By: Peiman Daneshgar

Email: daneshgar781@gmail.com

Table of Contents

- I Was You Two Years Ago

- The 30-Second Answer (For People in a Hurry)

- What IS a Bank Account? (Seriously, Let’s Start Simple)

- Checking Accounts Explained Like You’re Five

- Savings Accounts Explained Like You’re Five

- The Side-by-Side Comparison (No Confusing Charts)

- Do I Really Need Both? (Short Answer: Yes, Here’s Why)

- How to Open Your First Account (Without Anxiety)

- What Documents You’ll Need

- How Much Money Do You Need to Start?

- The “Emergency Fund” Concept (Life-Changing)

- Common Beginner Mistakes (And How to Avoid Them)

- What is Interest? (The Free Money Concept)

- Online Banks vs Traditional Banks: Which is Better for Beginners?

- Debit Cards vs Credit Cards: The Important Difference

- Overdraft Explained (And How to Never Pay for It)

- How to Check Your Balance (Without Anxiety)

- The “Pay Yourself First” Habit

- When to Upgrade Your Accounts

- Real Stories: How Beginners Got This Right

- Frequently Asked Questions from Beginners

- Your Next Steps (What to Do After Reading This)

1. I Was You Two Years Ago

Okay, let’s be real for a second.

You’re here because you’ve been putting this off for months. Maybe even years. Every time someone mentions “checking account” or “savings account,” your brain kinda glazes over and you nod like you know what they’re talking about. But inside? You’re thinking, “What’s the difference? Do I need one? Do I need both? Am I supposed to have money in them? HELP.”

I know exactly how you feel.

Two years ago, I was sitting in my apartment with a paycheck in my hand (yes, an actual paper check) and zero idea what to do with it. My friend said “just open a bank account.” Cool. Which one? How? Where? With what money? It felt like everyone else had received some secret manual that I missed.

Here’s the truth that nobody tells you:

Banking is simple. Like, embarrassingly simple. But banks and financial websites make it sound complicated because complicated = confusing = you give up and just accept whatever account they give you with whatever fees they charge.

I tried reading those “beginner’s guides” online. You know what I found? Articles that started with “a checking account is a transactional deposit account held at a financial institution…” and I was asleep by the fourth word.

This guide is different.

I’m going to explain this like we’re sitting at a kitchen table with coffee. No jargon. No “financial institution” nonsense. Just real talk about real money.

By the time you finish this (and I promise to make it interesting enough that you actually will finish), you’ll know more about bank accounts than most adults. You’ll know exactly what to open, where to open it, and what to do with it. And you’ll never feel stupid about money again.

how to talk to your partner about money without fighting

Deal? Awesome. Let’s start with the quick version for the impatient people.

2. The 30-Second Answer (For People in a Hurry)

If you’re the type who wants the short version before deciding if this article is worth your time, here it is:

A checking account is for money you’re going to spend soon. It’s like your wallet, but bigger. You use it for paying bills, buying groceries, getting coffee. Your paycheck goes here, and your money leaves here.

A savings account is for money you’re NOT going to spend soon. It’s like a piggy bank that pays you a little bit of money (called “interest”) just for keeping your money there. You use it for emergencies, for saving up for something big, or for money you just want to keep safe.

Do you need both? Yes. They do different jobs. Using just one is like trying to eat soup with a fork—technically possible but why would you make life harder?

financial milestones you should hit by age 25, 30, 40

That’s the 30-second version. But if you want to actually understand what you’re doing (and avoid the mistakes that cost beginners hundreds of dollars), keep reading. The good stuff is coming.

3. What IS a Bank Account? (Seriously, Let’s Start Simple)

Before we talk about checking vs savings, let’s go even more basic. What actually IS a bank account?

Imagine you have $100 under your mattress. It’s safe from thieves? Maybe. But if your house floods or catches fire, that money is gone. Plus, you can’t spend it online, you can’t use it to pay bills automatically, and it’s not growing at all.

A bank account is just a safer, more useful version of that mattress.

When you put money in a bank account:

- It’s insured – If the bank goes out of business (rare, but happens), the government guarantees you get your money back up to $250,000

- It’s accessible – You can use debit cards, write checks, pay bills online, transfer money to friends

- It can grow – Some accounts pay you interest just for keeping money there

- It’s trackable – You can see where your money goes, which helps with budgeting

- net worth calculator for millennials

That’s it. A bank account is just a safe digital home for your money with some useful features attached.

🤔 Quick question: Right now, without checking, do you know exactly how much money you have? If the answer is “kind of” or “roughly” or “no,” you need a bank account. Seriously. Not knowing is how money disappears.

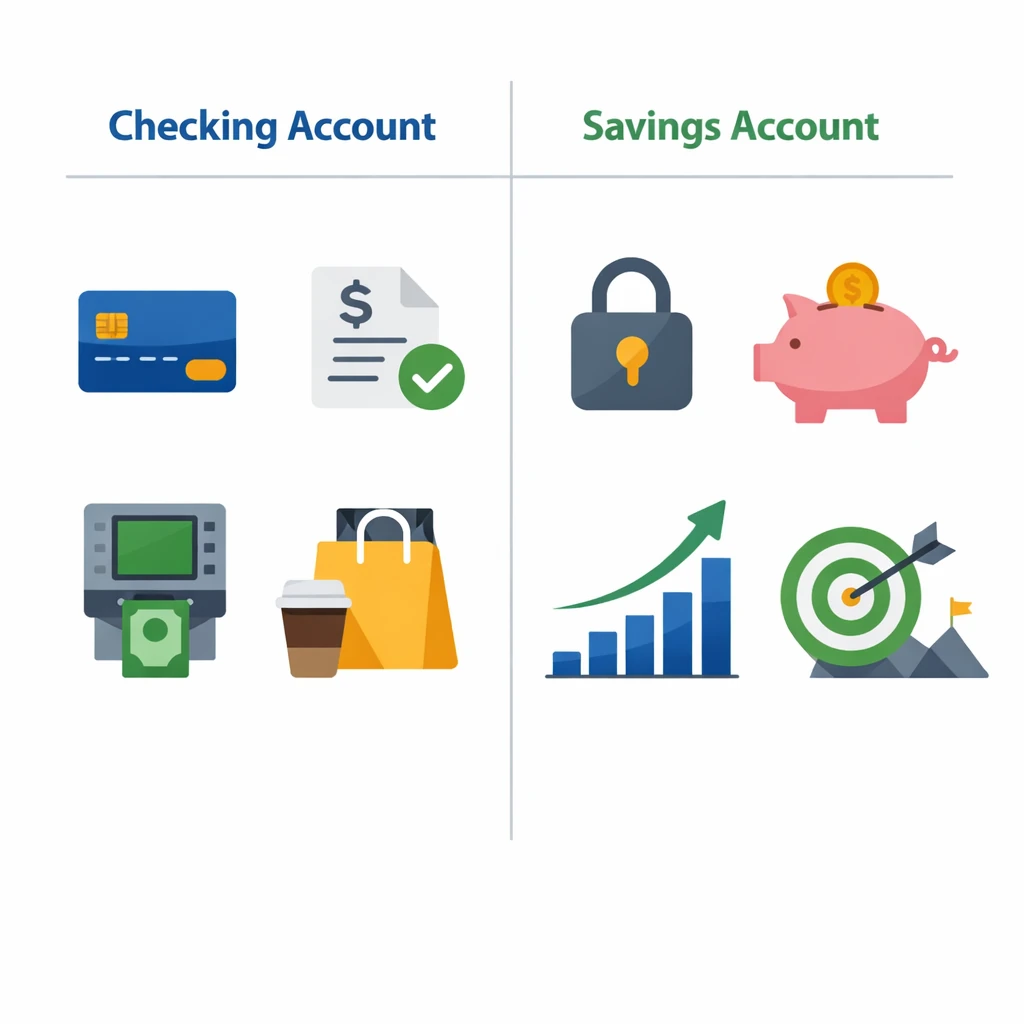

4. Checking Accounts Explained Like You’re Five

Let me paint you a picture.

Imagine you have a favorite pair of jeans with a really good pocket. Every morning, you put some money in that pocket. Throughout the day, you use that money to buy lunch, grab coffee, pay for the bus, maybe buy a movie ticket. At the end of the day, whatever’s left is still there for tomorrow.

That’s a checking account.

It’s your “everyday money” account. Money flows in (your paycheck, birthday gifts, etc.), and money flows out (rent, food, bills, fun stuff). It’s designed for movement.

Here’s what you can do with a checking account:

- Use a debit card – Swipe it at stores, use it online, tap it at coffee shops. The money comes straight out of your account.

- Write checks – Yes, people still use these. Landlords love them for some reason.

- Pay bills online – Set up automatic payments for rent, electricity, Netflix. Never miss a due date.

- Get cash from ATMs – Need physical money? Your debit card gets it from any machine.

- Use payment apps – Link to Venmo, Cash App, Zelle to send money to friends.

- how to create a financial plan step by step

The one thing checking accounts DON’T do well: They barely pay you anything for keeping money there. Most pay 0% interest. Some pay 0.01%, which means $10 earns you one penny per year. Not exactly retirement money.

Who needs a checking account? Everyone. If you have money coming in and going out, you need a checking account. It’s the command center for your financial life.

💡 Real talk: If you’re 18 or older and don’t have a checking account, you’re making life harder than it needs to be. You’re probably paying fees to cash checks or using prepaid debit cards with hidden costs. Open one. Today.

5. Savings Accounts Explained Like You’re Five

Now imagine you have a piggy bank on your dresser. Not the kind you break open, but the kind with a little stopper at the bottom. Every time you have extra money—spare change, birthday cash, money left over from the week—you drop it in the piggy bank.

You don’t touch it for everyday stuff. It’s for “later.” For something special. For emergencies.

That’s a savings account.

It’s your “future money” account. Money goes in, and ideally, it stays there. It’s not for daily coffee runs. It’s for:

- Emergency fund (job loss, car repair, medical bill)

- Big purchase (vacation, new phone, holiday gifts)

- Long-term goals (house down payment, new car)

Here’s what makes savings accounts special:

- They pay you interest – This is the magic part. The bank pays you a little bit of money just for keeping your money there. It’s not much (usually 0.5% to 4% depending on the bank), but it’s free money for doing nothing.

- They’re harder to spend from – Most savings accounts don’t give you a debit card. To get money out, you have to transfer it to checking first. That extra step makes you think twice before spending.

- They keep your money separate – When your savings is in a different account, your brain treats it differently. You don’t see that $1,000 every day and think “I could buy something nice.” You see it as “off-limits” money.

- long-term care insurance: who needs it?

The catch: Savings accounts sometimes limit how many times you can take money out (usually 6 times per month). They’re not designed for frequent withdrawals.

Who needs a savings account? Everyone who wants to build financial security. If you have any goal that’s more than a month away, you need a savings account.

6. The Side-by-Side Comparison (No Confusing Charts)

Let me put this in the simplest terms possible.

| Question | Checking Account | Savings Account |

|---|---|---|

| What’s it for? | Money you’ll spend soon | Money you’re keeping for later |

| Do I get a card? | Yes, a debit card | Usually no (maybe ATM card) |

| Can I pay bills? | Yes, easily | Not really (have to transfer first) |

| Does it earn interest? | No (or basically nothing) | Yes (this is the whole point) |

| Can I take money out anytime? | Yes, unlimited | Yes, but sometimes limited to 6x/month |

| Is it safe? | Yes, FDIC insured | Yes, FDIC insured |

| Should I have one? | YES, everyone needs this | YES, everyone needs this |

Think of it this way:

Your checking account is your front door. Money comes in and goes out all the time. It’s busy, it’s active, it’s where life happens.

understanding your home insurance deductible

Your savings account is your backup closet. Stuff goes in, stays there, and you only open it when you really need something.

7. Do I Really Need Both? (Short Answer: Yes, Here’s Why)

This is THE question everyone asks. “Can’t I just use one account for everything?”

Technically, yes. You CAN use just a checking account.

But here’s why that’s a bad idea:

Reason 1: You’ll spend your savings

When all your money is in one account, your brain sees the total and thinks “I have extra money.” That $2,000 in your account? Part of it is for rent next week. Part is for groceries. But your brain just sees $2,000 and thinks a new TV would be nice.

When you separate your money—$1,500 in checking for bills, $500 in savings for emergencies—your brain goes “oh, I only have $1,500 to spend.” You naturally spend less.

Reason 2: You’re losing free money

If you keep your savings in checking, you earn ZERO interest. If you move it to a savings account (especially a high-yield one at an online bank), you earn 4% or so. On $1,000, that’s $40 a year for doing absolutely nothing.

Reason 3: No emergency barrier

Life happens. Your car breaks down. Your phone dies. You get a medical bill. If all your money is in checking, you might spend your emergency fund without realizing it. A separate savings account keeps that money safe until you actually need it.

is pet insurance worth the cost?

The truth:

Using just a checking account is like using a screwdriver for everything—hammering nails, prying open paint cans, stirring coffee. It kinda works, but it’s not what it’s designed for, and you’ll do a better job if you use the right tool.

Use checking for money leaving soon. Use savings for money staying put.

🎯 Quick test: Look at your bank accounts right now. If you only have one, open a savings account this week. If you have both but they’re at the same bank, check the interest rate on your savings. If it’s below 0.5%, move it to an online bank. Do it today.

8. How to Open Your First Account (Without Anxiety)

Okay, you’re convinced. You need accounts. But how do you actually open them? It’s easier than you think.

Step 1: Pick a Bank

You have three main options:

Option A: Your Local Bank

- You’ve seen the building. Maybe you’ve walked past it.

- Pros: You can talk to humans, deposit cash easily, get cashier’s checks fast

- Cons: Lower interest rates on savings, possible fees

Option B: Online Bank (like Ally, Marcus, Chime, SoFi)

- No physical buildings, all app/website based

- Pros: Higher interest rates (4%+ on savings), fewer fees, better apps

- Cons: Hard to deposit cash, no in-person help

Option C: Credit Union

- Like a bank but owned by members, not shareholders

- Pros: Lower fees, better rates, more personal service

- Cons: Fewer branches, less fancy technology

For beginners, I’d recommend: Start with an online bank for savings (for the high interest) and maybe a local bank or credit union for checking (if you need to deposit cash).

Step 2: Go to Their Website or App

Don’t overthink this. Open your phone, download the app, or visit their website. Look for “Open Account” or “Get Started.”

Step 3: Choose the Account Type

They’ll ask: checking or savings?

- If you’re opening your first account, start with checking

- If you already have checking, open savings

Step 4: Fill Out the Application

This takes 5-10 minutes. They’ll ask for:

- Your name, address, date of birth

- Social Security number (to verify identity)

- Email and phone number

- Employment info (optional usually)

- disability insurance for self-employed professionals

Step 5: Fund the Account

Most banks require an initial deposit. This can be as low as $0 to $25 for basic accounts. You can fund it by:

- Transferring from another bank account

- Depositing a check (take a photo in the app)

- Transferring from a debit card

Step 6: Wait for Approval

Most online applications are approved instantly or within 1-2 business days. You’ll get an email when you’re all set.

9. What Documents You’ll Need

Don’t let paperwork scare you. It’s simple:

For U.S. citizens:

- Social Security number

- Government-issued ID (driver’s license, state ID, passport)

- Date of birth

- Current address

- how to shop for car insurance and get the best rate

For non-U.S. citizens:

- Passport

- Visa or immigration documents

- Sometimes a second form of ID

- Tax ID number (ITIN) if no SSN

Pro tip: Have your ID and Social Security card handy when you start. The process goes faster.

10. How Much Money Do You Need to Start?

This is the question that stops people cold. “I don’t have enough money to open an account.”

Here’s the truth: You can open most accounts with $0 to $25.

- Online banks – Often $0 minimum to open

- Local banks – Usually $25 to $100 for basic checking

- Credit unions – Often $5 to $25 (this buys you a “share” in the credit union)

- high-deductible health plan with HSA pros and cons

If a bank wants $100 minimum and you don’t have it, keep looking. There are hundreds of banks with no minimums. Don’t let a lack of money stop you from opening an account—that’s exactly when you need one the most.

What if you literally have $0? Some banks will still let you open an account. You just can’t fund it until you have money. Do it anyway. Get the account set up so when you get money, it has somewhere to go.

11. The “Emergency Fund” Concept (Life-Changing)

This is the most important thing you’ll learn about savings accounts.

An emergency fund is money you save specifically for unexpected bad things.

Not vacations. Not new phones. Not “treat yourself” days. Emergencies only.

What counts as an emergency:

- You lose your job and need to pay rent

- Your car breaks down and you need repairs

- You have a medical bill

- Your pet needs emergency vet care

- You need to travel suddenly for a family emergency

What’s NOT an emergency:

- Sales at your favorite store

- Concert tickets

- A weekend trip

- A new video game

How much should you save?

Start small. Like, really small.

- Goal 1: $500 (covers most small emergencies)

- Goal 2: $1,000 (covers more)

- Goal 3: 1 month of expenses

- Goal 4: 3 months of expenses

- Goal 5: 6 months of expenses (ideal for most people)

Where should this money live? In your savings account. Not your checking. Not under your mattress. Not invested in stocks. A boring, safe, accessible savings account.

🔥 Mind-blowing fact: 44% of Americans couldn’t cover a $400 emergency without borrowing or selling something. If you save just $500, you’re ahead of nearly half the country. That’s not hard—that’s skipping a few takeout meals.

12. Common Beginner Mistakes (And How to Avoid Them)

Let me save you some pain. Here’s what beginners mess up:

Mistake 1: Not Reading the Fine Print

The mistake: Opening an account without knowing the fees.

How to avoid it: Before you click “open account,” look for:

- Monthly maintenance fees

- Minimum balance requirements

- ATM fees

- Overdraft fees

If there are fees, ask: “Can these be waived?” (Usually yes, with direct deposit or minimum balance.)

Mistake 2: Keeping All Money in Checking

The mistake: Having a $5,000 balance in checking earning 0% interest.

How to avoid it: Keep 1-2 months of expenses in checking. Move the rest to savings where it earns interest.

Mistake 3: Using Savings Like Checking

The mistake: Dipping into savings for everyday stuff.

How to avoid it: Remember the “emergency only” rule. If you’re taking money out of savings more than once a month, something’s wrong.

Mistake 4: Not Setting Up Alerts

The mistake: Forgetting to check your balance and overdrawing.

How to avoid it: Set up text or email alerts for:

- Low balance (under $100)

- Large transactions

- Any transaction (if you want to track everything)

Mistake 5: Ignoring Interest Rates

The mistake: Keeping savings at a big bank earning 0.01%.

How to avoid it: Check your savings interest rate. If it’s below 1%, move your money to an online bank. It takes 15 minutes and can earn you hundreds more per year.

Mistake 6: Overdrafting

The mistake: Spending more than you have and paying $35 fees.

How to avoid it:

- Track your balance (use the app)

- Opt out of overdraft (so transactions just get declined instead of going through and charging you)

- Link your savings for overdraft protection (auto-transfers from savings if checking runs low)

13. What is Interest? (The Free Money Concept)

Interest sounds complicated. It’s not. Let me explain it simply.

Interest is money the bank pays you for letting them hold your money.

Why would they do that? Because banks use your money to lend to other people (for mortgages, car loans, credit cards). They charge those people interest, and they share a tiny bit of that with you.

Here’s how it works:

You put $1,000 in a savings account with 4% interest.

After one year, the bank gives you $40. Just for keeping your money there.

After two years, you have $1,000 + $40 (year 1) + $41.60 (year 2 interest on $1,040) = $1,081.60

That extra $1.60 in year 2 is “compound interest”—interest on your interest. It’s small at first, but over time it grows.

The 10-year picture:

- $1,000 at 0.01% (typical big bank savings) = $1,001 after 10 years

- $1,000 at 4% (online high-yield savings) = $1,480 after 10 years

That’s $479 free dollars just for picking the right bank.

Types of Interest Rates

APY (Annual Percentage Yield) – This is the number you care about. It’s the real rate you earn after compounding. Always compare APYs when choosing accounts.

Fixed vs Variable – Most savings accounts have variable rates. They can go up or down based on what the Federal Reserve does. Online banks usually adjust quickly; big banks barely adjust at all.

14. Online Banks vs Traditional Banks: Which is Better for Beginners?

Let’s settle this debate.

Online Banks (Ally, Marcus, SoFi, Chime, Discover)

Pros:

- Higher interest rates (4%+ on savings vs 0.01% at traditional banks)

- Fewer fees (many have $0 monthly fees)

- Better apps and technology

- ATM fee reimbursement (use any ATM, get fees refunded)

Cons:

- Can’t deposit cash easily (some accept cash at certain retailers)

- No in-person help (phone/chat only)

- Transfers can take 1-3 days (though many are instant now)

Traditional Banks (Chase, Bank of America, Wells Fargo)

Pros:

- Physical branches with humans

- Cash deposits easy

- Cashier’s checks and notary services available

- May have more products in one place

Cons:

- Terrible interest rates (0.01% on savings)

- More fees

- Older technology

Credit Unions

Pros:

- Member-owned, so better rates and lower fees

- More personal service

- Part of shared branching networks (use other credit unions)

Cons:

- Fewer branches

- Technology can be behind

- Must meet membership requirements (sometimes just living in an area)

The Verdict for Beginners

For savings accounts: Online banks win, no contest. Higher interest, fewer fees. Put your emergency fund and savings goals here.

For checking accounts: It depends. If you need to deposit cash regularly or want in-person help, go local. If you’re fine with all-digital, online checking is great too.

The power move: Have both. Checking at a local bank or credit union for cash needs, savings at an online bank for the high interest.

15. Debit Cards vs Credit Cards: The Important Difference

Since we’re talking about checking accounts, let’s clear up a common confusion.

Debit Cards (Linked to Your Checking Account)

When you use a debit card:

- Money comes OUT of your account immediately

- You can only spend what you have

- No interest, no payments, no bills

Good for: Everyday purchases, sticking to a budget, avoiding debt

Bad because: Less fraud protection than credit cards, doesn’t build credit history

Credit Cards (Not Linked to Checking)

When you use a credit card:

- The bank pays first, you pay them back later

- You’re borrowing money (with a promise to repay)

- If you don’t pay in full, you pay interest

Good for: Building credit history, better fraud protection, rewards points

Bad because: Easy to overspend, interest is expensive if you carry a balance

The Beginner’s Approach

Use your debit card for everyday spending when you’re starting out. It keeps you honest—you can’t spend what you don’t have.

Once you’re comfortable, get a credit card for one or two small purchases each month (like Netflix or gas). Pay it off in full every month. This builds your credit history without getting into debt.

16. Overdraft Explained (And How to Never Pay for It)

An overdraft happens when you spend more money than you have in your checking account.

Example: You have $50 in your account. You buy something for $60. You’re now negative $10.

What Happens Next?

Option A: Bank covers it (overdraft)

- Bank pays the $60 transaction

- Your balance goes to -$10

- Bank charges you $35 overdraft fee

- You now owe $45

Option B: Bank rejects it (non-sufficient funds)

- Bank declines the transaction

- Your card is declined at checkout (embarrassing)

- Bank may still charge a $35 “returned item” fee

Neither is great.

How to Never Pay Overdraft Fees

Method 1: Opt out of overdraft

Most banks let you choose. If you opt out, transactions that would overdraw you just get declined. No fee, no negative balance. Just an embarrassing moment at checkout.

Method 2: Link savings for overdraft protection

Connect your savings to checking. If checking runs low, money automatically transfers from savings. Banks usually charge a small fee ($5-10) or nothing for this. Much cheaper than $35.

Method 3: Track your balance

This sounds obvious, but most overdrafts happen because people forget about pending transactions. Check your app before spending.

Method 4: Keep a cushion

Keep an extra $100 in checking as a buffer. Pretend it’s not there. If you accidentally overspend, it catches you.

17. How to Check Your Balance (Without Anxiety)

Some people avoid checking their balance because it stresses them out. I get it. But ignorance isn’t bliss—it’s overdraft fees.

Easy Ways to Check

Method 1: Mobile App (Best)

Open your bank’s app. Log in (use face ID or fingerprint). Balance is right there. Takes 5 seconds.

Method 2: Text Alerts

Set up alerts for:

- Daily balance (bank texts you every morning)

- Low balance warning (text when under $100)

- Large transactions (text when over $50)

Method 3: Website

Same as app but on computer.

Method 4: ATM

Insert card, enter PIN, select “check balance.” Prints a receipt or shows on screen.

Method 5: Call

Call the number on your card. Automated system tells you balance.

The “Check Daily” Habit

Get in the habit of checking your balance every morning with your coffee. Takes 10 seconds. You’ll never be surprised again.

18. The “Pay Yourself First” Habit

Here’s a mindset shift that changes everything.

Most people do this:

- Get paycheck

- Pay bills

- Spend money

- Save whatever’s left (usually nothing)

The “Pay Yourself First” method:

- Get paycheck

- Immediately move money to savings (even $20)

- Pay bills with what’s left

- Spend what’s left of that

When you save first, you actually save. When you save last, you never save.

How to Do It

Manual method: Every payday, log into your bank and transfer money to savings before you do anything else.

Automatic method (better): Set up an automatic transfer from checking to savings for the day after payday. It happens without you thinking about it.

Start small: $10, $20, $50—whatever you can. The amount matters less than the habit.

💪 Challenge: This month, set up an automatic transfer of $25 from checking to savings on payday. Don’t touch that money for 3 months. See how it feels to have that cushion.

19. When to Upgrade Your Accounts

As you get more comfortable with banking, you might want “better” accounts. Here’s when to consider it.

Signs You’re Ready for a Better Account

You’ve outgrown your beginner account if:

- You consistently have $1,000+ in checking

- You have 3+ months of expenses in savings

- You’re paying fees that could be avoided

- You want higher interest than your current savings pays

- You’re ready to start investing

What “Upgrading” Means

Better savings:

- Move from big bank (0.01%) to online bank (4%+)

- Open multiple savings accounts for different goals (emergency, vacation, house)

- Consider a Money Market Account for slightly higher rates with check access

Better checking:

- Switch to an account that pays interest on checking

- Find an account with better ATM access

- Look for accounts with sign-up bonuses ($200-500 for new customers)

Beyond basic:

- Open a CD (Certificate of Deposit) for money you won’t need for 6 months to 5 years (usually higher rates than savings)

- Start an IRA for retirement savings

- Open a brokerage account for investing in stocks/bonds

20. Real Stories: How Beginners Got This Right

Let me share some real examples of people who started where you are.

Sarah’s Story: From Cash to Confidence

Sarah was 24, working as a barista, and kept all her money in a shoebox. Cash only. She was terrified of banks after her mom had overdraft problems.

What she did: She opened a free checking account at a credit union with just $25. She set up direct deposit for her tips (yes, you can deposit cash at credit unions). After 3 months of seeing her money safely in the app, she opened a savings account and started auto-transferring $20 per week.

One year later: Sarah had $1,040 in savings (enough for a emergency fund) and had never paid a single fee. She said the biggest change wasn’t the money—it was not worrying anymore.

Marcus’s Story: The High-Interest Switch

Marcus (yes, that’s his real name) had $5,000 in a savings account at a big bank earning 0.01%—about 50 cents a year. He thought that was normal.

What he did: He read an article about online banks, opened an Ally savings account in 10 minutes, and transferred his $5,000. He set up automatic transfers of $200 per month from checking.

One year later: Marcus earned $200 in interest (at 4%) instead of 50 cents. Plus he saved another $2,400 automatically. His $5,000 had grown to $7,600 without him doing anything differently.

Elena’s Story: The Overdraft Cycle

Elena kept overdrawing her account—$35 here, $35 there. She’d paid over $300 in fees in one year.

What she did: She opted out of overdraft coverage, meaning transactions just got declined instead of going through and charging her. She set up low balance alerts on her phone. She kept a $100 cushion in checking.

One year later: Zero overdraft fees. She said the first month was hard (getting declined at the grocery store once), but after that, she learned to check her balance and plan better.

21. Frequently Asked Questions from Beginners

Q: Can I have both a checking and savings account at the same bank?

A: Yes! Most people do. It makes transfers between accounts instant and easy. Just check that your savings is earning decent interest—if it’s not, consider opening savings elsewhere.

Q: How many bank accounts should I have?

A: At minimum: one checking, one savings. For better organization: one checking, multiple savings (emergency fund, vacation fund, etc.).

Q: What happens to my money if the bank fails?

A: If your bank is FDIC insured (most are), the government guarantees your money up to $250,000 per account type. You’ll get it back within a few days. Since 1933, no one has lost FDIC-insured money.

Q: Can I open a bank account if I have bad credit?

A: Yes! Banks don’t check your credit for basic checking/savings accounts. They use ChexSystems (a report on your banking history). If you’ve had problems before, look for “second chance” accounts.

Q: What’s the minimum age to open an account?

A: 18 to open alone. Under 18, you need a parent or guardian as joint owner.

Q: Should I get a credit card or debit card first?

A: Debit card first. Learn to manage money without the risk of debt. Later, get a credit card for one small bill and pay it in full every month.

Q: How do I choose between online and traditional banks?

A: For savings, choose online (better interest). For checking, choose what works for your lifestyle—online is fine if you don’t need cash deposits.

Q: What’s a “high-yield” savings account?

A: Just a savings account with a higher-than-average interest rate. Usually offered by online banks. Currently “high-yield” means 4% or more.

Q: Can I lose money in a savings account?

A: No. Savings accounts don’t lose value (unlike stocks). The only way to lose money is if you spend it or if fees eat it. Choose no-fee accounts.

Q: How do I deposit cash with an online bank?

A: This is tricky. Some online banks accept cash deposits at certain retailers (like CVS or Walmart) for a small fee. Others don’t accept cash at all. If you deal with cash often, keep a local bank account for deposits.

Q: What’s the difference between APY and interest rate?

A: APY includes compounding; interest rate doesn’t. For savings accounts, always compare APY—it’s the real rate you’ll earn.

Q: When should I open a savings account?

A: Yesterday. Seriously, open one as soon as you have any money at all. Even $10. Start the habit.

22. Your Next Steps (What to Do After Reading This)

You made it to the end. That means you’re already ahead of most people who start reading articles like this and give up halfway through. Pat yourself on the back.

But reading isn’t the same as doing. Here’s your action plan:

This Week

- Check what you already have – Log into your bank accounts. What accounts do you have? What are the interest rates? Any fees?

- If you have no accounts: Open a checking account at a bank or credit union. Start with $25 if you have it. Just do it.

- If you have checking but no savings: Open a savings account. Online bank recommended (Ally, Marcus, SoFi, etc.). Transfer $20 to start.

- If you have both: Check your savings interest rate. If it’s under 1%, move your money to a high-yield online bank.

This Month

- Set up automatic transfers – Payday → checking → automatic transfer to savings. Start with $20-50 per paycheck.

- Build your first $500 – This is your mini emergency fund. Once you hit $500, celebrate. You’re ahead of 44% of Americans.

- Track your spending for one month – See where your money actually goes. Use your bank app or a simple notebook.