, you might prioritize the card with the highest interest rate to maximize your savings.

Step 2: Dialing the Number and Getting to the Right Person

Call the customer service number on the back of your credit card. When the automated system asks why you are calling, simply say “Retention” or “Cancel account.” This will often route you directly to the retention department or a customer loyalty specialist. These individuals have more authority to negotiate lower credit card interest rates than the first-line customer service representative .

Step 3: The Script – What to Say to Negotiate Lower Credit Card Interest Rates

Here is a powerful, fill-in-the-blanks script you can use. Speak calmly and confidently.

You: “Hello, I hope you’re having a good day. I’ve been a loyal customer of [Bank Name] for [Number] years, specifically with this card ending in [Last 4 digits]. I’m calling today because I’m reviewing my finances and looking at ways to manage my accounts more effectively.”

Them: “Okay, how can I help?”

You: “I’ve noticed my current purchase APR is [Current Rate]%. I’ve recently checked my credit score, and it has improved to [Your Score]. Additionally, I’ve been receiving mail offers for other credit cards with promotional rates as low as [X]%. I really value my relationship with [Bank Name] and would prefer to keep my business here. Is it possible for you to review my account and see if you can negotiate lower credit card interest rates for me to match those competitive offers?”

The Pause: Stop talking. Let them review the account. Silence is a powerful negotiation tool.

Step 4: Handling Objections and the “HUCA” Method

If the representative says they cannot lower your rate, don’t get discouraged. Here is how to handle it:

- The Objection: “I’m sorry, but we don’t have any offers available for your account right now.”

- Your Response: “I understand. Is there a specific department, like the retention department, that handles these requests? Perhaps they have more flexibility. Alternatively, could we discuss a temporary hardship program or a lower fee structure?”

If they still say no, thank them politely and hang up. Then, use the “HUCA” (Hang Up, Call Again) method . Call back an hour later or the next day. You will likely get a different representative, and that person might be having a better day or have more authority to negotiate lower credit card interest rates.

best robo-advisors for beginners 2024 comparison

Advanced Negotiation Tactics

If the basic script doesn’t work, it’s time to deploy more advanced psychological tactics.

Leveraging Financial Hardship

If you are genuinely struggling due to job loss, medical bills, or a family emergency, honesty is the best policy. Banks would rather work with you than see you default.

Script: “Due to [specific hardship], my financial situation has changed. I am committed to paying off my debt, but at my current APR, it’s becoming very difficult to keep up. Are there any hardship programs or reduced-rate options available that could help me stay on track?” .

The Balance Transfer Leverage Play

This is a more assertive version of the first script. It works best if you have a specific offer in hand.

Script: “I’m considering a balance transfer offer from [Competitor Name] that gives me 0% APR for 18 months. I’d rather not go through the hassle of opening a new account and transferring my balance. Before I do that, I wanted to give you the opportunity to offer me a competitive rate so I can keep this account with you.” This explicitly frames the request as a way for them to keep your business .

Asking for a Supervisor

If the representative is unhelpful, politely ask to escalate.

Script: “I appreciate your time. Is it possible for me to speak with a supervisor or someone in the retention department who might have a bit more flexibility to help a long-term customer?”

how to start investing with $100 or less

What If They Say No? Alternative Strategies to Lower Your Rate

Sometimes, despite your best efforts, the issuer won’t budge. If you cannot negotiate lower credit card interest rates with your current provider, it is time to take your business elsewhere.

Balance Transfer Credit Cards

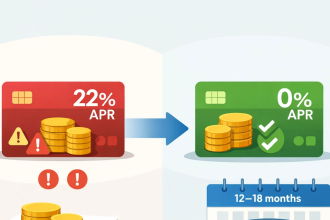

This is one of the most effective alternatives. These cards offer a 0% introductory APR for a period of 12 to 21 months .

- How it works: You apply for the new card and transfer your existing balance.

- The Catch: There is usually a balance transfer fee (3% to 5% of the amount transferred). You must also have a plan to pay off the debt before the 0% period ends; otherwise, the standard APR (which could be high) kicks in .

- Best For: People with good to excellent credit (scores above 670) who can pay off their debt within the promotional window.

Debt Consolidation Loans

A personal loan from a bank, credit union, or online lender can be used to pay off your credit cards.

- How it works: You get a fixed interest rate (often much lower than credit card rates) and a fixed monthly payment over a set term (e.g., 3 years).

- Pros: Simplifies multiple payments into one and has a definite end date.

- Cons: Requires a good credit score for the best rates and turns revolving debt into an installment loan .

Nonprofit Credit Counseling and Debt Management Plans (DMPs)

If your credit isn’t great or you need more structured help, contact a nonprofit credit counseling agency (like InCharge Debt Solutions or Money Management International).

- How it works: A certified counselor will work with your credit card companies to negotiate lower credit card interest rates on your behalf, often securing APRs as low as 8% to 9% .

- Pros: Professional negotiation, single monthly payment, and you become debt-free in 3-5 years.

- Cons: You must close your credit card accounts (which can temporarily dip your score), and there is a small monthly fee .

- best stocks for dividend income for beginners

Long-Term Strategies: Keeping Your Rates Low

Successfully negotiating a lower rate is a great achievement, but maintaining it requires discipline.

- Pay On Time, Every Time: Your payment history is the most significant factor in your credit score. Set up autopay for at least the minimum amount to ensure you never miss a payment .

- Keep Utilization Low: Try to keep your credit utilization ratio (the amount you owe divided by your credit limit) under 30%. The lower, the better .

- Review Statements Monthly: Check your statements to ensure your negotiated rate is being applied and that no new fees have been added.

- Re-Negotiate Annually: Don’t assume the rate is permanent. As your credit score improves or as market rates change, make it a habit to revisit negotiations every 12 to 18 months .

- how to invest in S&P 500 from Europe (or UK, Germany, etc.)

Frequently Asked Questions (FAQs)

1. Will asking for a lower rate hurt my credit score?

No. Simply asking your current issuer to negotiate lower credit card interest rates results in a soft inquiry, which does not affect your credit score. However, if you apply for a new balance transfer card or consolidation loan, that will result in a hard inquiry, which might temporarily ding your score by a few points .

2. What is a “good” credit card interest rate?

A “good” rate depends on the market. As of late 2025, the average APR is over 22%. Therefore, anything below the national average is considered decent. For those with excellent credit (740+), rates can be as low as 14% to 17%. The best rate, of course, is 0%—which you can achieve by paying your balance in full every month .

3. How often can I ask for a rate reduction?

There is no official limit. You can ask as often as your financial situation improves or whenever you see better offers in the market. A good rule of thumb is to check once a year or after a significant positive event, like paying off another debt or getting a raise .

4. What is the “HUCA” method?

HUCA stands for “Hang Up, Call Again.” If you get a “no” from a representative, politely end the call and call back later. Different representatives have different levels of authority and willingness to help. It is a legitimate and effective tactic when you want to negotiate lower credit card interest rates .

5. Can I negotiate rates on cards with a zero balance?

Yes, you can. Even if you don’t carry a balance, a lower rate can be beneficial if you ever need to carry a balance in the future. However, your leverage might be slightly less because the bank isn’t currently making interest income from you.

6. What’s the difference between a rate reduction and a hardship program?

A rate reduction is often a permanent change to your APR based on your improved creditworthiness. A hardship program is a temporary measure (usually 6-12 months) offered to customers experiencing financial difficulty, which lowers payments and rates but may come with restrictions, like having your card frozen for new purchases .

7. Should I threaten to cancel my card?

This can be effective, but use it carefully. Threatening to cancel might prompt a retention offer. However, if the bank calls your bluff and you actually cancel the card, it could hurt your credit score by reducing your total available credit and shortening your credit history. Only use this threat if you are truly willing to follow through .

8. Are credit card companies willing to negotiate with people who have bad credit?

It is more difficult, but not impossible. If your credit score has dropped, the bank may see you as a higher risk. In this case, your best angle is a hardship program. Explain why you are struggling and that a lower rate is the only way you can ensure continued payments. This is often more successful than a standard rate reduction request .

9. How long does a rate negotiation take?

The phone call itself usually takes between 10 and 20 minutes. If the agent has the authority, the change can be applied instantly and will appear on your next billing statement .

10. What if I can’t get a lower rate and don’t qualify for a balance transfer card?

If you are in this situation, it is crucial to seek professional help. Contact a nonprofit credit counseling agency. They can enroll you in a Debt Management Plan (DMP), where they use their industry relationships to negotiate lower credit card interest rates and fees on your behalf, often resulting in significant savings .

Is Investing in Cryptocurrency Safe for Beginners?

Conclusion: Take Action Today to Secure a Lower Rate

The power to change your financial future is literally in your hands—and it starts with a single phone call. The process of learning how to negotiate lower credit card interest rates is not complicated, but it requires preparation, confidence, and persistence. The statistics are on your side; millions of Americans successfully lower their rates every year, saving themselves thousands of dollars in the process.

Whether your credit score has improved, you are facing a temporary hardship, or you simply have better offers from competitors, you have legitimate leverage. Use the scripts and strategies in this guide to advocate for yourself. And if your first attempt fails, remember the HUCA method, or explore the powerful alternatives of balance transfers, consolidation loans, or nonprofit credit counseling.

Your money is too hard-earned to give it away to excessive interest. Don’t wait for a better rate to magically appear. Take control, make the call, and start negotiating today.