Zero-Based Budgeting vs. The 50/30/20 Rule: The Ultimate Financial Strategy Guide for 2026

Author: Peyman Daneshgar

Email: daneshgar781@gmail.com

Publication Date: January 1, 2026

Executive Summary

In the complex world of personal finance, two methodologies have risen to prominence for their effectiveness, clarity, and transformative potential: Zero-Based Budgeting (ZBB) and the 50/30/20 Rule. This comprehensive guide, crafted for discerning readers across America and Europe, will serve as your definitive resource, dissecting every facet of these two powerful budgeting frameworks. Whether you’re a financial novice seeking structure or a seasoned budgeter aiming to optimize, this article will provide unparalleled insights, practical applications, and data-driven analysis to help you determine which system—or hybrid approach—will best serve your financial goals in 2026 and beyond. We will explore the philosophical underpinnings, step-by-step implementation, psychological impacts, and long-term financial outcomes associated with both Zero-Based Budgeting and the 50/30/20 Rule.

Table of Contents

- Introduction: The Quest for Financial Mastery

- Chapter 1: Deep Dive into Zero-Based Budgeting (ZBB)

- Philosophy and Core Principles

- The Step-by-Step ZBB Process

- Pros and Cons: A Clear-Eyed Analysis

- Ideal User Profile: Who Thrives with ZBB?

- Chapter 2: Comprehensive Exploration of the 50/30/20 Rule

- Origin and Foundational Philosophy

- Implementing the 50/30/20 Framework

- Advantages and Limitations

- Ideal User Profile: Who Benefits Most from 50/30/20?

- Chapter 3: Zero-Based Budgeting vs. 50/30/20 Rule: The Head-to-Head Comparison

- Flexibility vs. Structure

- Time Commitment and Complexity

- Effectiveness for Debt Reduction and Wealth Building

- Psychological and Behavioral Impacts

- Chapter 4: Advanced Applications and Hybrid Models for 2026

- Combining ZBB Rigor with 50/30/20 Simplicity

- Adapting Frameworks for High-Income Earners, Freelancers, and Families

- Technology Integration: Best Apps and Tools for Each Method

- Chapter 5: Long-Term Financial Planning: Beyond Monthly Budgeting

- Integrating with Investing, Retirement, and Major Life Goals

- Navigating Economic Uncertainty with Your Chosen System

- Frequently Asked Questions (FAQs)

- Conclusion: Choosing Your Path to Financial Freedom

how to create a budget for beginners step by step

Introduction: The Quest for Financial Mastery

In an era marked by economic volatility, rising costs of living, and an overwhelming array of financial choices, gaining control over one’s personal finances is no longer a luxury—it is a necessity. A budget is the fundamental tool for this control, acting as a blueprint for your financial life. Yet, the very word “budget” can evoke feelings of restriction and complexity. This is where proven frameworks like Zero-Based Budgeting (ZBB) and the 50/30/20 Rule revolutionize the process. They transform budgeting from a punitive exercise into a proactive strategy for empowerment. This article is designed to be the most thorough, actionable, and valuable resource available online, meticulously crafted to answer every possible question a reader might have about Zero-Based Budgeting vs. the 50/30/20 Rule. Our goal is not only to inform but to guide you toward a sustainable and successful financial future.

Chapter 1: Deep Dive into Zero-Based Budgeting (ZBB)

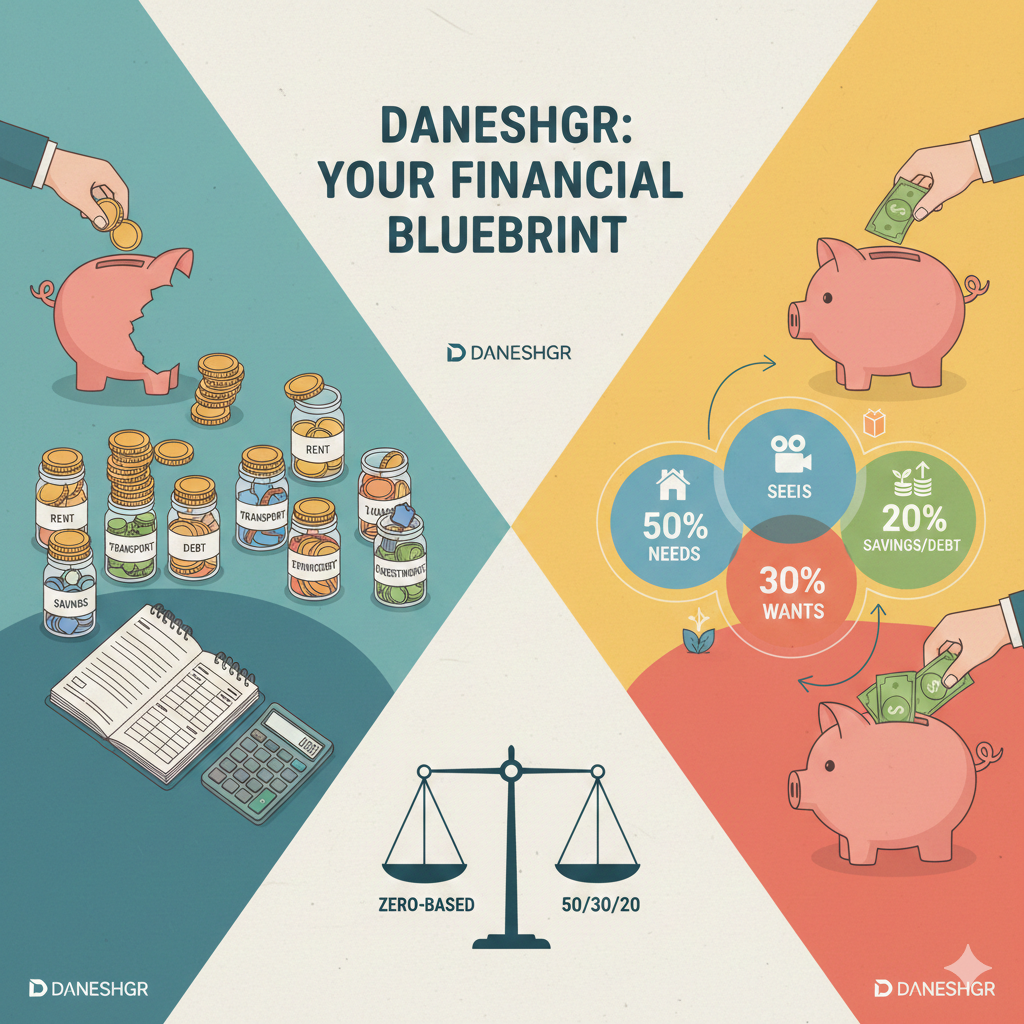

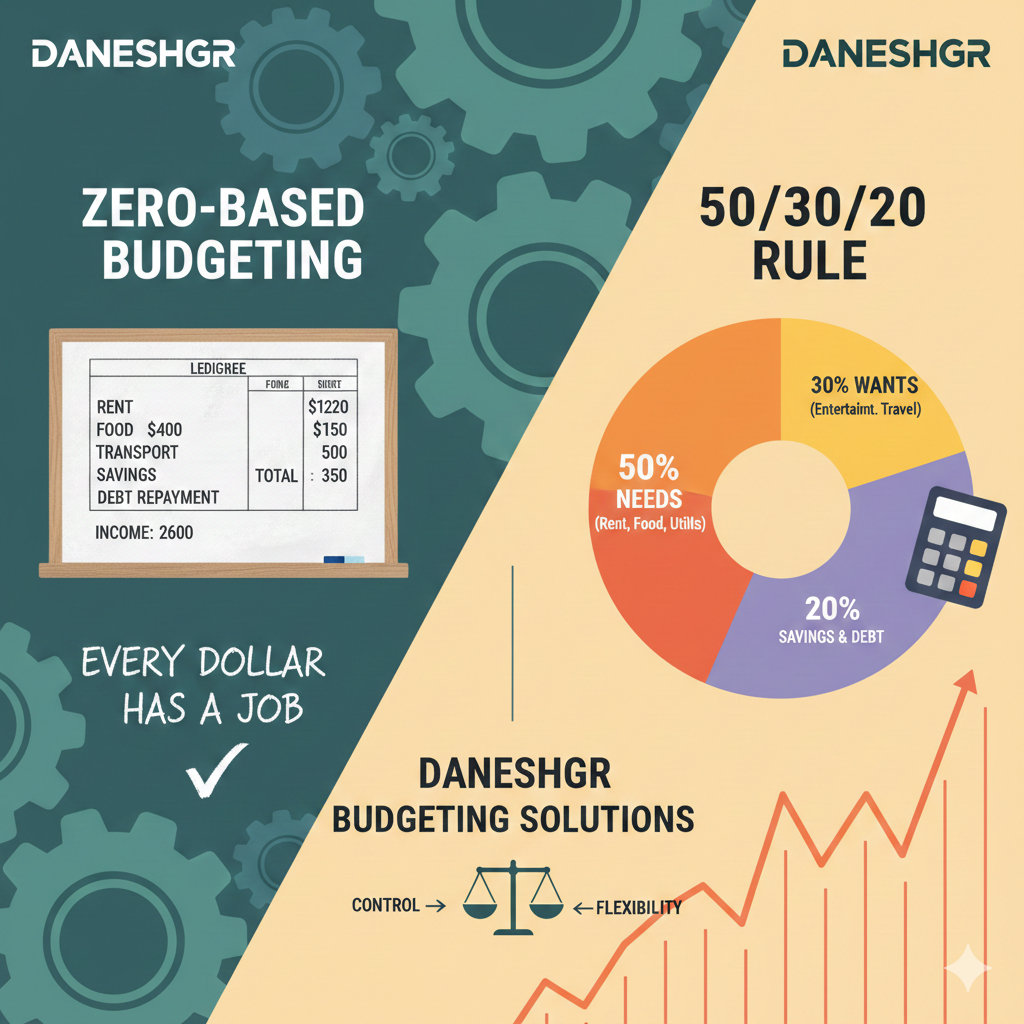

Zero-Based Budgeting (ZBB) is a meticulous, proactive allocation method where your income minus your expenses equals zero. Every dollar is assigned a “job”—whether for bills, groceries, savings, or entertainment—leaving no dollar unaccounted for.

Philosophy and Core Principles:

The philosophy of Zero-Based Budgeting is rooted in intentionality and justification. Unlike traditional budgeting that often adjusts previous budgets, ZBB starts from a “zero base” each period. Every expense must be justified for the new period, promoting efficiency and eliminating wasteful spending. The core principles are:

- Income Assignment: Every unit of income received is allocated to a specific category.

- Justification: All spending categories are analyzed for necessity and optimal cost.

- Proactive Control: You decide the destination of your money before you spend it.

- Alignment with Goals: Spending is directly tied to short- and long-term financial objectives.

The Step-by-Step ZBB Process:

- Identify Monthly Income: Calculate your total take-home pay for the month.

- List All Expenses: Catalog every anticipated expense, from rent and mortgages to subscriptions and coffee.

- Categorize Expenses: Group expenses into categories (e.g., housing, utilities, debt, groceries, savings, giving).

- Assign Every Dollar: Allocate funds to each category until your income minus your planned spending equals zero.

- Track Religiously: Record every transaction throughout the month.

- Adjust as Needed: If you overspend in one category, you must reduce another to maintain the “zero” balance.

- Repeat Monthly: Conduct this process at the start of every budgeting period.

best budgeting method for irregular income

Pros and Cons of Zero-Based Budgeting:

- Pros:

- Maximum Control & Awareness: Provides an intimate understanding of cash flow.

- Eliminates Waste: Uncovers and curbs unnecessary or habitual spending.

- Highly Flexible: Can adapt to irregular incomes or major life changes.

- Accelerates Debt Paydown: Allows for aggressive allocation of surplus funds to debt.

- Cons:

- Time-Intensive: Requires significant setup and ongoing tracking.

- Can Feel Restrictive: The need to justify every expense can be daunting for some.

- Complex for Beginners: The granularity can overwhelm those new to budgeting.

- Requires Discipline: Success is dependent on consistent monthly participation.

Ideal User Profile for Zero-Based Budgeting:

Zero-Based Budgeting excels for individuals or households who: are detail-oriented; have a specific, aggressive financial goal (e.g., debt freedom, saving for a down payment); have a variable or irregular income (e.g., freelancers, commission-based workers); or have tried simpler methods and need more control to stop overspending.

Chapter 2: Comprehensive Exploration of the 50/30/20 Rule

Popularized by Senator Elizabeth Warren in her book All Your Worth, the 50/30/20 Rule is a simplified, ratio-based budgeting framework. It divides your after-tax income into three broad categories, offering a structural guideline rather than a detailed plan.

Origin and Foundational Philosophy:

The 50/30/20 Rule is built on the philosophy of balance and sustainability. It aims to create a healthy equilibrium between necessities, personal desires, and financial future, preventing burnout from overly restrictive budgets. Its strength lies in its simplicity and focus on macro-level allocation.

Implementing the 50/30/20 Framework:

- Calculate After-Tax Income: Determine your monthly take-home pay.

- Apply the Ratios:

- 50% to Needs: Essentials you must pay for survival (housing, utilities, groceries, minimum debt payments, basic transportation, insurance).

- 30% to Wants: Non-essential lifestyle choices (dining out, entertainment, hobbies, travel, subscription services).

- 20% to Savings & Debt Repayment: Future financial health (emergency fund, retirement accounts, investments, and debt repayment beyond the minimum).

- Adjust Spending: Ensure your actual spending aligns within these percentage brackets.

50/30/20 rule calculator excel template free

Advantages and Limitations of the 50/30/20 Rule:

- Advantages:

- Extremely Simple to Start: Low barrier to entry for budgeting novices.

- Provides Healthy Guidelines: Encourages a balanced approach to spending and saving.

- Low Maintenance: Requires less daily tracking than ZBB.

- Reduces Decision Fatigue: Eliminates the need to micro-manage countless categories.

- Limitations:

- Can Be Inflexible for High or Low Incomes: Those in high-cost-of-living areas may struggle to keep “Needs” at 50%. Low-income earners may find little room for “Wants.”

- Lacks Granularity: Doesn’t provide insight into specific spending leaks.

- Potential for Misclassification: Individuals may rationalize “Wants” as “Needs.”

- May Not Be Aggressive Enough: For those with substantial debt, 20% may not be sufficient for rapid repayment.

Ideal User Profile for the 50/30/20 Rule:

The 50/30/20 Rule is perfect for individuals or families who: are new to budgeting and need an easy starting point; have a stable, steady income; seek a balanced lifestyle without deep financial analysis; or are already in a reasonably stable financial position without overwhelming debt.

Chapter 3: Zero-Based Budgeting vs. 50/30/20 Rule: The Head-to-Head Comparison

This critical analysis directly pits Zero-Based Budgeting vs. the 50/30/20 Rule across key dimensions to clarify their differences.

1. Flexibility vs. Structure:

- Zero-Based Budgeting (ZBB) offers supreme flexibility. Every month is a blank slate, allowing for complete reallocation based on changing priorities, seasonal expenses, or income fluctuations.

- The 50/30/20 Rule offers rigid structure. The percentages provide a consistent template, which simplifies decision-making but can be hard to adapt to unique financial circumstances.

2. Time Commitment and Complexity:

- ZBB is high-touch and complex. It demands regular, active engagement (often weekly or even daily) with your finances.

- The 50/30/20 Rule is low-touch and simple. Once the percentages are calculated, only periodic check-ins are needed to ensure you’re on track.

how to save money on a tight income

3. Effectiveness for Debt Reduction and Wealth Building:

- ZBB is a powerful tool for aggressive debt elimination. By finding and reallocating every spare dollar, it can accelerate debt payoff timelines dramatically. It’s equally effective for aggressive saving goals.

- The 50/30/20 Rule promotes steady, disciplined savings and debt repayment. It ensures you are always paying down debt and saving, but the pace may be slower unless you consciously allocate part of your “Wants” category.

4. Psychological and Behavioral Impacts:

- ZBB fosters a sense of total control and can be highly motivating for goal-oriented people. However, it can also induce stress or guilt if categories are consistently overspent.

- The 50/30/20 Rule reduces financial anxiety by providing clear, forgiving guardrails. The dedicated 30% for “Wants” prevents feelings of deprivation, promoting long-term adherence.

Chapter 4: Advanced Applications and Hybrid Models for 2026

The most sophisticated financial practitioners often create hybrid systems. Here’s how to blend Zero-Based Budgeting and the 50/30/20 Rule for optimal results.

The Hybrid Approach:

- Use 50/30/20 as Your Macro Framework: Start by allocating your income into the three main buckets: Needs, Wants, Savings/Debt.

- Apply ZBB Within Categories: Especially within the “Wants” and even “Needs” categories, use Zero-Based Budgeting principles to assign specific dollar amounts. For example, within your 30% “Wants,” assign specific amounts to dining, hobbies, and entertainment to zero.

- Prioritize with ZBB, Scale with 50/30/20: Use ZBB’s justification process to prioritize your savings/debt goals (the 20% bucket), then use the 50/30/20 rule to ensure your overall lifestyle remains balanced.

money saving challenges for couples

Adaptations for Specific Situations:

- High-Income Earners: May use a reverse-engineered ZBB, focusing first on savings/investment goals (e.g., 40%), then allocating the remainder.

- Freelancers/Variable Income: Use a Zero-Based Budgeting approach based on a conservative estimate of monthly income. In high-income months, allocate surplus directly to quarterly tax payments, emergency fund, or investments.

- Families: Can use the 50/30/20 Rule as a family budget, then implement ZBB for specific children-related or household project categories.

Technology Integration:

- For Zero-Based Budgeting: Apps like YNAB (You Need A Budget) are built on the ZBB philosophy and are exceptional for real-time tracking and allocation.

- For the 50/30/20 Rule: Apps like Mint or Personal Capital are excellent for automatic categorization and tracking spending against your set percentage targets.

sinking funds: what are they and how to set them up

Chapter 5: Long-Term Financial Planning: Beyond Monthly Budgeting

Both Zero-Based Budgeting and the 50/30/20 Rule are primarily monthly cash-flow tools. True financial mastery requires integrating them into a broader plan.

- Investing: The “20%” in the 50/30/20 rule explicitly includes investing. In ZBB, investing is a non-negotiable category you fund each month. Automate contributions to IRAs, 401(k)s, or brokerage accounts.

- Retirement Planning: Use your budget to ensure you are hitting annual contribution targets. Both systems should feed into a retirement calculator to ensure you’re on track.

- Major Life Goals: Use ZBB to create dedicated sinking funds for goals like a home, education, or sabbatical. The 50/30/20 Rule can be temporarily adjusted (e.g., to 40/30/30) to accelerate saving for a specific goal.

Frequently Asked Questions (FAQs)

Q1: I have a lot of debt. Which is better, Zero-Based Budgeting or the 50/30/20 Rule?

A: For aggressive debt payoff, Zero-Based Budgeting (ZBB) is generally superior. It allows you to scrutinize every expense and allocate the maximum possible amount to debt repayment each month, potentially far exceeding the 20% allocation suggested by the 50/30/20 rule.

Q2: Can I use the 50/30/20 rule if I live in a very expensive city?

A: It can be challenging. You may need to adjust the ratios to reflect reality, perhaps to a 60/20/20 model. The key is to be honest about what is a true “Need.” If your essential costs exceed 50%, you must compensate by reducing your “Wants” percentage to maintain the crucial 20% for savings and debt.

Q3: Is Zero-Based Budgeting too time-consuming for a busy professional?

A: It can be initially, but technology streamlines it. Apps like YNAB connect to your accounts and reduce manual entry. Many find that the 30-60 minutes per week it demands saves them countless hours of financial stress and saves them significant money.

Q4: Which method is better for someone with an irregular income?

A: Zero-Based Budgeting is typically better suited for irregular income. It forces you to allocate dollars you actually have, not projected income. You budget based on your current “cash on hand,” making it inherently adaptable to income fluctuations.

Q5: Can I switch from one method to the other?

A: Absolutely. Many people start with the simple 50/30/20 Rule to build the budgeting habit and then graduate to the more detailed Zero-Based Budgeting for greater control. Others may switch to the 50/30/20 rule after reaching major goals to maintain their finances with less granular effort.

Q6: How do I handle unexpected expenses in each system?

A: In ZBB, you must adjust your allocations immediately—moving money from other categories to cover the expense. In the 50/30/20 Rule, a robust emergency fund (built from the 20% category) should cover true emergencies. For smaller unexpected costs, you would pull from your “Wants” category for that month.

Conclusion: Choosing Your Path to Financial Freedom

The debate between Zero-Based Budgeting vs. the 50/30/20 Rule is not about finding a universal winner, but about identifying the right tool for your personal financial personality, circumstances, and goals.

- Choose Zero-Based Budgeting (ZBB) if you crave total control, have specific aggressive financial targets, don’t mind detailed work, and have a variable income. It is the precision instrument of budgeting.

- Choose the 50/30/20 Rule if you value simplicity and balance, are new to budgeting, have a stable income, and want a sustainable, low-stress framework to guide your overall financial behavior.

For many, the most powerful strategy in 2026 may be a synergistic blend: using the 50/30/20 Rule as a strategic compass to ensure balance, while employing the granular, intentional tactics of Zero-Based Budgeting within its framework to maximize efficiency and goal attainment.

Ultimately, the best budget is the one you will stick with. We encourage you to experiment with both Zero-Based Budgeting and the 50/30/20 Rule. Start with a three-month trial of each. Track not only your financial numbers but also your stress levels and sense of empowerment. The data and feelings you gather will point you decisively toward the system that will serve as your foundation for lasting financial freedom and peace of mind