The Ultimate Guide: Pros and Cons of a 15-Year vs 30-Year Mortgage

By Peiman Daneshgar

Email: daneshgar781@gmail.com

Table of Contents

- Introduction: The Most Important Decision in Home Financing

- Understanding the Basics: What Do These Terms Mean?

- The Core Difference: A Side-by-Side Comparison

- The 15-Year Mortgage: A Deep Dive into the Pros and Cons

- The 30-Year Mortgage: A Deep Dive into the Pros and Cons

- Beyond the US: A Note for European Homebuyers

- The “Rich Person’s” Debate: Pay Off Debt or Invest?

- Alternatives to the Traditional 15- or 30-Year Mortgage

- How to Decide: A Step-by-Step Framework

- Strategies to Get the Best of Both Worlds

- The Impact of 2026 Market Conditions

- Frequently Asked Questions

- Conclusion

Introduction: The Most Important Decision in Home Financing

For most people, a mortgage is the largest financial commitment they will ever make. It is also one of the most complex. Before you even start comparing interest rates from different lenders, you face a fundamental, strategic choice that will shape your budget and your financial future for decades: Should you choose a 15-year or a 30-year mortgage?

This decision is about more than just picking a number. It is a trade-off between monthly cash flow and long-term wealth building, between financial flexibility and the psychological comfort of owning your home outright. In the current economic climate of 2026, with interest rates having stabilized at levels higher than the historic lows of the past decade, understanding the pros and cons of a 15-year vs 30-year mortgage is more critical than ever.

This comprehensive guide will walk you through every nuance of this decision. We will analyze the mathematical differences, explore the strategic implications, and provide a clear framework to help you choose the path that aligns with your unique financial situation and life goals. Whether you are a first-time homebuyer in the United States or navigating the different mortgage landscapes of Europe, this article will answer every question you have about the pros and cons of a 15-year vs 30-year mortgage.

Understanding the Basics: What Do These Terms Mean?

Before diving into the complexities, it is essential to define the two main competitors clearly.

What is a 30-Year Fixed-Rate Mortgage?

A 30-year fixed-rate mortgage is a loan amortized over 360 months. As the name suggests, the interest rate is locked in for the entire duration of the loan, meaning your monthly principal and interest payment remains constant for three decades.

- Prevalence: This is the most popular mortgage product in the United States, accounting for roughly 90% of home purchase mortgages . Its popularity stems from its affordability on a month-to-month basis.

- Mechanics: Because the repayment period is long, the principal is paid down very slowly in the early years. In the first decade of a 30-year loan, the vast majority of your monthly payment goes toward interest, not reducing the actual amount you borrowed.

- How to Choose Your First Mutual Fund

What is a 15-Year Fixed-Rate Mortgage?

A 15-year fixed-rate mortgage is a loan amortized over just 180 months. It offers the same stability of a fixed interest rate but compresses the repayment schedule into half the time.

- Prevalence: Far less common than its 30-year counterpart, 15-year mortgages typically make up less than 10% of new home loans .

- Mechanics: With a 15-year loan, you are forcing yourself to pay off the debt much faster. This results in a significantly higher monthly payment, but it also means you build equity in your home at a much more rapid pace.

The Core Difference: A Side-by-Side Comparison

The choice between these two mortgages boils down to three primary factors: the monthly payment, the interest rate, and the total cost of the loan. To truly understand the pros and cons of a 15-year vs 30-year mortgage, let’s look at a concrete example based on current market data.

How to Choose Your First Mutual Fund

Assume you are taking out a loan of $400,000. Based on averages, a lender might offer you a 6.5% interest rate on a 30-year loan and a 6.0% rate on a 15-year loan .

| Feature | 15-Year Mortgage | 30-Year Mortgage | The Difference |

|---|---|---|---|

| Loan Term | 15 years | 30 years | 15 years shorter |

| Interest Rate | Lower (e.g., 6.0%) | Higher (e.g., 6.5%) | 0.5% lower rate |

| Monthly Payment | Higher (~$3,375) | Lower (~$2,528) | ~$847 more/month |

| Total Interest Paid | ~$207,500 | ~$510,000 | ~$302,500 saved |

| Total Cost of Home | ~$607,500 | ~$910,000 | ~$302,500 cheaper |

Figures are estimates for illustrative purposes.

As the table illustrates, the trade-off is stark. The 30-year mortgage offers immediate relief with a lower monthly payment, making it easier to qualify for the loan and fit into your current budget. However, this convenience comes at a staggering cost: you will pay the bank over $300,000 more in interest over the life of the loan .

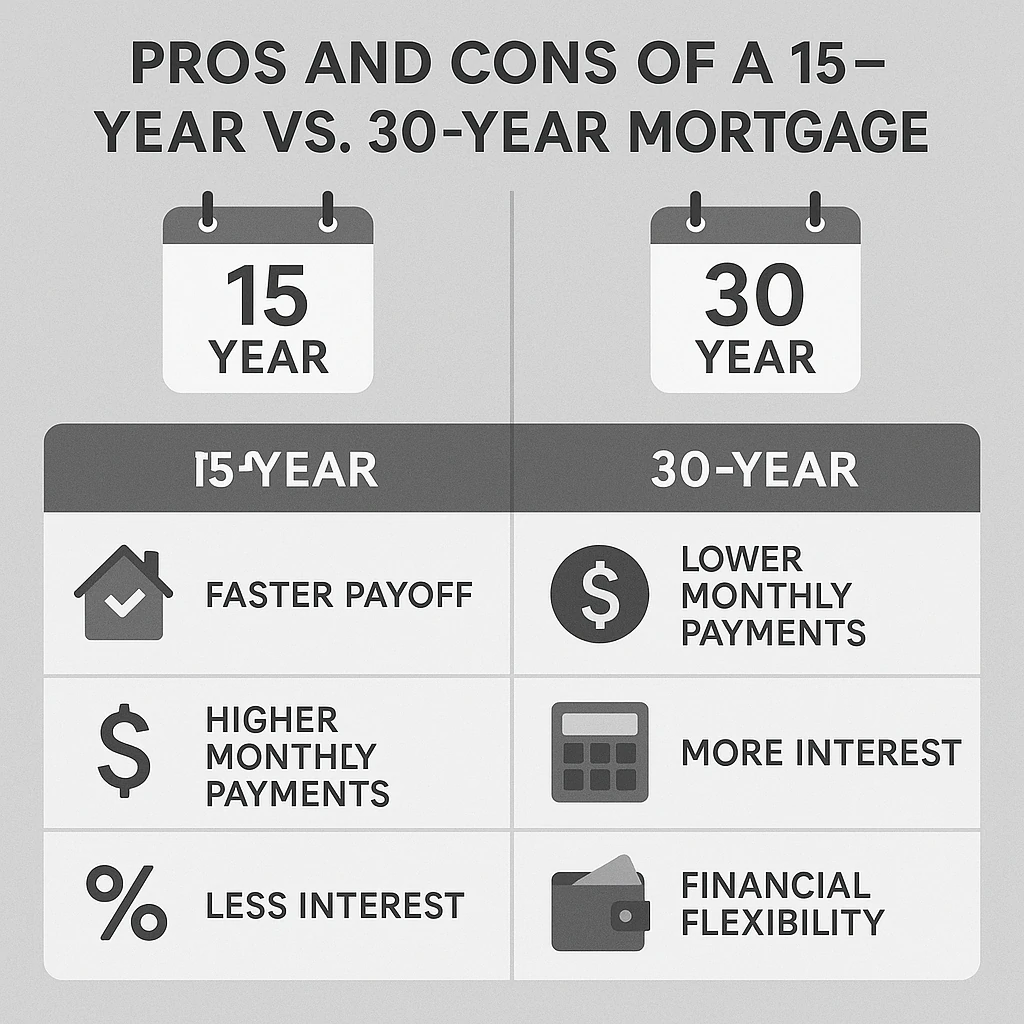

The 15-Year Mortgage: A Deep Dive into the Pros and Cons

The 15-year mortgage is often championed by personal finance purists like Dave Ramsey as the only way to buy a home . But is it right for everyone? Let’s break down the advantages and disadvantages in detail.

Pros of a 15-Year Mortgage

1. Massive Savings on Interest

This is the single most compelling financial argument for a 15-year loan. As demonstrated in the example above, the interest savings can be in the hundreds of thousands of dollars . You save in two ways: first, lenders typically offer a lower interest rate for shorter-term loans because their money is at risk for less time. Second, you are only paying interest for 15 years instead of 30. This combination dramatically reduces the total cost of your home.

Is Investing in Cryptocurrency Safe for Beginners?

2. Build Home Equity at an Accelerated Pace

Equity is the portion of your home you truly own. With a 15-year mortgage, a much larger chunk of your monthly payment goes directly toward the principal from day one. This rapid equity building gives you financial power sooner. You could potentially use that equity to fund a major renovation, start a business, or have a significant asset to tap into during retirement .

3. True Ownership in Half the Time

Imagine being mortgage-free while you are still in your prime earning years or as you enter retirement. Paying off your home by age 50 or 55 frees up a massive amount of monthly cash flow that can be redirected toward travel, hobbies, or retirement savings. For those approaching retirement, having a paid-off home is a massive relief, significantly reducing monthly expenses on a fixed income .

4. A Disciplined, Forced Savings Plan

A 15-year mortgage acts as a powerful form of forced savings. The higher monthly payment is non-negotiable, compelling you to build wealth with every check you write. For individuals who might otherwise struggle to invest the difference, this structure guarantees that a significant portion of their income is going toward their net worth .

Cons of a 15-Year Mortgage

1. Significantly Higher Monthly Payments

This is the biggest barrier. In our $400,000 loan example, the monthly payment is nearly $850 higher. This can lead to being “house rich, but cash poor,” leaving little room in your budget for other important goals like investing, saving for your children’s education, or even just enjoying life .

how to invest in S&P 500 from Europe (or UK, Germany, etc.)

2. Reduced Financial Flexibility

Tying up so much of your monthly income in your home can be risky. If you lose your job or face a medical emergency, the inflexible, high payment can become a severe burden. You have less cash on hand to deal with unexpected expenses .

3. You Can’t Borrow as Much

Lenders qualify you based on your debt-to-income (DTI) ratio. Because the monthly payment on a 15-year loan is so much higher, it consumes a larger portion of your gross monthly income. This lowers the maximum loan amount you qualify for, potentially pricing you out of the home you want or forcing you to buy a less expensive property .

4. Higher Opportunity Cost

This is a critical point for wealth-building. The extra money you are throwing at your mortgage each month is money that cannot be invested in the stock market. Historically, the stock market has delivered average annual returns of 7-10%. If your mortgage rate is 6%, you might be financially better off investing the extra cash and earning an 8% return, even after paying the mortgage interest .

The 30-Year Mortgage: A Deep Dive into the Pros and Cons

The 30-year mortgage is the bedrock of the American housing market. Its resilience and popularity stem from the flexibility and breathing room it offers.

Pros of a 30-Year Mortgage

1. Lower, More Manageable Monthly Payments

The primary advantage is affordability. The lower payment makes homeownership accessible to millions of people who could not afford the high payments of a 15-year loan. It fits more comfortably into a monthly budget, allowing you to cover other living expenses without stretching yourself too thin .

2. Superior Cash Flow and Liquidity

By keeping your housing costs lower, you free up cash to pursue other financial opportunities. You can contribute more to your 401(k) or IRA, build a robust emergency fund, save for a child’s college tuition, or invest in other assets. This liquidity provides a safety net that a high mortgage payment can erode .

3. Increased Borrowing Power

Because the monthly payment is lower, your debt-to-income ratio looks much healthier to lenders. This allows you to qualify for a larger loan amount, which can be crucial in expensive real estate markets where home prices are high .

4. The “Optionality” of Prepayment

A 30-year mortgage gives you control. You have the option to make extra principal payments when you have the cash, effectively turning it into a 15-year loan on your own schedule. However, if you hit a rough patch financially, you can simply pay the lower required amount without penalty. This flexibility is something a 15-year mortgage simply does not offer .

best stocks for dividend income for beginners

Cons of a 30-Year Mortgage

1. Enormous Interest Costs

This is the major drawback. You are paying interest for twice as long, often at a higher rate. Over the life of the loan, you will pay a staggering amount in interest—often more than the original purchase price of the home itself . Some financial critics call this the “30-year trap,” where you end up paying for the bank’s second house while living in your first .

2. Painfully Slow Equity Growth

In the early years of a 30-year mortgage, your payments are almost entirely interest. It can take over a decade to build any significant equity. This means if you need to sell the home after a few years, you might barely break even after realtor commissions and closing costs .

3. Psychological Burden of Long-Term Debt

For some, carrying a large debt for three decades is a source of stress. The idea of making mortgage payments well into one’s 60s can be daunting and runs counter to the goal of a debt-free retirement for many people .

Beyond the US: A Note for European Homebuyers

While this guide focuses on the pros and cons of a 15-year vs 30-year mortgage, it is important to note that the mortgage market in Europe can be quite different.

- Fixed-Rate Terms are Shorter: In many European countries (like the UK, France, and Germany), the most common fixed-rate mortgage terms are 2, 5, or 10 years, rather than 15 or 30 . After this initial “fixed period,” the loan typically reverts to a variable rate, or you must renegotiate a new rate with your lender. True 30-year fixed-rate mortgages are less common outside the US.

- Variable and SARON Mortgages: Products like variable-rate mortgages or those tied to benchmarks like SARON (Swiss Average Rate Overnight) are popular. These offer lower initial rates but expose you to interest rate fluctuations .

- The 25-Year Standard: In the UK, for example, a 25-year mortgage term is a very common standard, representing a middle ground between the US 15- and 30-year options .

- Portability: In many European countries, mortgages are often “portable,” meaning you can transfer them to a new property if you move, avoiding hefty early repayment charges.

- how to start investing with $100 or less

For European readers, the principles in this article apply to the total amortization period of the loan. The pros and cons of a 15-year vs 30-year mortgage regarding interest costs and cash flow remain valid, even if your initial fixed-rate period is much shorter. You must also carefully consider the risk of rising interest rates when your initial fixed term ends .

The “Rich Person’s” Debate: Pay Off Debt or Invest?

This is perhaps the most nuanced aspect of the pros and cons of a 15-year vs 30-year mortgage. It boils down to a simple question: what should you do with your extra cash?

The mathematical answer is based on a comparison:

- Guaranteed Return: Paying off a 6% mortgage gives you a guaranteed, risk-free return of 6%. Every dollar you prepay saves you from paying 6% interest in the future .

- Expected Return: Investing in a diversified portfolio (like an S&P 500 index fund) has an historical average return of around 7-10%, but this is not guaranteed.

If your mortgage rate is low (e.g., 3-4%), the math strongly favors investing. The potential returns from the market are almost certainly going to be higher than the cost of your debt.

However, in the 2026 rate environment (with mortgages in the 6-7% range) , the math is much closer. A guaranteed 6.5% return by paying down debt is very attractive compared to a risky 8% return from the market . The decision then becomes about your personal risk tolerance. Do you want the certainty of a paid-off home, or are you willing to accept market volatility for a chance at higher long-term wealth?

best robo-advisors for beginners 2024 comparison

Alternatives to the Traditional 15- or 30-Year Mortgage

The 15- and 30-year loans aren’t your only options. Here are a few alternatives to consider.

- 20-Year Mortgage: A happy medium. You get a faster payoff than a 30-year and lower payments than a 15-year, with moderate interest savings.

- 10-Year Mortgage: An aggressive strategy for those who want to own their home outright as soon as possible and can handle a very high monthly payment .

- 40-Year Mortgage: Rare, and usually a bad idea. The lower monthly payments are offset by an astronomical total interest cost .

- Adjustable-Rate Mortgage (ARM): These offer a low fixed rate for an initial period (e.g., 5, 7, or 10 years) and then adjust periodically. They can be a good option if you are certain you will move or refinance before the fixed period ends .

- ETF vs index fund: which is better for a beginner?

How to Decide: A Step-by-Step Framework

Choosing between the pros and cons of a 15-year vs 30-year mortgage requires a personal, data-driven approach. Use this framework to guide your decision.

Step 1: Run the Numbers

Use an online mortgage calculator to compare the exact monthly payments and total interest for both terms based on current rates for your desired loan amount. The numbers don’t lie .

Step 2: Assess Your Budget with the 28/36 Rule

A common rule of thumb is that your total monthly housing costs (principal, interest, taxes, insurance) should not exceed 28% of your gross monthly income. Furthermore, your total monthly debt payments (including the mortgage, car loans, student loans, and credit cards) should not exceed 36% of your gross income . Can you meet these thresholds with the 15-year payment?

Step 3: Evaluate Your Job Security and Income Stability

If your income is commission-based, seasonal, or variable, the flexibility of a 30-year loan is invaluable. A 15-year loan is best suited for those with very stable, predictable, and secure employment .

Step 4: Consider Your Life Stage and Retirement Goals

If you are in your 50s, a 30-year mortgage would stretch into your 80s, which is not ideal . A 15-year mortgage aligns better with a traditional retirement timeline. If you are in your 20s or 30s, you have more time to leverage a 30-year mortgage for flexibility and investment.

Step 5: Be Honest About Your Financial Discipline

This is the behavioral finance question. Are you disciplined enough to invest the difference every single month? Or will that extra cash simply get spent? If you lack the discipline to invest, the forced savings of a 15-year mortgage is a powerful tool .

how to open a brokerage account for the first time

Strategies to Get the Best of Both Worlds

You do not have to make a binary choice. Here are strategies to combine the flexibility of the 30-year loan with the wealth-building benefits of the 15-year loan.

1. The “Borrow 30, Pay 15” Strategy

Take out a 30-year mortgage for its lower required payment and easier qualification. Then, set up an automatic payment as if it were a 15-year loan. This gives you the flexibility to drop back down to the 30-year payment if you ever face a financial hardship. As long as you stick to the higher payment, you will pay off your home in 15 years and save a fortune in interest .

2. The Bi-Weekly Payment Plan

Instead of one monthly payment, pay half your monthly payment every two weeks. Because there are 52 weeks in a year, this results in 26 half-payments, which equals 13 full monthly payments. This extra payment each year goes directly to your principal, shaving years off a 30-year loan and saving you thousands in interest .

3. Make One Extra Lump-Sum Payment Per Year

If bi-weekly payments are too complicated, simply commit to making one extra mortgage payment each year, perhaps with your tax refund or work bonus. Mark it clearly for “principal reduction.”

4. Refinance Later

You can start with a manageable 30-year mortgage now. Then, in 5-10 years, if your income has increased significantly and interest rates are favorable, you can refinance into a 15-year loan to finish paying it off .

The Impact of 2026 Market Conditions

As of 2026, the decision matrix has shifted. With mortgage rates hovering in the 6-7% range, the “guaranteed return” of paying down debt is much more compelling than it was when rates were at 3% . The era of “free money” is over.

Furthermore, high home prices mean that the monthly payment on a 15-year mortgage is out of reach for many first-time buyers. In this environment, the 30-year mortgage is often the only viable path to homeownership, allowing people to enter the market and start building equity rather than waiting on the sidelines . The key is to enter with a plan to eventually pay it off faster.

Frequently Asked Questions

Q1: Is a 15-year mortgage always better than a 30-year mortgage?

No. While a 15-year mortgage saves you a tremendous amount in interest, it is not “better” if the high monthly payments leave you financially vulnerable. The “best” mortgage is the one you can afford comfortably while still meeting your other financial goals .

Q2: Can I pay off a 30-year mortgage in 15 years?

Absolutely. This is one of the best strategies. As long as your loan has no prepayment penalty (most don’t), you can make extra principal payments to pay it off on a 15-year timeline. This gives you the flexibility of a lower required payment .

Q3: Why do most people choose a 30-year mortgage?

Most people choose a 30-year mortgage because it offers the lowest possible monthly payment, making homeownership affordable for the average family. It provides more breathing room in the monthly budget .

Q4: What is the main drawback of a 30-year loan?

The main drawback is the enormous amount of interest you pay over the life of the loan. You will likely pay more in interest than the original purchase price of the home .

Q5: How do I qualify for a 15-year mortgage?

Qualifying for a 15-year mortgage is harder. You will need a higher income and a lower debt-to-income ratio because the monthly payment is so much larger. Lenders want to see that you can comfortably afford that higher payment .

Q6: Is the mortgage interest tax deduction a good reason to get a 30-year loan?

For most people, no. Since the Tax Cuts and Jobs Act, the standard deduction has been so high that very few homeowners benefit from itemizing their mortgage interest. The tax savings are usually far less than the extra interest you pay .

what is dollar-cost averaging and how to set it up

Q7: What happens if I can’t make the payments on a 15-year mortgage?

If you cannot make your payments, you risk foreclosure, just as you would with any mortgage. This is the primary risk of choosing a payment that is too high for your budget .

Q8: Are these mortgage terms available in Europe?

Fixed-rate mortgages for the full 15- or 30-year amortization period are less common. In many European countries, you might have a 25- or 30-year amortization schedule, but the interest rate is only fixed for the first 2-10 years, after which it becomes variable or is renegotiated .

Q9: Should I refinance my 30-year mortgage to a 15-year mortgage?

Refinancing to a 15-year term can be a great move if interest rates are lower than your current rate and you can comfortably afford the higher payment. It allows you to lock in savings and pay off your home faster.

Q10: Which mortgage term is better for first-time homebuyers?

Generally, a 30-year mortgage is better for first-time buyers. The lower monthly payment provides a crucial margin of safety as you adjust to the costs of homeownership, and it frees up cash for unexpected repairs, furniture, and building an emergency fund .

how to stop impulse buying online

Conclusion

The decision between the pros and cons of a 15-year vs 30-year mortgage is one of the most consequential financial choices you will make. It is a classic trade-off between present comfort and future wealth. The 30-year mortgage offers affordability, flexibility, and liquidity, allowing you to buy a home and free up cash for other investments. The 15-year mortgage offers the promise of a paid-off home in half the time, with staggering savings on interest and a forced path to equity building.

In the 2026 housing market, there is no single right answer. The correct choice hinges entirely on your personal financial picture: your income stability, your budget, your tolerance for risk, and your long-term goals. For many, the ideal path is not an either/or proposition. By choosing a 30-year mortgage and employing the discipline to make extra payments, you can capture the flexibility of the long-term loan while still achieving the wealth-building benefits of the short-term one.

Ultimately, the best mortgage is the one that helps you sleep soundly at night, secure in the knowledge that you have a plan for your home and your financial future.

This article is for informational purposes only and does not constitute financial advice. Mortgage rates and terms change frequently. Always consult with a qualified financial advisor and mortgage professional before making a decision. Your home may be repossessed if you do not keep up repayments on your mortgage.

The Ultimate Guide: Pros and Cons of a 15-Year vs 30-Year Mortgage

By Peiman Daneshgar

Email: daneshgar781@gmail.com

Table of Contents

- Introduction: The Most Important Decision in Home Financing

- Understanding the Basics: What Do These Terms Mean?

- The Core Difference: A Side-by-Side Comparison

- The 15-Year Mortgage: A Deep Dive into the Pros and Cons

- The 30-Year Mortgage: A Deep Dive into the Pros and Cons

- Beyond the US: A Note for European Homebuyers

- The “Rich Person’s” Debate: Pay Off Debt or Invest?

- Alternatives to the Traditional 15- or 30-Year Mortgage

- How to Decide: A Step-by-Step Framework

- Strategies to Get the Best of Both Worlds

- The Impact of 2026 Market Conditions

- Frequently Asked Questions

- Conclusion

Introduction: The Most Important Decision in Home Financing

For most people, a mortgage is the largest financial commitment they will ever make. It is also one of the most complex. Before you even start comparing interest rates from different lenders, you face a fundamental, strategic choice that will shape your budget and your financial future for decades: Should you choose a 15-year or a 30-year mortgage?

This decision is about more than just picking a number. It is a trade-off between monthly cash flow and long-term wealth building, between financial flexibility and the psychological comfort of owning your home outright. In the current economic climate of 2026, with interest rates having stabilized at levels higher than the historic lows of the past decade, understanding the pros and cons of a 15-year vs 30-year mortgage is more critical than ever.

This comprehensive guide will walk you through every nuance of this decision. We will analyze the mathematical differences, explore the strategic implications, and provide a clear framework to help you choose the path that aligns with your unique financial situation and life goals. Whether you are a first-time homebuyer in the United States or navigating the different mortgage landscapes of Europe, this article will answer every question you have about the pros and cons of a 15-year vs 30-year mortgage.

Understanding the Basics: What Do These Terms Mean?

Before diving into the complexities, it is essential to define the two main competitors clearly.

What is a 30-Year Fixed-Rate Mortgage?

A 30-year fixed-rate mortgage is a loan amortized over 360 months. As the name suggests, the interest rate is locked in for the entire duration of the loan, meaning your monthly principal and interest payment remains constant for three decades.

- Prevalence: This is the most popular mortgage product in the United States, accounting for roughly 90% of home purchase mortgages . Its popularity stems from its affordability on a month-to-month basis.

- Mechanics: Because the repayment period is long, the principal is paid down very slowly in the early years. In the first decade of a 30-year loan, the vast majority of your monthly payment goes toward interest, not reducing the actual amount you borrowed.

What is a 15-Year Fixed-Rate Mortgage?

A 15-year fixed-rate mortgage is a loan amortized over just 180 months. It offers the same stability of a fixed interest rate but compresses the repayment schedule into half the time.

- Prevalence: Far less common than its 30-year counterpart, 15-year mortgages typically make up less than 10% of new home loans .

- Mechanics: With a 15-year loan, you are forcing yourself to pay off the debt much faster. This results in a significantly higher monthly payment, but it also means you build equity in your home at a much more rapid pace.

The Core Difference: A Side-by-Side Comparison

The choice between these two mortgages boils down to three primary factors: the monthly payment, the interest rate, and the total cost of the loan. To truly understand the pros and cons of a 15-year vs 30-year mortgage, let’s look at a concrete example based on current market data.

Assume you are taking out a loan of $400,000. Based on averages, a lender might offer you a 6.5% interest rate on a 30-year loan and a 6.0% rate on a 15-year loan .

| Feature | 15-Year Mortgage | 30-Year Mortgage | The Difference |

|---|---|---|---|

| Loan Term | 15 years | 30 years | 15 years shorter |

| Interest Rate | Lower (e.g., 6.0%) | Higher (e.g., 6.5%) | 0.5% lower rate |

| Monthly Payment | Higher (~$3,375) | Lower (~$2,528) | ~$847 more/month |

| Total Interest Paid | ~$207,500 | ~$510,000 | ~$302,500 saved |

| Total Cost of Home | ~$607,500 | ~$910,000 | ~$302,500 cheaper |

Figures are estimates for illustrative purposes.

As the table illustrates, the trade-off is stark. The 30-year mortgage offers immediate relief with a lower monthly payment, making it easier to qualify for the loan and fit into your current budget. However, this convenience comes at a staggering cost: you will pay the bank over $300,000 more in interest over the life of the loan .

The 15-Year Mortgage: A Deep Dive into the Pros and Cons

The 15-year mortgage is often championed by personal finance purists like Dave Ramsey as the only way to buy a home . But is it right for everyone? Let’s break down the advantages and disadvantages in detail.

Pros of a 15-Year Mortgage

1. Massive Savings on Interest

This is the single most compelling financial argument for a 15-year loan. As demonstrated in the example above, the interest savings can be in the hundreds of thousands of dollars . You save in two ways: first, lenders typically offer a lower interest rate for shorter-term loans because their money is at risk for less time. Second, you are only paying interest for 15 years instead of 30. This combination dramatically reduces the total cost of your home.

2. Build Home Equity at an Accelerated Pace

Equity is the portion of your home you truly own. With a 15-year mortgage, a much larger chunk of your monthly payment goes directly toward the principal from day one. This rapid equity building gives you financial power sooner. You could potentially use that equity to fund a major renovation, start a business, or have a significant asset to tap into during retirement .

3. True Ownership in Half the Time

Imagine being mortgage-free while you are still in your prime earning years or as you enter retirement. Paying off your home by age 50 or 55 frees up a massive amount of monthly cash flow that can be redirected toward travel, hobbies, or retirement savings. For those approaching retirement, having a paid-off home is a massive relief, significantly reducing monthly expenses on a fixed income .

4. A Disciplined, Forced Savings Plan

A 15-year mortgage acts as a powerful form of forced savings. The higher monthly payment is non-negotiable, compelling you to build wealth with every check you write. For individuals who might otherwise struggle to invest the difference, this structure guarantees that a significant portion of their income is going toward their net worth .

Cons of a 15-Year Mortgage

1. Significantly Higher Monthly Payments

This is the biggest barrier. In our $400,000 loan example, the monthly payment is nearly $850 higher. This can lead to being “house rich, but cash poor,” leaving little room in your budget for other important goals like investing, saving for your children’s education, or even just enjoying life .

2. Reduced Financial Flexibility

Tying up so much of your monthly income in your home can be risky. If you lose your job or face a medical emergency, the inflexible, high payment can become a severe burden. You have less cash on hand to deal with unexpected expenses .

3. You Can’t Borrow as Much

Lenders qualify you based on your debt-to-income (DTI) ratio. Because the monthly payment on a 15-year loan is so much higher, it consumes a larger portion of your gross monthly income. This lowers the maximum loan amount you qualify for, potentially pricing you out of the home you want or forcing you to buy a less expensive property .

4. Higher Opportunity Cost

This is a critical point for wealth-building. The extra money you are throwing at your mortgage each month is money that cannot be invested in the stock market. Historically, the stock market has delivered average annual returns of 7-10%. If your mortgage rate is 6%, you might be financially better off investing the extra cash and earning an 8% return, even after paying the mortgage interest .

The 30-Year Mortgage: A Deep Dive into the Pros and Cons

The 30-year mortgage is the bedrock of the American housing market. Its resilience and popularity stem from the flexibility and breathing room it offers.

Pros of a 30-Year Mortgage

1. Lower, More Manageable Monthly Payments

The primary advantage is affordability. The lower payment makes homeownership accessible to millions of people who could not afford the high payments of a 15-year loan. It fits more comfortably into a monthly budget, allowing you to cover other living expenses without stretching yourself too thin .

2. Superior Cash Flow and Liquidity

By keeping your housing costs lower, you free up cash to pursue other financial opportunities. You can contribute more to your 401(k) or IRA, build a robust emergency fund, save for a child’s college tuition, or invest in other assets. This liquidity provides a safety net that a high mortgage payment can erode .

3. Increased Borrowing Power

Because the monthly payment is lower, your debt-to-income ratio looks much healthier to lenders. This allows you to qualify for a larger loan amount, which can be crucial in expensive real estate markets where home prices are high .

4. The “Optionality” of Prepayment

A 30-year mortgage gives you control. You have the option to make extra principal payments when you have the cash, effectively turning it into a 15-year loan on your own schedule. However, if you hit a rough patch financially, you can simply pay the lower required amount without penalty. This flexibility is something a 15-year mortgage simply does not offer .

Cons of a 30-Year Mortgage

1. Enormous Interest Costs

This is the major drawback. You are paying interest for twice as long, often at a higher rate. Over the life of the loan, you will pay a staggering amount in interest—often more than the original purchase price of the home itself . Some financial critics call this the “30-year trap,” where you end up paying for the bank’s second house while living in your first .

2. Painfully Slow Equity Growth

In the early years of a 30-year mortgage, your payments are almost entirely interest. It can take over a decade to build any significant equity. This means if you need to sell the home after a few years, you might barely break even after realtor commissions and closing costs .

3. Psychological Burden of Long-Term Debt

For some, carrying a large debt for three decades is a source of stress. The idea of making mortgage payments well into one’s 60s can be daunting and runs counter to the goal of a debt-free retirement for many people .

Beyond the US: A Note for European Homebuyers

While this guide focuses on the pros and cons of a 15-year vs 30-year mortgage, it is important to note that the mortgage market in Europe can be quite different.

- Fixed-Rate Terms are Shorter: In many European countries (like the UK, France, and Germany), the most common fixed-rate mortgage terms are 2, 5, or 10 years, rather than 15 or 30 . After this initial “fixed period,” the loan typically reverts to a variable rate, or you must renegotiate a new rate with your lender. True 30-year fixed-rate mortgages are less common outside the US.

- Variable and SARON Mortgages: Products like variable-rate mortgages or those tied to benchmarks like SARON (Swiss Average Rate Overnight) are popular. These offer lower initial rates but expose you to interest rate fluctuations .

- The 25-Year Standard: In the UK, for example, a 25-year mortgage term is a very common standard, representing a middle ground between the US 15- and 30-year options .

- Portability: In many European countries, mortgages are often “portable,” meaning you can transfer them to a new property if you move, avoiding hefty early repayment charges.

For European readers, the principles in this article apply to the total amortization period of the loan. The pros and cons of a 15-year vs 30-year mortgage regarding interest costs and cash flow remain valid, even if your initial fixed-rate period is much shorter. You must also carefully consider the risk of rising interest rates when your initial fixed term ends .

The “Rich Person’s” Debate: Pay Off Debt or Invest?

This is perhaps the most nuanced aspect of the pros and cons of a 15-year vs 30-year mortgage. It boils down to a simple question: what should you do with your extra cash?

The mathematical answer is based on a comparison:

- Guaranteed Return: Paying off a 6% mortgage gives you a guaranteed, risk-free return of 6%. Every dollar you prepay saves you from paying 6% interest in the future .

- Expected Return: Investing in a diversified portfolio (like an S&P 500 index fund) has an historical average return of around 7-10%, but this is not guaranteed.

If your mortgage rate is low (e.g., 3-4%), the math strongly favors investing. The potential returns from the market are almost certainly going to be higher than the cost of your debt.

However, in the 2026 rate environment (with mortgages in the 6-7% range) , the math is much closer. A guaranteed 6.5% return by paying down debt is very attractive compared to a risky 8% return from the market . The decision then becomes about your personal risk tolerance. Do you want the certainty of a paid-off home, or are you willing to accept market volatility for a chance at higher long-term wealth?

Alternatives to the Traditional 15- or 30-Year Mortgage

The 15- and 30-year loans aren’t your only options. Here are a few alternatives to consider.

- 20-Year Mortgage: A happy medium. You get a faster payoff than a 30-year and lower payments than a 15-year, with moderate interest savings.

- 10-Year Mortgage: An aggressive strategy for those who want to own their home outright as soon as possible and can handle a very high monthly payment .

- 40-Year Mortgage: Rare, and usually a bad idea. The lower monthly payments are offset by an astronomical total interest cost .

- Adjustable-Rate Mortgage (ARM): These offer a low fixed rate for an initial period (e.g., 5, 7, or 10 years) and then adjust periodically. They can be a good option if you are certain you will move or refinance before the fixed period ends .

How to Decide: A Step-by-Step Framework

Choosing between the pros and cons of a 15-year vs 30-year mortgage requires a personal, data-driven approach. Use this framework to guide your decision.

Step 1: Run the Numbers

Use an online mortgage calculator to compare the exact monthly payments and total interest for both terms based on current rates for your desired loan amount. The numbers don’t lie .

Step 2: Assess Your Budget with the 28/36 Rule

A common rule of thumb is that your total monthly housing costs (principal, interest, taxes, insurance) should not exceed 28% of your gross monthly income. Furthermore, your total monthly debt payments (including the mortgage, car loans, student loans, and credit cards) should not exceed 36% of your gross income . Can you meet these thresholds with the 15-year payment?

Step 3: Evaluate Your Job Security and Income Stability

If your income is commission-based, seasonal, or variable, the flexibility of a 30-year loan is invaluable. A 15-year loan is best suited for those with very stable, predictable, and secure employment .

Step 4: Consider Your Life Stage and Retirement Goals

If you are in your 50s, a 30-year mortgage would stretch into your 80s, which is not ideal . A 15-year mortgage aligns better with a traditional retirement timeline. If you are in your 20s or 30s, you have more time to leverage a 30-year mortgage for flexibility and investment.

Step 5: Be Honest About Your Financial Discipline

This is the behavioral finance question. Are you disciplined enough to invest the difference every single month? Or will that extra cash simply get spent? If you lack the discipline to invest, the forced savings of a 15-year mortgage is a powerful tool .

Strategies to Get the Best of Both Worlds

You do not have to make a binary choice. Here are strategies to combine the flexibility of the 30-year loan with the wealth-building benefits of the 15-year loan.

1. The “Borrow 30, Pay 15” Strategy

Take out a 30-year mortgage for its lower required payment and easier qualification. Then, set up an automatic payment as if it were a 15-year loan. This gives you the flexibility to drop back down to the 30-year payment if you ever face a financial hardship. As long as you stick to the higher payment, you will pay off your home in 15 years and save a fortune in interest .

2. The Bi-Weekly Payment Plan

Instead of one monthly payment, pay half your monthly payment every two weeks. Because there are 52 weeks in a year, this results in 26 half-payments, which equals 13 full monthly payments. This extra payment each year goes directly to your principal, shaving years off a 30-year loan and saving you thousands in interest .

3. Make One Extra Lump-Sum Payment Per Year

If bi-weekly payments are too complicated, simply commit to making one extra mortgage payment each year, perhaps with your tax refund or work bonus. Mark it clearly for “principal reduction.”

4. Refinance Later

You can start with a manageable 30-year mortgage now. Then, in 5-10 years, if your income has increased significantly and interest rates are favorable, you can refinance into a 15-year loan to finish paying it off .

The Impact of 2026 Market Conditions

As of 2026, the decision matrix has shifted. With mortgage rates hovering in the 6-7% range, the “guaranteed return” of paying down debt is much more compelling than it was when rates were at 3% . The era of “free money” is over.

Furthermore, high home prices mean that the monthly payment on a 15-year mortgage is out of reach for many first-time buyers. In this environment, the 30-year mortgage is often the only viable path to homeownership, allowing people to enter the market and start building equity rather than waiting on the sidelines . The key is to enter with a plan to eventually pay it off faster.

Frequently Asked Questions

Q1: Is a 15-year mortgage always better than a 30-year mortgage?

No. While a 15-year mortgage saves you a tremendous amount in interest, it is not “better” if the high monthly payments leave you financially vulnerable. The “best” mortgage is the one you can afford comfortably while still meeting your other financial goals .

Q2: Can I pay off a 30-year mortgage in 15 years?

Absolutely. This is one of the best strategies. As long as your loan has no prepayment penalty (most don’t), you can make extra principal payments to pay it off on a 15-year timeline. This gives you the flexibility of a lower required payment .

Q3: Why do most people choose a 30-year mortgage?

Most people choose a 30-year mortgage because it offers the lowest possible monthly payment, making homeownership affordable for the average family. It provides more breathing room in the monthly budget .

Q4: What is the main drawback of a 30-year loan?

The main drawback is the enormous amount of interest you pay over the life of the loan. You will likely pay more in interest than the original purchase price of the home .

Q5: How do I qualify for a 15-year mortgage?

Qualifying for a 15-year mortgage is harder. You will need a higher income and a lower debt-to-income ratio because the monthly payment is so much larger. Lenders want to see that you can comfortably afford that higher payment .

Q6: Is the mortgage interest tax deduction a good reason to get a 30-year loan?

For most people, no. Since the Tax Cuts and Jobs Act, the standard deduction has been so high that very few homeowners benefit from itemizing their mortgage interest. The tax savings are usually far less than the extra interest you pay .

Q7: What happens if I can’t make the payments on a 15-year mortgage?

If you cannot make your payments, you risk foreclosure, just as you would with any mortgage. This is the primary risk of choosing a payment that is too high for your budget .

Q8: Are these mortgage terms available in Europe?

Fixed-rate mortgages for the full 15- or 30-year amortization period are less common. In many European countries, you might have a 25- or 30-year amortization schedule, but the interest rate is only fixed for the first 2-10 years, after which it becomes variable or is renegotiated .

Q9: Should I refinance my 30-year mortgage to a 15-year mortgage?

Refinancing to a 15-year term can be a great move if interest rates are lower than your current rate and you can comfortably afford the higher payment. It allows you to lock in savings and pay off your home faster.

Q10: Which mortgage term is better for first-time homebuyers?

Generally, a 30-year mortgage is better for first-time buyers. The lower monthly payment provides a crucial margin of safety as you adjust to the costs of homeownership, and it frees up cash for unexpected repairs, furniture, and building an emergency fund .

Conclusion

The decision between the pros and cons of a 15-year vs 30-year mortgage is one of the most consequential financial choices you will make. It is a classic trade-off between present comfort and future wealth. The 30-year mortgage offers affordability, flexibility, and liquidity, allowing you to buy a home and free up cash for other investments. The 15-year mortgage offers the promise of a paid-off home in half the time, with staggering savings on interest and a forced path to equity building.

In the 2026 housing market, there is no single right answer. The correct choice hinges entirely on your personal financial picture: your income stability, your budget, your tolerance for risk, and your long-term goals. For many, the ideal path is not an either/or proposition. By choosing a 30-year mortgage and employing the discipline to make extra payments, you can capture the flexibility of the long-term loan while still achieving the wealth-building benefits of the short-term one.

Ultimately, the best mortgage is the one that helps you sleep soundly at night, secure in the knowledge that you have a plan for your home and your financial future.