Author: Peiman Daneshgar

Email: daneshgar781@gmail.com

Estimated reading time: 5 minutes

Table of contents

- 1. What Are Sinking Funds?

- 2. Why Sinking Funds Are Important

- 3. How Sinking Funds Work

- 4. The Difference Between Sinking Funds and Emergency Funds

- 5. Common Types of Sinking Funds

- 6. How to Start Your First Sinking Fund

- 7. Where to Keep Your Sinking Funds

- 8. Mistakes Beginners Often Make

- 9. How Sinking Funds Improve Financial Stability

- 10. Frequently Asked Questions

- 11. Final Thoughts

- Minimal Illustration Images (for your article)

1. What Are Sinking Funds?

A sinking fund is money you set aside regularly for a future expense that you already know will happen.

Instead of paying for a large cost all at once, you slowly save for it over time.

For example, imagine you know your car will need new tires next year. Rather than scrambling to find $600 when the time comes, you could save $50 per month until the expense arrives.

By the time you need the tires, the money is already waiting.

Sinking funds transform large financial surprises into manageable monthly savings.

They are one of the simplest ways to reduce financial stress.

2. Why Sinking Funds Are Important

Many financial problems occur because people treat predictable expenses as unexpected emergencies.

Examples include:

- Holiday shopping

- Car maintenance

- Annual insurance payments

- Travel costs

- Home repairs

These expenses are not truly surprises. They happen regularly.

Without planning, these costs often end up on credit cards or loans.

Sinking funds solve this problem by spreading expenses across time.

Instead of one painful payment, the cost becomes small and manageable.

3. How Sinking Funds Work

The concept is straightforward.

First, determine the expected cost of an upcoming expense.

Second, calculate how many months remain before you need the money.

Finally, divide the cost by the number of months.

Example:

Vacation cost: $1,200

Time until vacation: 12 months

Monthly sinking fund contribution:

$1,200 ÷ 12 = $100 per month

By saving $100 each month, the full amount is ready when needed.

This approach removes financial pressure and prevents last‑minute debt.

Digital Envelope Saving System

4. The Difference Between Sinking Funds and Emergency Funds

Many beginners confuse sinking funds with emergency funds.

Although both involve saving money, they serve different purposes.

Emergency funds are for unexpected events such as:

- Job loss

- Medical emergencies

- Sudden home repairs

Sinking funds are for predictable expenses.

Examples include:

- Birthdays

- Vacations

- Car maintenance

- Annual subscriptions

Think of it this way:

Emergency funds handle surprises.

Sinking funds handle planned costs.

Both are essential for a stable financial plan.

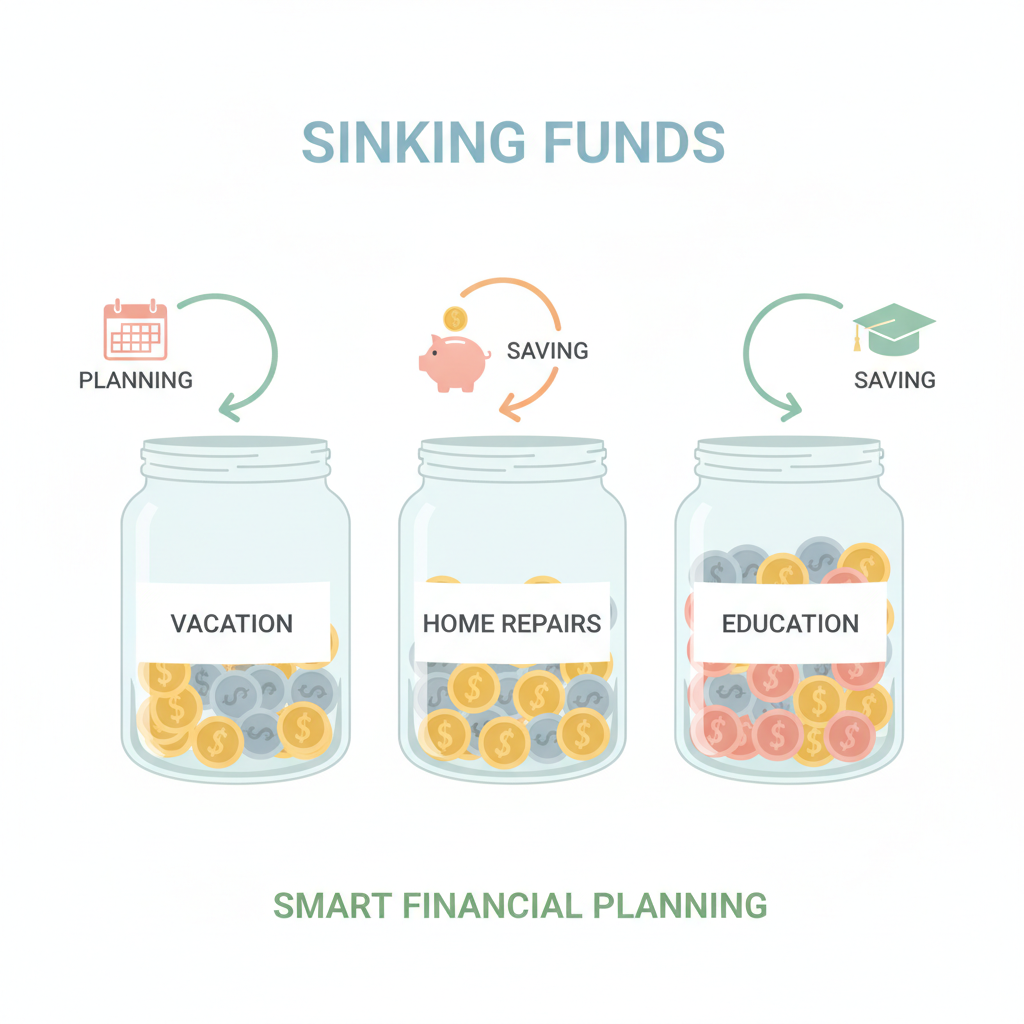

5. Common Types of Sinking Funds

Most people create several sinking funds to cover recurring expenses.

Popular categories include:

Car Maintenance Fund

Cars require repairs, oil changes, and replacement parts.

Saving monthly prevents unexpected repair bills.

Holiday Fund

Many people overspend during the holiday season.

Saving small amounts throughout the year removes financial pressure.

Travel Fund

Vacations are much more enjoyable when they are fully paid for.

A sinking fund allows you to travel without debt.

Home Repair Fund

Homes inevitably require maintenance.

Setting aside money monthly prepares you for these costs.

Annual Bills Fund

Some expenses occur once or twice per year.

Examples include insurance premiums or subscription renewals.

Sinking funds ensure these bills are never a shock.

6. How to Start Your First Sinking Fund

Starting a sinking fund requires only a few simple steps.

Step 1: Identify Upcoming Expenses

Look ahead over the next 6–12 months and list predictable costs.

Examples include:

- Birthdays

- Car maintenance

- Holiday gifts

- Vacations

Step 2: Estimate the Cost

Make a realistic estimate of each expense.

Accuracy is helpful, but the estimate does not need to be perfect.

Step 3: Divide the Cost by Time

Calculate how much to save each month.

For example:

Holiday budget: $600

Time remaining: 10 months

Monthly savings needed:

$60 per month

Step 4: Automate the Savings

Automatic transfers make the process easier.

Each month, move the required amount into a dedicated savings category.

Automation reduces the risk of forgetting.

7. Where to Keep Your Sinking Funds

Your sinking funds should be stored somewhere safe and easily accessible.

Common options include:

High‑Yield Savings Accounts

These accounts earn interest while keeping funds secure.

Separate Savings Accounts

Some people create multiple accounts for different goals.

This makes tracking easier.

Budgeting Apps

Apps can track sinking funds digitally without requiring separate bank accounts.

Choose whichever method keeps the system simple and organized.

8. Mistakes Beginners Often Make

One common mistake is not being realistic about costs.

If you underestimate expenses, your sinking fund may fall short.

Another mistake is mixing sinking funds with everyday spending money.

Keeping funds separate prevents accidental spending.

Finally, some people try to create too many funds at once.

Start with the most important expenses and expand gradually.

9. How Sinking Funds Improve Financial Stability

Sinking funds create financial control.

Instead of reacting to expenses, you prepare for them in advance.

Benefits include:

- Reduced financial stress

- Fewer credit card balances

- Better budgeting accuracy

- Increased financial confidence

Over time, this system creates smoother financial management.

Large expenses stop feeling overwhelming.

10. Frequently Asked Questions

How many sinking funds should I have?

Most people start with three to five funds and add more over time.

Can sinking funds replace emergency funds?

No. Emergency funds are still necessary for unexpected situations.

Should sinking funds earn interest?

If possible, yes. Keeping them in a high‑yield savings account helps your money grow.

What happens if I don’t use the money?

You can roll it forward to the next year or redirect it toward another financial goal.

11. Final Thoughts

Sinking funds are one of the most powerful yet overlooked personal finance tools.

They allow you to prepare for predictable expenses long before they arrive.

Instead of feeling stressed when bills appear, you already have the money ready.

Over time, this approach transforms financial management from reactive to proactive.

The result is a smoother, more stable financial life where fewer expenses catch you off guard.

Minimal Illustration Images (for your article)

You can use these three minimal images in the article:

{kind=link}

{kind=link}

{kind=link}